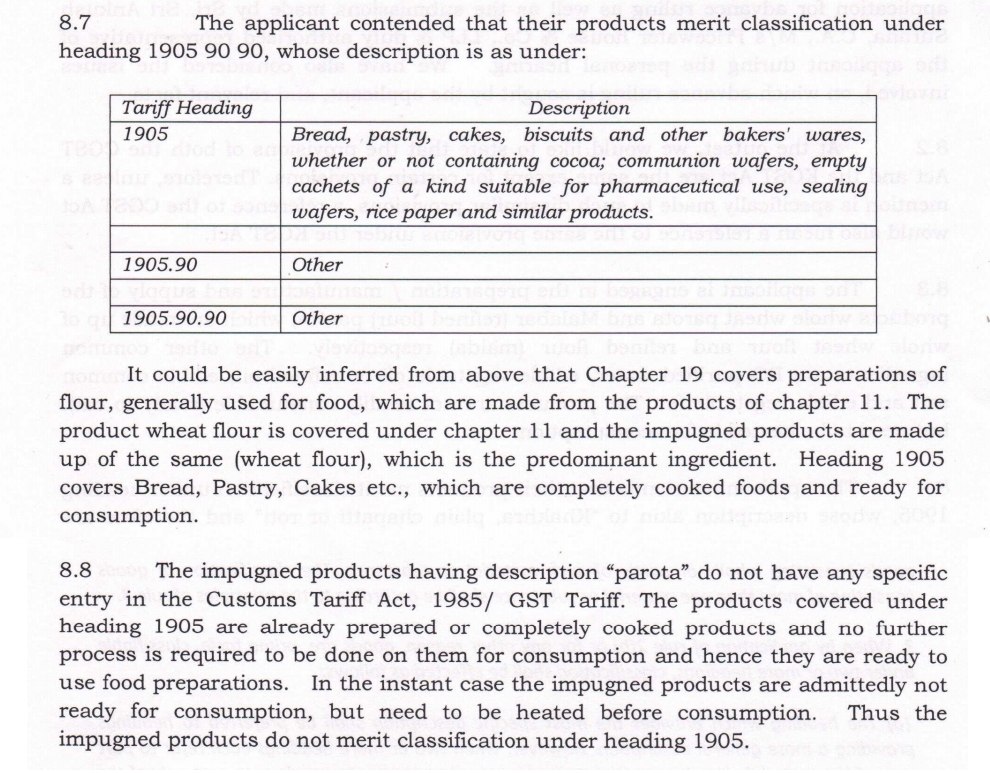

A recent ruling by the Authority of Advance Ruling in Karnataka saying that Parotas are not rotis, and hence they will attract 18% GST instead of 5%, have caused much outrage on social media. After the ruling was reported by various media houses, people assumed that they will have to higher tax if they consume parota in their favourite food joint, as compared to rotis, both being popular flatbreads that originated in the Indian subcontinent.

The kind of media reports which came out certainly made it look bizarre and unreasonable, causing outrage on social media. But the question is, was the decision bizarre or there is something more on the issue? Let us examine the facts.

On studying the order, it becomes clear that this case is a classic example of how misinformation and fake news spread, and how some media houses contribute to this by not reporting the full facts related to a matter. Because, the ruling of AAR is not at all related to the Parotas served at food stalls and restaurants. The decision by Authority of Advance Ruling is related to frozen packaged parotas manufactured by food processing industries, and it is not applicable to fresh Parotas prepared by eateries.

The ruling was issued after a Karnataka based food processing company ID Fresh Food Pvt Ltd applied to the AAR under section 97 of the CGST Act, 2017, seeking to classify their packaged Malabar parotas and whole wheat parotas (or Paranthas) under Chapter heading 1905. Items listed in chapter 1905 attract GST rate of 5%, and it includes items like khakhra, chapatti, roti, bread, pastry and other baked products. The company argued that parotas are similar to rotis, chapattis and khakhras, and they should be taxed at the same rate.

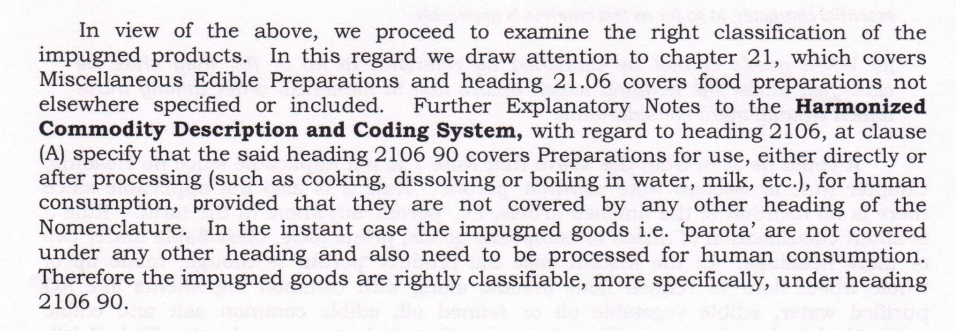

The AAR studied the matter in detail, and they ruled that the parotas sold by the company are not same as rotis and khakhras. They found that the heading 1905 covers completely cooked food products which are ready for consumption. The item Parota is not included in any list in the Customs Tariff Act, 1985 and the GST Tariff. Therefore, the authority had to analyse the item to determine the appropriate category for it under the tax rules.

The AAR found that the parotas sold by the company are not ready to eat items in the heading 1905 like rotis and pastries, and they need further processing by the consumers before eating them. Therefore, they are not ready to eat products, and will attract tax rate as applicable with other ready to cook processed packaged food products.

The AAR has determined that the packaged Parotas will come under heading 2106, and accordingly it will be taxed at 18%. The order makes it clear that it is applicable to the parotas made in the factories of the food processing company, which are kept frozen, and they need further processing by consumers before consuming them. This also makes it clear that the order is not applicable to parotas served at food stalls and restaurants, which are completely cooked products and consumers can consume them directly without requiring any further processing.

It is important to note that plain roti or parota served in a restaurant or provided in takeaway get same treatment in rates and attract 5% GST only, unlike what some sensational news reports conveyed.

It may be noted that the frozen parotas like the ones sold by the company are preserved, sealed packed, branded and are usually sold at higher price. It is not a staple food and is generally consumed by the class which could afford to pay taxes. Moreover, even items like cheaper biscuits, pastries, cakes, etc., attract GST at the rate of 18%. Frozen foods can’t be comparable to plain roti or plain parota served in restaurants.

It is a standard practise worldwide to tax processed or packaged foods at a higher rate. For example, milk is tax free, but tetrapacked milk is taxed at 5% and condensed milk is taxed at 12%. The food processing companies make significant profits on sale of packaged food items by selling them at higher rates. These items are largely consumed by those who are economically better. That is why world over such items are taxed at a higher rate.

So, there is no need to worry before ordering a parota at a restaurant, the GST on it remains same as a roti or a pastry. And, this shows how unnecessary outrage and debates are triggered by media houses by simply hiding a small but important detail while reporting.