What makes a good RBI governor? If one were to ask this question to a layman, prompt would be the response with a ‘one who cuts down my home loan rates faster or chuck that, one who doesn’t make anti-India (that too as per my definition ) statements in the world forums’. ‘Perhaps someone who isn’t at loggerheads with the government’. But well, there’s much more to it. Your home loan rate that you end up paying, is a constituent of mainly two components viz. base lending rate in the economy (repo rate, set by the RBI) and the margin charged to you by your bank. And this margin charged by the bank is a function of demand/supply dynamics of money and the banks’ balance sheets and at their discretion. This is more or less the case with Corporates’ borrowing as well, give or take some bargaining power.

) statements in the world forums’. ‘Perhaps someone who isn’t at loggerheads with the government’. But well, there’s much more to it. Your home loan rate that you end up paying, is a constituent of mainly two components viz. base lending rate in the economy (repo rate, set by the RBI) and the margin charged to you by your bank. And this margin charged by the bank is a function of demand/supply dynamics of money and the banks’ balance sheets and at their discretion. This is more or less the case with Corporates’ borrowing as well, give or take some bargaining power.

Did you know that since a year and a half (which forms half the term of Rajan), RBI has cut down almost 150 basis points in the Repo rates, but it is your banks who haven’t been passing that down to you? So far, on an average, banks have only passed down around 60-70 bps to the end borrower, with RBI governor repeatedly urging them to do so. Do you know that it is with this margin that your banks make profits. Even at a policy level, the inflation debate is always an inconclusive one. There are as many views as people and it is always easier to criticise in hindsight. Many have critiqued Rajan for not cutting rates further, but what value does it hold to the end consumer if we are still away by 60-70bps being passed down to us by the banks? Ir-respectively, the fact remains that inflation did come down from double digit levels when Rajan took over to around 5% on an average now.

It is with Rajan’s insistence that RBI and the Government decided to put in place a monetary policy framework in Mar’15, with a CPI based inflation targeting. The new framework makes RBI more accountable, as it will have to offer explanations to government on missing inflation targets. This restrains RBI from taking any aggressive or accommodative monetary policy stance, putting India on par with other countries in terms of flexible inflation targeting.

By mid-2013, Rupee had seen a sharp free fall to the levels of 70. India’s current account deficit had risen to a staggering 5% of GDP! CAD is basically a measure of the amount of supply of dollars (since that is the major currency of trade) in the country and a rising CAD indicates that the country is importing more than it is exporting. This causes the local currency to depreciate. India’s forex reserves had gone down to $250B and the government had signalled that they might run out of reserves in a few months. While the entire financial industry was in a panic mode, many of us were sitting in our offices wondering how many more days we have left in our jobs. The then governor Subbarao had imposed capital controls on Indian companies to limit their abilities to sell Rupees. One of the major duties of a central Bank’s governor is to continuously decide the supply of currency in the country.

So, when Raghuram Rajan took over as one on 5th September, he took over a in a difficult situation and one of the most challenging tasks ever! Today, we’re looking at a CAD of a very mellow 0.1% of GDP and our forex reserves just touched record highs of $363B on 10th June. (Average reserves in the period have been at $350B). “Rupee gained 10% between September and Dec’13 on the back of RBI measures”. With stronger reserves, RBI has managed to curb volatility in exchange rates. For it is the volatility of the currency which hurts participants more than its levels. The more volatility the currency, the higher than hedging cost and higher losses. It is this strength imparted to India’s balance sheet and stability to Rupee that made international investors comfortable with India again. A remarkable fea t indeed!

In the last quarter of 2015-16, RBI gave a deadline to banks to declare all bad loans on their books and clean their balance sheets until Mar’17 instead of postponing and masquerading them as good loans. As a result of this, PSU banks have declared NPAs of almost 4 lakh crores and much more by now. Bilk of these are from loans issued by banks a good 5 years back, or even more. The chickens are just coming home to roost now. RBI’s strict stance on the matter has hastened the process of NPA recognition and provisioning by banks. This move is going to add strongly to the edifice of our banking system.

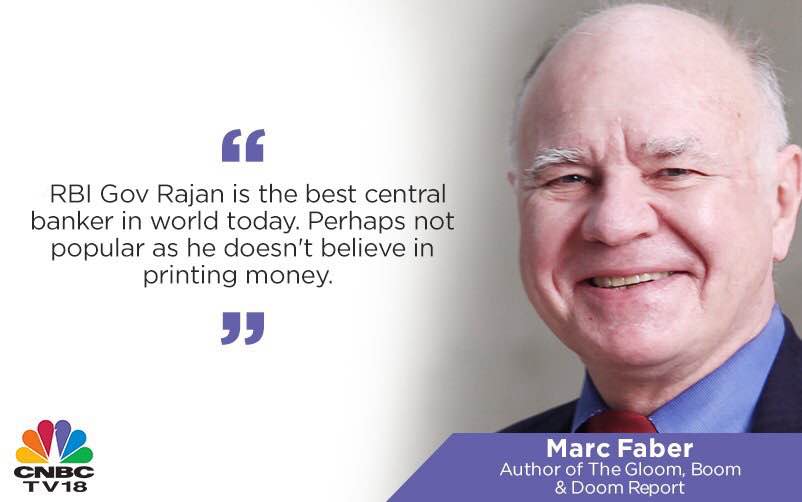

The list of Rajan’s contribution in making our Institutions’ foundations stronger is endless. It is because of these accomplishments that he has become an important figure in the eyes of

International investing community. Below are some international voices on Rajan’s exit :

There may have been some disagreements between the governor and the government, which is bound to happen by design if the governor is an independent thinker. It has only benefitted us as a nation and put us a few steps ahead on our way to progress. After all, we do take pride in having our autonomous institutions being run so, don’t we?

When has India Inc ever come together to voice their support to an RBI governor to retain him? Industry stalwarts like Rahul Bajaj, Harsh Mariwala, Adi Godrej, Kiran Majumdar Shaw, Deepak Parekh et al have acknowledged that Rajan must stay.

The reason for his exit (at least in public perception) could very well be some very personal and unsubstantiated attacks by Subramanian Swamy. A good Governor leaving in the backdrop of some frivolous attacks certainly doesn’t look good. No single person is indispensable and no individual is greater than the institution especially one like RBI, but India might have let an asset slip out of its grip. Rajan will be only the second governor to have served only for three years.