BIG BUSINESS BAILOUT!! TAX PAYER MONEY!! ADANI AMBANI, NPAs!! Etc etc etc screamed the Twitter liberal circle. On the other hand a section of dolts kept saying “we need reforms”. This is not enough. Need to do more. A golden chance to correct errors is being missed. Etc etc etc..

Its not quite clear what these people intend to say. Anyway I shall keep that for some other day. Let us focus on the Bank Recapitalization part for now. I shall try and explain the whole activity in as many simple terms as possible.

What is Capital Adequacy Ratio (CAR)/(CRAR):

A bank cannot keep on lending. There are certain limits to it. These limits are set to protect depositors like you and me and to promote a stable and efficient financial system. Thus the capital “adequacy” ratio, as the name suggests, is a measure of a “bank’s capital.” It is expressed as a percentage of a bank’s risk weighted credit exposures or in simpler terms its “loans”. CAR is also known as Capital to Risk (Weighted) Assets Ratio (CRAR)

So What was the problem with CRAR?

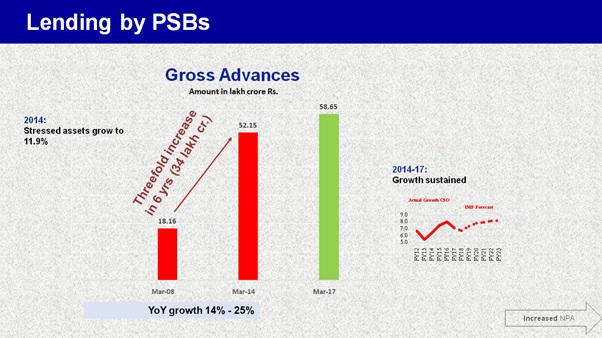

Indiscriminate Lending under UPA government!!

This chart explains how loan portfolio of banks increased manifold. There were certainly few allegations that loans were issued on phone calls and under influence from top politicians. Some of the practices from then are captured in Vijay Mallya’s saga. Anyway, this lending led to an increase in NPA’s. If you lend to an unviable project, it cannot service the debt! This is precisely what happened. As on today the total banking NPAs have crossed Rs 8 lakh crore in the quarter ended June 2017, 90% of which are from public sector banks.

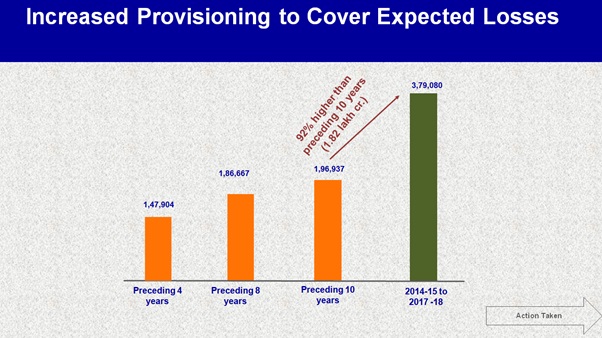

When an account is declared “NPA” banks have to mandatorily make “provisions” for bad loans in their books which leaves them with even lesser money to lend further and very badly affects their profitability and capital adequacy.

So tell me who is to be blamed for this situation? The people under who’s tenure the loans were given or the people who are trying to fix the rot?

This indiscriminate lending has resulted in six banks having been put under the “prompt corrective action” category by the Reserve Bank of India. This means that their activities like announcing dividend, opening branches, hiring and giving further loans to below investment grade rated entities are restricted. In fact the headlines should read how UPA nearly collapsed the banking system.

Banks had to cushion in a lot of provisions to cover up these loans. A graph issued by the Finance Ministry covers this aspect:

All in all, poor oversight by the UPA government over functioning of the Public Sector Banks, nearly collapsed our economy. The provisioning has eroded the capital adequacy ratio thereby hampering the ability of banks to lend fresh loans.

So why this “Capitalisation of Banks”

Capitalisation simply means infusing fresh capital with the banks. This time the government is planning to issue “Capitalisation bonds” to raise funds. Here is one of the ways it can be done:

Government issues bonds. Banks subscribe to bonds. Government gets funds. Government uses same funds to infuse into banks and thereby expanding their capital base. Thus improving CRAR. This allows banks to lend fresh loans and even allows them to raise even more funds from outsiders at cheaper rate.

These fresh loans generate productive assets, jobs and create demand. Demand drives the economy. The exact mechanism of these bonds has not been announced yet but it will come out in due course of time.

Who shall benefit out of this?

Anybody who is willing and eligible for a commercial loan from a bank shall benefit out of this. Banks, which are currently stressed and cannot lend much, will be freer to lend. They need eligible and good borrowers to keep the cycle running. The Finance Minstry highlighted that special focus shall be given on Mudra and Standup India loans once fresh capital is infused.

Are Tax Payers Bailing Out Banks?

The technical versions may say NO, but to put it bluntly: Yes. But we have to remember there is no other option. We are in a tight spot, and this could be the best out of bad options. Let anyone tell you otherwise, we cannot let our banks die.

Are Tax Payers bailing out the NPA accounts or big defaulters?

No. The proceedings under various laws are going on. The recovery proceedings against defaulters will not stop. There is a difference between bailing out a bank and an individual borrower. So no, you aren’t paying Vijay Mallya’s loan off.

What is the guarantee that future loans will not go bad?

True. There is no guarantee. They may also go the same way. For that systemic reforms have been taken by this government. Here is a glimpse of the same.

Lending based on sound principles will ensure lesser NPA’s. Bank Boards and credit appraisal system have been revamped. Insolvency and Bankruptcy code has been enacted. State Bank Group has been consolidated. MOUs with 11 Public Sector Banks have been signed to ensure a turnaround. None of this was done by the UPA. It was done under the Modi Government.

Conclusion

Instead of following views of some policy wonks and copy-paste “economists” on twitter, listen to what experts have to say. There is no denying that Banks today are not in the best of shape. There is also no denying that most of the loans which are causing troubles, were extended during the UPA regime. The current Government is essentially cleaning up the mess of the previous Government, and as you know, in any clean-up, hands will get dirty. The public at large needs to only ensure that even after this clean up, Banks do not go back to their old ways of lending. Stricter norms for loan appraisal need to be enforced and the Government must ensure that we do not see a repeat of the crisis.

Post Script

If you are a Raghuram Rajan fan and are wondering “what would he have done”, read this:

“I think it’s important to recognize that banks do need capital and you need to put it aside and if it means that there are other resources allocations that should be reduced, so be it. I mean, that’s the cost of staying within the budget. This is not painless,”