It was generally believed that the 2G scam which involved a presumptive loss of 1.76 lakh crore was the biggest scam of the UPA regime that ruled India between 2004 and 2014. However the biggest crisis facing Indian economy today, i.e. that of NPA (non performing assets) could been one of the biggest scams of UPA.

The corrective measures taken over a period of past three years have not only brought more transparency in the system, but also unravelled the scale of mismanagement and scam in public sector banks under Congress led UPA.

What is a non performing asset ?

Definition of non performing asset (NPA) is : a loan or advance for which the principal or interest payment remained overdue for a period of 90 days.

A loan can turn into a NPA if the amount taken by the borrower fails to generate any money from productive activities. This could be either due to failure of borrower or roadblocks to the project for which the loan is taken. For example if a highway builder is unable to acquire land from a private person in the path of the road, he will not be able to build the road in time. Thus, the loan will turn into a NPA.

The making of NPA scam

One might ask to how the NPA ‘scam’ was allowed to occur. The 2G scam was based on ‘presumptive loss’ theory, i.e. possible loss to the exchequer due to a faulty process. The theory had been validated post facto as the money raked in through transparent bidding was much higher than the earlier process.

The NPA scam is far more sophisticated and harder to detect in the eyes of a common man. It relies on three important pillars.

- Reckless lending without accounting for risks in a given project or overall economy. (Such a system is allowed to take shape when banks are forced to lend to cronies of the regime)

- Ever-greening of loans, i.e. postponing the due date of payment everytime the borrower fails to pay. This can also be done by clever accounting techniques.

- Lack of effective legal framework to ensure that NPAs don’t affect banks perpetually. This forces banks to resort to ever-greening of loans

While the first part of the scam is difficult to prove , the other two points in the scam are straightforward affairs. A RBI report titled ‘Re-emerging Stress in the Asset Quality of Indian Banks: Macro-Financial Linkages’ published in February 2014 captures the growth of NPAs under the Congress led UPA regime.

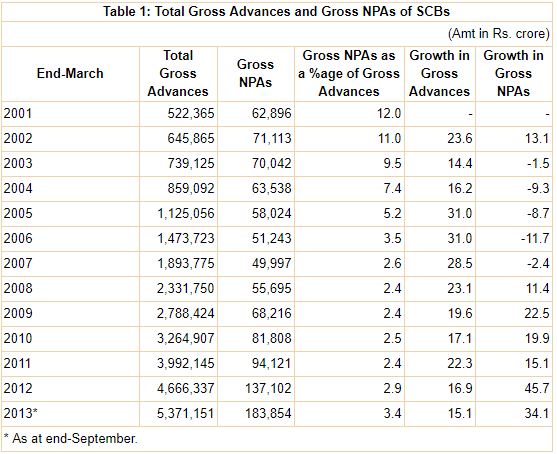

The table from the report is shown below :

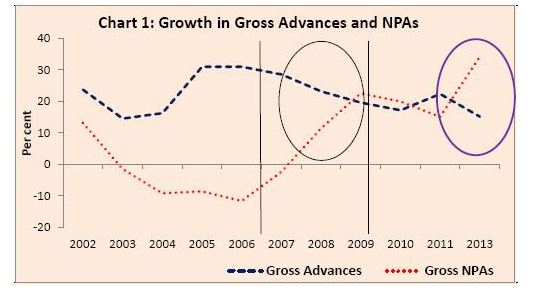

If one sees the steady growth of NPAs in absolute terms, it shows that the figure nearly trebled between 2004 and 2013 (63,538 crores to 183,854 crores) . However , in percentage terms it remained low because the overall amount lent (i.e. gross advances) by banks rose drastically. It must also be noted from the table that NPAs rose steadily after 2006 and then drastically in the 2012 and 2013 by 45.7% and 34.1% respectively. This trend is visible in the graph below.

The delay in growth of NPAs vis a vis the growth of loans is due to the fact almost no loans will turn into NPAs in the first few years. Unless there is some major event, loans are generally serviced well in the initial term, and later the loan quality drops and it turns into an NPA. This is also the time by when any efforts of evergreening have reached their limits.

The report says :

Third Phase: 2009 to 2012: During this period, growth in credit as well as NPAs slowed down in 2010. However, by end-March 2012, there was a sharp contrast in the movement of both, with credit growth witnessing a sharp contraction and growth in NPAs trending up. NPAs grew at around 46 per cent as at end March 2012, far outpacing credit growth of around 17 per cent. This widening divergence in the growth of credit and NPAs has implications for the asset quality in the near term. The decline in credit growth during this period could be attributed to the general economic slowdown that set in as a result of combination of domestic and global factors.

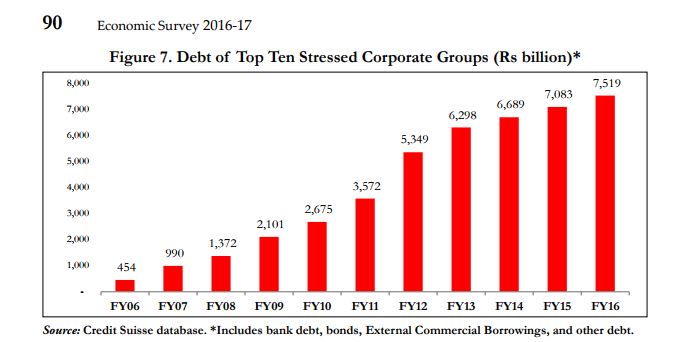

At the same time it is important to note the growth of debt in the top 10 firms of India. It must be noted that the debt of stressed firms rose from 1,372 crores to 6.689 crores in a matter of 6 years.

Source : Economic Survey 2016- 17 [ pdf ]

Thus, by the end of the Congress led UPA regime, growth had slowed down and NPAs had risen drastically. In addition to this, many NPAs were hidden under the carpet. This was bad for Indian economy in two ways.

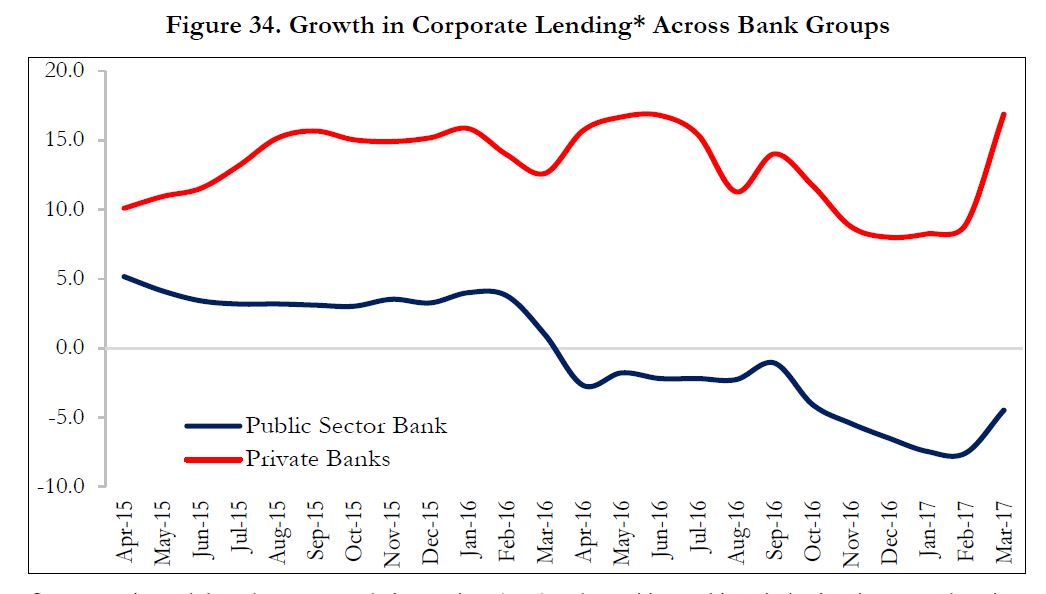

Banks are essential for growth as they fund new ventures. If they are in bad health , economy will not get credit for new ventures ( i.e. growth ) . Secondly, if NPAs are high banks will face losses and the government will have to spend money to bring them back to track. The drop in lending activities of sick public sector banks is visible below is evident

Source Economic Survey 2016-17 Part -2 [ pdf ]

Asset quality review unravels more NPAs

RBI conducted asset quality review i.e. scrutiny of loans given out by banks from 2015 onwards to uncover NPAs. This revealed that the banks had been hiding NPAs in excess of what appeared in the RBI report and data presented above. In August 2017, the government also passed an amendment to Banking Regulation Act in order to empower RBI in managing the NPA problem. After this move, more NPAs are being uncovered.

On December 6. 2017 , NS Vishwanathan told the press that the banks had not applied the rules correctly to identify these NPAs . He said : ‘We’ve assessed banks’ classification based on the rules they are today and we’ve found that in some cases, they have not applied those rules correctly.’

As a result of these exercises, there has been slowdown in growth and businesses. NPAs have risen from 3.4% in 2013 to 9.6% in August 2017. They are expected to reach 10.6% by March 2018. Measures to bring the banks back to good health have been taken by the government in the meantime. The insolvency and bankruptcy code will provide for a legal and transparent way to clear off the NPA. 2.11 lakh recapitalisation plan will bring in fresh funds for the banks to lend, thereby putting the economy back on the growth path.

NPA scam could be bigger than 2G scam

Reports suggest that the value of NPAs could be around Rs 8 lakh crores. Compare this to the value of NPA in 2013 ( i.e Rs 1.83 lakh crore). It is widely accepted that the bulk of NPAs are a part of the UPA legacy. The finance minister had reiterated this fact in Parliament earlier in the year. Thus, the difference between current NPA level and that in 2013 that could be attributed to UPA will run into lakhs of crores.

This time it is not a ‘presumptive loss.’ Only a detailed study by RBI in this regard will bring the actual figures to light. Thus, it can be said that the NPA scam is much bigger than 2G scam.