In a major announcement, following the GST Council Meeting at Guwahati, Finance Minister Arun Jaitley announced that a decision was made to tax food at all stand-alone restaurants, AC and non-AC, at a uniform rate of 5%. This was a departure from the existing rates of 12% and 18%.

This apparent reduction in rates brought cheer to many on social media:

GOOD NEWS: Eating out becomes cheaper, GST reduced by 13%. Now, pay only 5% GST when you dine in at the restaurants of your Choice!

— Prashant Kumar (@Prashant_TN) November 10, 2017

Thanks to @arunjaitley ji for reducing #GST to 5% in restaurants, now food is cheaper by 13%. #GSTCouncil #GSTCouncilMeet

— Karthik (@skarthikdotin) November 10, 2017

But will eating out really be cheaper by 13%? Lay people will not understand this, but the reduced rate of 5% comes with a rider. The press release stated the terms:

All stand-alone restaurants irrespective of air conditioned or otherwise, will attract 5% without ITC. Food parcels (or takeaways) will also attract 5% GST without ITC.

The words “without ITC” are key. ITC refers to Input Tax Credit. ITC basically is GST paid on purchase made. In the case of a restaurant, the GST which is charged on the rent it is paying, or on the groceries it is buying, is called ITC. This GST paid while purchasing items, can be utilized while making payment of GST which a restaurant collects from its customers.

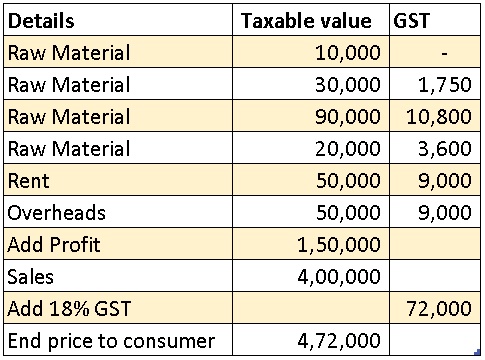

To take a very simple example: Let us assume that the monthly expenses of a restaurant are Rs 250000, on which, the restaurant is charged Rs 34150 GST by various suppliers. Thus the total purchase cost is Rs 284150. But, this Rs 34150 can be used as “ITC”. When the restaurant sells food, for egs for Rs 400000, it charges GST of 18% on the same, i.e. Rs 72000. This Rs 72000 which has been collected from customers, needs to be paid to the Government. At this point, a restaurant can utilise the ITC of Rs 34150, and instead of paying Rs 72000, can pay only Rs 37850. This can be explained with the following table:

In the sample data above, raw materials are assumed to be taxed at various GST rates such as 0,5,12 and 18% since food items are scattered all over the rates spectrum. Based on the above, if a restaurant can avail ITC, and if it charges 18% GST on sales, the end price to the consumer would be Rs 472000.

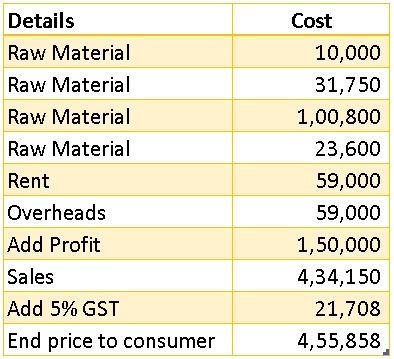

In the proposed amendment making the rate of GST as 5%, the benefit of ITC has been withdrawn. Thus, all the GST which was earlier sitting separately and was being adjusted against GST collected on sales, suddenly becomes useless. The restaurant has to now straightaway charge 5% on sales and pay that 5%, without any adjustment. So Does that mean the GST on sales would be 5% of Rs 400000 and end price to consumer would be just Rs 420000? No.

Since the GST on purchases (ITC) is now useless, it becomes part of the cost of the restaurant. As costs go up, and profit remains constant, the selling price also goes up. But this increase will be partly absorbed by reduction in the GST rate from 18% to 5%. Thus, holding all the data as above constant, and only changing the 2 conditions of ITC and 5% GST, we get this data:

Thus, although GST rate was reduced by 13%, other things being constant, the price to the end consumer reduced only by around 3.42%. This percentage can vary depending on the actual data of each specific case and the product mix, but in almost no situation will the reduction be near 13%.

At this point, it is important to understand why this change of reducing the rate from 18% to 5% was brought in. In the pre-GST era, ITC was restricted to very few items. All VAT or Service Tax paid or purchases was not freely available as ITC, and hence, lot of such tax component resided in the cost of products. As GST came in, the ITC rules were largely liberalised. Virtually any GST paid for business was allowed as ITC, thus reducing effective costs. Further, the excise embedded in goods was not available as ITC to specific industries like traders, restaurants etc, but under GST, the entire tax was available as ITC.

The Government expected that business would pass on these reduced costs to consumers by reducing selling prices. In certain well regulated sectors, and in companies run by big corporates, this price reduction was evident. Within days of GST being launched, FMCG companies either slashed the prices of goods or increased the grammage of the products. Auto companies too passed on the benefits by reducing prices.

Similarly, it was expected that restaurants and eateries would also slash prices. But do you remember eating out becoming visibly cheaper? Did the restaurants in your neighborhood reduce their prices? There may be a few, but most restaurants did not fall in line. The GST Council was also of the same view that most restaurants did not pass on the benefits of input tax credit to customers by reducing prices after GST was implemented from July 1.

Hence, since the restaurant industry was not playing fair, the Government went ahead and removed their eligibility to claim ITC, and also slashed the rate of GST to a flat 5%.

Thus, a visible fall in GST of 13% may not result in food at restaurants becoming cheaper by 13%. Worse, if restaurants continue the trend of playing hanky panky and decide to pocket the 3-5% odd benefits as shown above, then your restaurant bill may remain the same. The tax component may shrink but the overall cost may remain the same.