In 2016, when India’s Non-Performing Assets (NPAs) and debt default were piling up after the ruin that UPA 2 left in its wake, the Modi government decided to introduce one of the greatest reforms in Insolvency laws that the country has ever seen. The Insolvency and Bankruptcy Code (IBC) was introduced by the Modi govt in 2016 to consolidate the process of recovery, resolve such conflicts promptly and most importantly, give more power to creditors than they held under the previous, scattered laws.

The extent of the rot was only discovered almost after a year of NDA coming to power.

“Deep Surgery” of India’s Banking system started in the second half of 2015, with RBI conducting an Asset Quality Review (AQR), a one-time special review of most of the large borrower accounts across the Banking system. AQR revealed a much higher asset quality deterioration than was earlier known. Many banks were found to be hiding bad assets under the practice of forbearance(a temporary repayment relief). AQR overrode such practices and helped determine the accurate level of bad loans that were earlier unreported by Banks. Not surprisingly, the true NPA level shot up and was projected to be INR 9.5 lakh crore in March 2018, from INR 2.78 lakh crore in March 2015. To emphasize the enormity of this crisis, INR 10 lakh crores (US $150 billion) is larger than the GDP of 130 countries.

From IMF’s 2016 data, India’s bad loans (8.6%), were much higher than other prominent economies like China, Japan, the USA or the UK where this is below 2%

To address the issue of mounting NPAs, the Insolvency and Bankruptcy Code (IBC) was passed in May 2016, which created a one-stop solution for resolving insolvencies. The greatest strength of IBC is that it set a strict time limit for cases and the process could not go beyond 270 days (9 months). Shortly thereafter in June 2016, the National Company Law Tribunal (NCLT) was constituted as a quasi-judicial body with the responsibility of overseeing the insolvency process under IBC.

What does IBC aim to do?

The aim of the IBC 2016 was to focus on the resolution of a company becoming insolvent and ensuring that the rights of the creditors are also secured.

Key aspects of the IBC are as follows:

- IBC initiates a paradigm shift from the existing ‘Debtor in possession’ to a ‘Creditor in control’ regime.

- IBC consolidated all existing insolvency-related laws as well as amending multiple legislation including the Companies Act.

- The code aims to resolve insolvencies in a strict time-bound manner – the evaluation and viability determination must be completed within 180 days. Moratorium period of 180 days (extendable up to 270 days) for the Company.

- Introduce a qualified insolvency professional (IP) as an intermediary to oversee the Process, keep the debtor as a going concern, protect the assets of the company, make sure the resolution plans are approved and sound etc.

How IBC 2016 resolved deep-seated issues in the insolvency and debt recovery process

The passage of IBC started showing results in the year 2018 when The National Company Law Tribunal (NCLT) approved Tata Steel’s resolution plan for Bhushan Steel. In May 2018, Tata Steel formally took control of Bhushan Steel settling about Rs 35,200 crore, or nearly two-thirds, of the loans owed to lenders. While the banks (creditors) took a 37% haircut the issue was successfully resolved thereby reducing NPA.

In the first two years, IBC helped resolve stressed assets worth Rs 3 lakh crore.

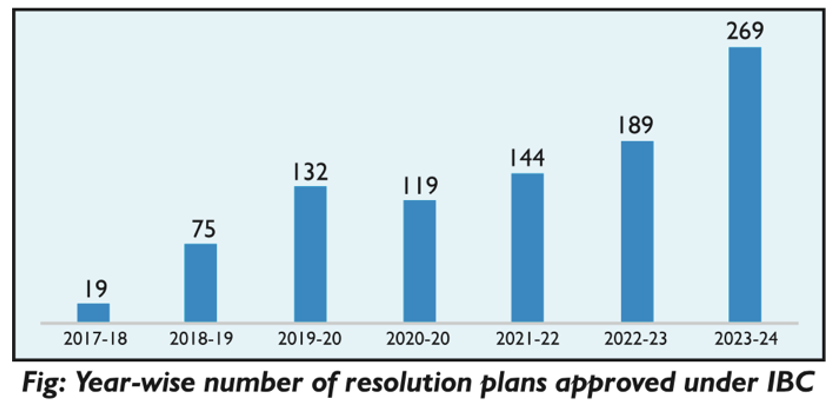

According to data from the Insolvency and Bankruptcy Board of India (IBBI), “The FY23-24 has witnessed an unprecedented surge in the approval of resolution plans under the IBC, showcasing the effectiveness of the legal framework in facilitating the revival of insolvent businesses. A record number of 269 resolution plans were approved by NCLT during FY24, as against the approval of 189 resolution plans during FY23 — indicating a significant increase of 42% from FY23. Since inception till the end of FY24, 947 resolution plans have been approved. These CDs resulted in the realisation of 32% as against the admitted claims and 162% as against the liquidation value”.

With the aim of IBC being the preservation of business by prioritizing resolution over liquidation, businesses improved their profitability and functioning after the process of resolution under IBC, according to a study conducted by IIM A.

It is important to note here that businesses are considered a ‘legal person’, which is to say that even if the original owners of a business are unable to clear debts and keep the business alive, IBC has focused on the right of the legal person (the business) to continue to be a going concern and thrive commercially, under the leadership of a different management who takes over the ailing business after the process of resolution. IBC prioritises resolution over liquidation because the process of liquidation ensures that the legal person (the business) ceases to exist with all its assets sold to repay creditors. The process of resolution, on the other hand, focuses on the continuity of the business by letting a more able management take over the company, thereby preserving the rights of the creditors as well.

The other priority of the IBC is to ensure that resolutions are completed promptly, ensuring that the process does not amount to punishment – for the business and the creditors. However, while the system provides for speedy resolution, litigation by concerned parties tends to extend the time taken for resolution.

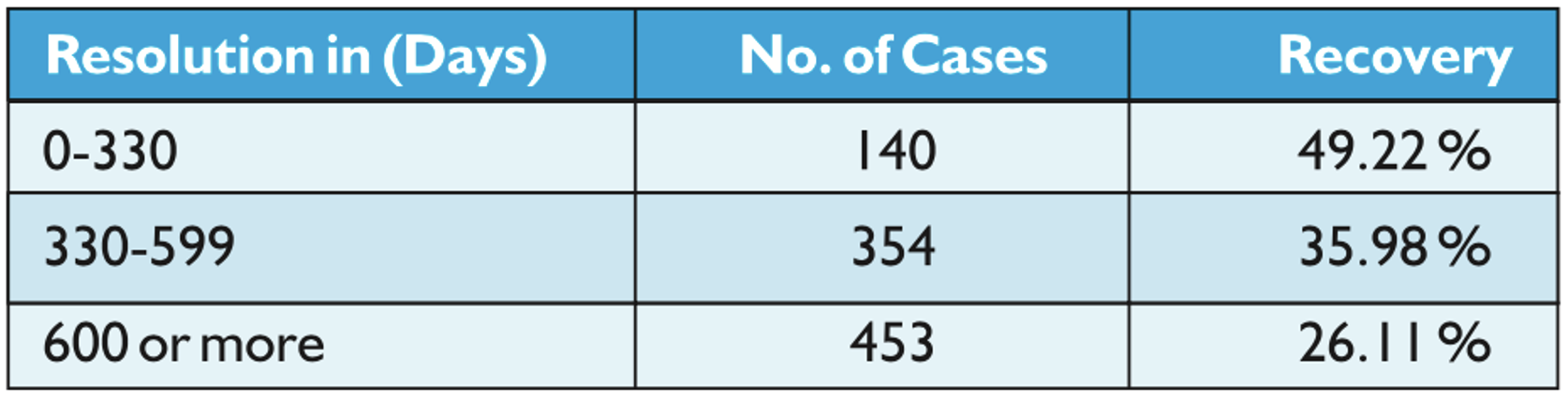

According to data by IBBI, “The resolution process, on average, is taking 679 days to conclude as against the standard timeline of 330 days. The delays often due to litigations by multiple stakeholders with competing interests, erode the value of already distressed CD further and minimize the recovery value to the creditors. Data of 947 resolved cases as of March 2024 indicates a direct correlation between the length of the resolution process and the recovery rate. Cases resolved within shorter timeframes tend to yield higher recovery rates, while the longer resolution periods coincide with diminished recovery rates”.

While the average time taken for resolution is currently far diminished compared to the status before IBC was passed, there are some loopholes which delay the process of resolution beyond just the parties involved indulging in litigation. It becomes imperative to look at certain cases where litigation was facilitated by the misuse of the IBC process itself. This article will examine the abuse of the process by certain parties involved at a later stage.

The process of IBC and the importance of the Insolvency Professional (IP)

When a company defaults on repayment of debts, the central question which arises is what is to be done with it. There are several ways in which the problem can be resolved.

One possibility is to take the firm into liquidation. Another possibility is to negotiate a debt restructuring, where the creditors accept a reduction of debt on an NPV basis, and hope that the negotiated value exceeds the liquidation value. Another possibility is to sell the firm as a going concern and use the proceeds to pay creditors. There are several other hybrid possibilities to ensure that the creditors get their due.

IBC 2016 kept the creditors as the central focus of the Insolvency Resolution Process. Essentially, the Modi govt believed that the possibilities of what should be the way forward should be the decision of the creditors, who are owed money. To that end, IBC envisioned a creditors committee, where all financial creditors have votes in proportion to the magnitude of debt that they hold. The IBC, therefore, says that when a default takes place, the Insolvency Resolution Process can be initiated by the creditors (financial and operational). This committee which was recommended by the IBBI later took shape in the form of a CoC – Committee of Creditors. In the insolvency process, other than the CoC, the role of paramount importance is that of the RP – the Resolution Professional, who is meant to play a catalytic role in the process.

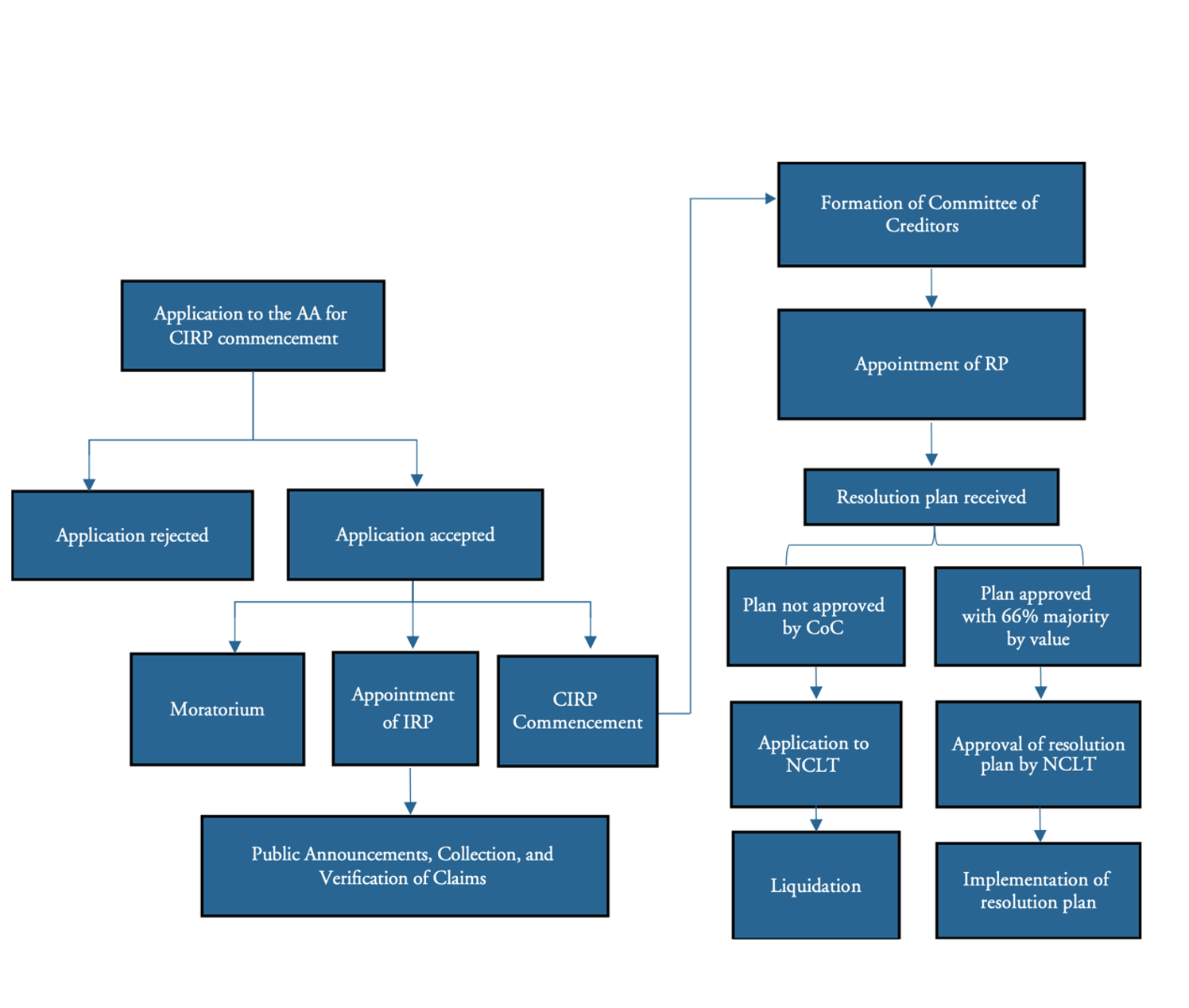

Following is a brief summation of the IBC process:

- When a company defaults, creditors (financial or operational) can apply to the Adjudicating Authority (NCLT) to initiate a Corporate Insolvency Resolution Process (CIRP).

- Once NCLT receives the application, they evaluate whether the application is to be accepted or rejected.

- The whole process of CIRP process should be completed within 180 Days from the date of admission an application extension is allowed for 90 days only one extension is allowed by NCLT However, CIRP should be completed within a period of a maximum of 330 days from the date the insolvency commencement date.

- Once NCLT admits the application, it appoints an Interim Resolution Professional (IRP)

- IRP will then constitute the CoC

- The CoC will then appoint the Resolution Professional (RP) – resolution professional

- Once the public announcement is made and resolution plans are received, if the plan is approved by 66% majority of the CoC (by value of debt), then the RP forwards the plan to the NCLT for approval. When NCLT approves, the resolution plan is executed.

- If the plan is rejected, the company goes into liquidation.

As can be seen, the Resolution Professional (RP) plays a crucial role in the CIRP. The RP is supposed to take charge of the management of the company and ensure that it remains a going concern, manage the operations of the business, be a custodian of the assets, bring the creditors together to reach a consensus and successfully conduct the corporate insolvency resolution process.

As is the state of several procedures in India, what happens when elements find a way to manipulate a just law? What happens when the RP, who is entrusted with the conduct of the resolution process abuses the process entrusted to him? What happens when private players not only hijack the pool of RPs but also manage to manipulate the CoC to benefit certain players? What happens when those meant to execute the law hijack and abuse it?

To analyse, we need to look at one of the longest-running insolvency processes in India – still to be resolved – marred by damning allegations of corruption, conflict of interest and more.

HNG case – India’s longest-running insolvency processes

The case started in 2020 with the DBS Bank initiating insolvency proceedings against Hindustan National Glass & Industries Limited (HNG) in NCLT Kolkata. Insolvency was admitted in the year 2021. Hindustan National Glass & Industries Limited is an Indian container glassmaker based in Kolkata. The company is the largest and one of the oldest glass manufacturing companies in India. In the year 2022, the CoC (Committee of Creditors) appointed Girish Juneja as the Resolution Professional.

Juneja then appointed Ernst & Young (EY) as its advisor. Essentially, EY was supposed to advise the RP to discharge his duties, keep the company a going concern, manage the affairs and functioning of the company etc. This fact would be instrumental to understanding the conflict of interest at play in this case later.

One of the creditors in the CoC was Edelweiss ARC. This fact would also be instrumental in understanding the conflict of interest at play in this case.

After the issue of Expression of Interest, Juneja received 14 bids to acquire HNG. Once the RP received the applications, on the 24th of May 2022, a Request for Resolution Plan was issued and eventually, only three firms expressed interest in purchasing HNG – AGI Greenpac (AGI), International Sugar Corporation (INSCO) and Nirma Chemical.

Before we move along, it is pertinent to note here that the IBC is an extremely robust system to ensure the market interests are protected as well along with that of the creditors. To that end, one of the rules embedded in IBC is that before a resolution plan is approved by the CoC, the company wishing the acquire the insolvent company has to take unconditional approval from the Competition Commission of India (CCI). This rule has been put in place to ensure that the acquisition does not lead to a monopolistic market situation where other small players in the same market suffer commercially.

Why is this detail important? Because AGI Greenpac which wanted to acquire HNG was the second largest Indian container glass maker, HNG (the company undergoing insolvency) is the largest. AGI (second largest) acquiring HNG (largest) would lead to a monopolistic market condition.

Now, here is where the saga of questionable conduct starts. From the court documents and other documents seen by OpIndia to expert opinions on the record, several questions have been raised on the conduct of the RP and how it may have unduly benefited AGI.

A query was raised by one of the resolution applicants in August 2022 about the proposal by AGI and the lack of approval by CCI by one of the Resolution Applicants about AGI’s proposal. To that, the RP said that the CCI approval could be taken after the approval of the plan by the CoC but before the filing of the resolution plan with the Adjudicating Authority (NCLT Kolkata).

Now, the CCI approval is mandatory per law. The watering down of this requirement by the RP has been questioned by experts since it favoured AGI Greenpac’s plan. AGI being the second largest in the industry segment, would not have got CCI’s unconditional approval and therefore, the RP’s decision to water down the mandatory provision and put the plan to CoC voting benefitted AGI. INSCO, the other bidder in the race, approached NCLT Kolkata which affirmed that the CCI approval is mandatory before the CoC approves the plan by order dated 21/9/2022.

The conduct of the RP has been deemed questionable not just by people in the know of the case but also by former judges. An opinion by Justice Sikri on the matter says, “The RP could not have given relaxation from the rules only to AGI for submitting its resolution plan to the CoC when it did not comply with the mandatory requirements of the RFRP and the RP’s emails, which otherwise was applicable to all other participants. The Resolution Plan submitted by AGI therefore ought not be considered by the NCLT since it is violative of the requirements of RFRP and mandatory requirements issued by RP”.

Justice Sikri further said, “I feel that the statutory requirement under proviso to Section 31(4) ought to be considered as mandatory, especially in cases such as the present, where if the mandatory requirement is watered down, it would lead the CD into inevitable liquidation and the same would be completely contrary to the objective of ‘maximization of value of assets of the CD and to protect the interest of all stakeholders of the CD’”.

This is an opinion that Justice Nariman agreed with. In his legal opinion, he said the RP and CoC failed to conduct the CIRP proceedings fairly and had no right to condone any mandatory provision of the law.

Even if we consider the first infraction by the RP an oversight, what happened next may point towards collaboration between the RP, who is meant to be neutral and execute the insolvency process, and AGI, which was not eligible to be in the process in the first place according to expert opinions.

AGI did seek the approval of CCI thereafter, however, there was a catch. It filed ‘Form-1’ with the CCI instead of ‘Form-2’.

Form-1 is like the ‘green channel’ of immigration. Essentially, it tells the CCI that there are no considerations of monopolistic market creation if the said company acquires the insolvent entity. Form-2 is the ‘red channel’ – declaring the scale of the company’s business.

AGI is the second largest player in the market wishing to acquire the largest player – there are clear considerations of the merger creating a monopolistic situation and therefore, AGI should have submitted their application to CCI under Form 2 – they did not. INSCO on the other hand filed Form-1 too and got the CCI approval since it is a foreign firm with no prior presence in India in this industry segment. CCI, as expected, rejected AGI’s application terming it ‘not valid’, disqualifying them from the process.

After this, ideally, INSCO would have been the only bidder for HNG since CCI rejected the application of AGI and after the third round of bidding, NIRMA had withdrawn from the insolvency process.

At this stage, the RP could have approved the INSCO plan to take over HNG, however, the story was far from over.

The authorised signatory of AGI wrote to the RP saying that the CCI had asked them to file for approval under Form 2 and that they were in the process of doing so. AGI said that they would ‘hopefully’ they would get CCI approval by November 2022. The email was sent on the 27nd of October 2022.

Based on this ‘assurance’ by AGI, the RP went ahead and put the two resolution plans by AGI and INSCO respectively to vote in the CoC. At this point, the RP seems to have wilfully circumvented the NCLT order which would bar the AGI plan to be put to a vote in the CoC, as it did not have an unconditional CCI approval yet.

AGI won the bid in CoC and INSCO lost. In the CoC, each credit can vote for multiple plans or no plan at all and therefore, the percentages don’t add up to 100%. Edelweiss, as mentioned earlier, had 4 votes. One of the votes it cast was against INSCO which resulted in AGI winning by 8.30% difference owing to Edelweiss ARC’s vote. We would also examine the role of Edelweiss in this case at a later stage.

AGI filed Form 2 for approval with CCI only 5 days after their plan got approved by the CoC. Before they got approval, the RP filed the proposal with the NCLT. It is pertinent to remember here that the RP had himself said that the CCI approval could be taken after the voting by the CoC but before filing the plan with the NCLT. While his circumvention of the CCI approval provision was overridden by NCLT, he seems to have disregarded that and filed the proposal with NCLT before the CCI approval came through. It is an agreed convention that no plan which has conditionalities can be filed before the NCLT per a judgement of the Supreme Court, however, the RP in this case seems to have acted questionably. Since the matters are sub-judice in the Supreme Court, the AGI plan is yet to be approved by NCLT.

Justice Nariman considered an authority in this field, said that the decisions by the CCI and the NCPT were bad in law. He opined, “There is no doubt that the approval to the resolution plan of AGI by the CoC and the Adjudicating Authority would be contrary to law, in as much as, it is clear that AGI was declared a successful resolution applicant on 28.10.2022, whereas conditional approval from the Commission was obtained only on 15.03.2023”.

While the RP’s role was questionable, the CCI’s conduct has been questioned as well.

For example, Glassex (India) Pvt. Ltd one of the private players in the industry wrote a letter to CCI pointing out that the combination of AGI and HNG would create an anti-competition environment in the industry – a grievance which was ignored by the CCI. UP Glass Manufacturer Syndicate also raised similar grievances, which were ignored.

When INCSO then approached the NCLT praying that the selection of AGI should be set aside, CCI seems to have contravened the law further in favour of AGI.

CCI issued a show-cause notice only to AGI when the law mandates that the CCI must seek an explanation from all parties involved in the resolution process – that is the acquirer and the company getting acquired. AGI on its part responded to CCI by saying that if the combination of AGI and HNG would lead to a monopolistic market, they could divest (sell-off) one plant of HNG – Rishikesh Plant – to ensure that the combination does not become monopolistic. Based on this modification, the CCI conditionally approved the plan by AGI.

There were several problems with this decision by the CCI, as discussed by legal experts. First and foremost, AGI has not acquired HNG yet and therefore, they have no locus standi to commit the divestment of one of the assets of HNG. The RP on his part should have also objected to this modification since during the resolution process, the RP is meant to be the custodian of the assets of the insolvent firm. The RP, its advisor Ernst and Young, the CCI and the NCLT (which later dismissed the petition filed by INCSO) – everyone seems to have erred. Interestingly, in AGI’s plan to divest the Rishikesh Plant, AGI seemed to have misrepresented the facts of the plant and HNG’s capacity. In their ‘adjusted’ plan, they had taken into consideration the current level of manufacturing by the plant instead of its optimal capacity. To simplify, if the plan was capable of manufacturing 10 units but was instead manufacturing only 5, AGI, to demonstrate that the combination of AGI and HNG would not lead to anti-competition. Now, suppose after the merger, AGI manages to run the Rishikesh plant at its optimum capacity and starts producing the 10 units it is capable of, the consideration demonstrated in this plan would not hold true.

Justice Sikri on this issue in his expert opinion says, “The modification proposed by AGI in respect of divestment of assets of HNG was also without the approval or even intimation to the CoC of HNG. The CoC ought to have considered the resolution plan of AGI with complete disclosures. This is also the mandate under Section 30 of the Code read with 38 of the IBBI (CIRP) Regulations, 2016”.

He further says, ‘The subsequent modification of the plan by the successful resolution applicant after approval by the CoC but before the approval by the NCLT, is a serious irregularity of the provisions of the IBC Code. Such an irregularity cannot be cured ex-post facto by virtue of the NCLT requesting the CoC to peruse the modification proposed by AGI which was not challenged by the CoC”.

Justice Sikri in his opinion was, in fact, scathing towards the RP.

In his opinion, he says, “The actions of the RP have given an undue advantage to AGI over remaining resolution applicants, especially INSCO”, further calling the actions of the RP “prejudiced” and “partisan”.

Thereafter, there were several complaints filed against the conduct of the RP, the decision of the CCI and the abuse of process in the case. INSCO, which should have been awarded the acquisition of HNG in the first place approached the Supreme Court and the case is pending hearing.

The questionable role of Ernst and Young

There appears to be a conflict of interest Pandora’s box, inside which, the main players seem to be Edelweiss Group, the leading financial services company of Mumbai and Erst and Young (EY), a multinational financial services company.

First and foremost, it is pertinent to remember that EY was hired as the advisor of the RP. The RP’s role has been deemed partisan and biased by legal luminaries who have given their expert opinion on this case. From Justice Nariman to Justice Sikri, Justice Ramana and others have opined that the conduct of RP is questionable, with several laws contravened by him.

The central question that arises at this stage is why EY, as the advisor to the RP, at no stage raised questions about the laws being contravened by the RP and the partisan approach being adopted in the insolvency process.

There is no document on record which can prove that EY raised these issues with the RP or the relevant authorities.

There are 5 central issues in which the RP seems to have strayed:

- Putting AGI’s plan to vote in the CoC without the approval of the CCI

- While putting the AGI’s resolution plan to vote in the CoC, the RP should have made a full disclosure to the CoC regarding the plan not receiving approval from the CCI, so the CoC could make an informed decision. This was not done by the RP.

- Not only the CoC, but the RP also misled the NCLT, Kolkata by filing the compliance certificate i.e., Form-H with wrong information by stating that there are not contingencies in the resolution plan approved by the CoC.

- The change in the resolution plan with respect to divesting the Rishikesh Plan was also flawed in law. The information provided to circumvent to combination creating a monopolistic situation was also inaccurate. The RP in Form H claimed that the plan of AGI had no contingencies, while clearly, the divestment of the Rishikesh Plant was a contingency in itself. Interestingly, in clause 11 of Form-H, the RP stated that CCI approval must be obtained “prior to CoC approval or prior to filling of application for approval of resolution plan” and has further stated “on the basis of email dated 27.10.2022, the time frame proposed for obtaining CCI approval is November 2022” which makes it clear that there was a condition which was to be followed before approval from Adjudicating Authority and admittedly AGI failed to comply with the said condition before filing of application for approval by Adjudicating Authority. Further, Under Clause 12 of Form H, RP has mentioned “The Resolution Plan is not subject to any contingency” while the plan did not have any CCI approval as on the date of filing of the Resolution Plan and Form H before the Adjudicating Authority.

- Recently, in January 2024, there was a fire at the Nashik plant of HNG. The Industrial Safety and Health Department of Maharashtra conducted a probe into the fire and in its report to the Chief Judicial Magistrate has revealed that the fire fighting equipment at the plan was lying in a scrap condition. The employees of the plan have squarely blamed the RP (Juneja) for the fire at the plant. A petition by the workers of the plant in the NCLT Kolkata claims that despite there being Rs 300 crores in cash and a substantial bank balance in HNG, the CoC and the RP have not undertaken urgent and pending repair work of the plant. The police complaint by one of the supervisors with HNG says, “Mr. Juneja and Mr. Ramchandra Une started working against the interest of the company and started damaging the company’s property illegally and betrayed the company. As a result, the company suffered losses and both Mr. Juneja and Mr. Une benefited. The duo conspired to carry out illegal transactions to benefit themselves at the expense of the company. To avoid opposition from the local Staff they transferred them or forced them to resign, because of that the Staff suffered”. Further, the complaint says, “Both Mr. Une and Mr. Juneja are selling all scrap materials burnt due to fire in the company as well as unburnt valuables by making very low price bills and taking the remaining amount in cash from the respective customers. The scrap material is worth crores of rupees and out of that Mr. Une and Mr. Juneja are embezzling crores of rupees”. There are also allegations of the RP (Juneja) clearing the bills of some of the creditors selectively. The complaint says that Ramachandra Parasram Une was the Unit Head of Hindusthan National Glass & Industries Ltd., Sinner Plant and he retired in 2023 but was reappointed as Unit Head by Mr. Juneja. and is responsible for the day-to-day operations and safety of the plant and for safeguarding the interests of the company and its permanent employees as well as the safety and welfare of the workers.

In this entire fiasco where the RP is alleged to have compromised the interest of the HNG, the assets and working of which he is meant to oversee, EY seems to have maintained studious silence. There has been no complaint by EY against the RP and no communication, at least on record, to indicate that EY, at any point, attempted to stop the RP from functioning in this manner.

The questionable role of Edelweiss – gross conflict of interest?

As mentioned earlier, the difference in the voting of 8.3% in the votes of INSCO and AGI is because of Edelweiss ARC which only voted for AGI on the CoC voting held in October 2022. In the Rs 3,500 crore debt of HNG, Edelweiss ARC was the second largest creditor after SBI. Its exposure increased after it acquired securities from HBSC, taking its exposure to 24%. After Edelweiss’ structured deal, it became the second largest credit, thereby, its say in the CoC also became far more pronounced.

This would not have been a point of contention had certain revelations not come to the fore.

On March 20th, journalist Palak Shah published a report in BusinessWorld which outlined how Edelweiss Group was also the funding partner of AGI Greenpac, in favour of whose resolution plan Edelweiss ARC voted.

This revelation was made during the proceedings in the NCLT when a letter came to the fore, from Edelweiss Alternate Asset Advisors to AGI promising Rs 1,100 crore for the acquisition of HNG. In fact, one of the key clauses of the funding which Edelweiss was providing to AGI Greenpac was that the funding would only be approved if their proposal was approved by the CoC. What was also revealed during the NCLT proceedings was that someone in the CoC, according to the minutes, had objected to Edelweiss ARC voting in the CoC, however, the RP had overlooked that objection.

Interestingly, during the CoC meeting, the RP had told the creditors that Edelweiss had submitted 4 different claims and therefore, it would have 4 votes instead of the 1 combined vote.

There are several points of breach of trust and conflict of interest that arise from the conduct of Edelweiss;

- Since Edelweiss was financing AGI Greenpac with Rs 1,100 crores to acquire HNG, Edelweiss ARC in the CoC had a clear motive to ensure that AGI’s proposal is adopted despite the illegalities and omissions.

- Edelweiss had ensured that they would fund AGI with Rs 1,100 crores only after the proposal was accepted by the CoC.

- The RP is appointed by the CoC, as was the case in HNG as well. With Edelweiss’ increased exposure, it had a greater say in the appointment of Juneja as RP who then ensured that Edelweiss got 4 votes instead of the 1 combined vote. Juneja also overlooked the objection in the CoC. In such a scenario, one wonders if this mutually beneficial arrangement, could be argued as hinting towards some quid pro quo.

- As a part of the funding deal, according to the BusinessWorld report, Edelweiss was to get non-convertible debentures of HNG. This would indicate impropriety on the part of Edelweiss since it would benefit financially with AGI’s plan being accepted.

- Edelweiss was essentially on both sides of the deal – funding AGI to acquire HNG and also voting in HNG CoC to ensure that AGI’s proposal was passed. This points towards conflict of interest.

It would appear from the facts revealed by BusinessWorld that Edelweiss, the RP, AGI and EY were in some sort of an agreement to ensure that the resolution process goes in a certain direction, regardless of aspects that circumvented the law.

The problem of the IBC process being hijacked and manipulated by private players like EY and Edelweiss

As is the norm in India, it is often not the law but the implementation of the law that leaves much to be desired. The IBC was passed by the Modi government to ensure transparency of the process and also, ensure the security of the creditors – giving them a say in how the process of resolution proceeds. Despite the law being well-intentioned, certain loopholes get invariably hijacked and manipulated by motivated private parties, ending with a gross abuse of the process. In the process, those entities who could benefit the insolvent going concern and the going concern itself suffers.

EY is a multinational company with decades of expertise working in the field, in India and across the world. It would come as no surprise that EY would have a close working relationship with most RPs in the system, given their professional network and decades worth of work. However, what becomes abuse of the process is when that professional proximity is manipulated to benefit certain parties.

Edelweiss, just like EY, is a financial company with decades of experience and work in the segment and undoubtedly, it knows how to use the loopholes in the system, as is evident from this case.

There are also indications that this apparent collaboration is not new.

In 2021, the NCLT ordered the liquidation of debt-laden ship-builder Bharati Defence and Infrastructure Limited. In the order, the NCLT made damning observations against EY and Edelweiss ARC. Citing conflict of interest, the NCLT removed Dhinal Shah, a partner at Ernst & Young and the resolution professional (RP) for Bharati.

NCLT observed that EY was engaged by Edelweiss ARC (whose resolution plan was thrown out by the insolvency court) through a service agreement. The Committee of Creditors (CoC) — in which Edelweiss had an 82.7 per cent voting share — cleared the resolution plan of Edelweiss before it was brought to the NCLT for approval.

According to a report in BusinessLine, the order said:

“The RP admitted that E&Y provided support services to him during the corporate insolvency resolution process (CIRP). Further, RP has delegated his authority and duties under CIRP to Dinkar Venkatsubramaniam by a Power of Attorney. Dinkar Venkatsubramaniam is also a partner of E&Y Restructuring LLP.

Further, E&Y was given the mandate of investment banker for the corporate debtor (Bharati) to find investors. From the records submitted by the parties, it is noted that the disciplinary committee of the Insolvency and Bankruptcy Board of India (IBBI) after issuing show cause notice and an opportunity of hearing, imposed a penalty of ₹1 lakh on Dinkar Venkatsubramaniam on August 23, 2018, in another insolvency matter of JEKPL Pvt Ltd. In spite of disciplinary proceedings initiated by IBBI, RP has delegated his power to Dinkar Venkatsubramaniam.

The resolution plan has not given due consideration to the interest of all the stakeholders.

It is noted that E&Y/E&Y LLP is providing entire service in the current CIRP like a single window system — the RP Dhinal Shah is partner of E&Y, the Power of Attorney holder Dinkar Venkatsubramaniam is also from E&Y, RP’s team members are also from E&Y, the investment banker appointed during the CIRP is also from E&Y.

“This creates a conflict of interest. We believe that the RP and CoC have failed to ensure appropriate checks and balances and failed to implement ‘Chinese wall’ concept during the entire CIRP. Further, this will also act as a monopoly in the entire CIRP, which needs to be examined by IBBI. Therefore, we direct IBBI to examine this issue and to frame suitable guidelines,” Ravikumar Duraisamy and V P Singh wrote in the 14 January order.

Interestingly, the erstwhile promoters of Bharati told the court, “The applicants believe that the resolution plan submitted by Edelweiss ARC is the plan prepared by E&Y under the service agreement. In such case, the RP and Edelweiss ARC cannot be said to have duly examined the resolution plans submitted by all resolution applicants without bias and prejudice. Further, it is evident that E&Y has been directly/indirectly managing and conducting the CIRP and has done so in a manner to favour EARC and EY itself,” the former promoters said.

This case has stark similarities with the HNG case we have used as a case study with some operational differences. While in this case, the RP was directly employed by EY and the resolution plan which Edelweiss ARC voted on as a part of CoC was prepared by EY too. In fact, the RP in the case was of EY as well.

In the case of Bharati Defence, the NCLT exposed a nexus between Edelweiss ARC, EY and the RP in question – a conclusion that might hold similarity with the HNG case as well.

It is also obvious that EY and Edelweiss (ARC or the Alternate Asset Advisors Limited – both of which are involved in the HNG case) work together on multiple occasions and therefore, have professional camaraderie, to say the least.

In this case, for example, it is on the EY website itself that they were working together with Edelweiss Alternate Asset Advisors Limited. EY says that it advised several entities of Adarsh Group to raise Rs 550 crores from Edelweiss. While this case has no illegality, it only goes to show the professional working relationship between the two firms.

There are other cases where the authorities found conflict of interest between Edelweiss, EY and the RP as well.

With a long history of evidence towards the conflict of interest between EY, RP and Edelweiss, there are several questions that plague the IBC process which needs not only to be answered but also addressed by the authorities as far as the larger policy is concerned.

- Is there an active collaboration between firms like EY and Edelweiss to subvert the IBC process, which is built for transparency and fairness?

- Is there a need to legally build a Chinese wall between the RPs and such financial institutions which are in a position to affect the decisions taken by said RPs in the resolution process?

- Should the IBC have specific clauses which mitigate risks of conflict of interest as seen in several cases?

- Should private financial institutions be allowed to act as advisors to the RP when they, often, have a professional relationship with the said RPs?

- Should employees of private financial institutions be allowed to act as RPs, given that their employment may affect the impartial and non-partisan approach they are meant to have?

These are policy loopholes that are being manipulated, rampantly, in the IBC process, marring the objectives of a law that protects creditors and the going concern. Perhaps it is time for the government to fine-tune the law to plug the last remaining loopholes in an otherwise transparent and fair process.