A lot of unnecessary noise is being created on the “bail-in” clause in the Financial Resolution and Deposit Insurance (FRDI) Bill. Many articles have been published, which claim that deposits of the customers would be put under severe risk, if this Bill was implemented as an Act as it is.

One of the sites at the forefront of this fear-mongering was “The Logical Indian” (TLI). On 4th December, an alarmist post titled “Banks Can Wipe Out Your Money” was published by the website. We had already done a detailed fact-check on the issue as a whole, but since The Logical Indian has posted a rebuttal, it is essential to clear the air one more time, step-by-step.

The 4th December article says:

Under Section 52 of the FRDI Bill, the powers of the Resolution Corporation are so extensive that it can cancel a liability of a bank — which means that it can declare the bank doesn’t owe you any money though you have deposited your hard earned money with it. Under the same section, it can modify or change the form of liability — the import of it is that if you have deposited say Rs 10 lakh for 5 years intending to use the money for your child’s graduation or marriage, the corporation can convert it into a locked-in deposit of 20 year tenure without your consent. The Bill also has a provision that allows the RC to exempt the failing bank for fulfilling its obligations under a contract or an agreement.

In simple words, it means that your savings account balance of Rs 15 lakh can be reduced to Rs 1 lakh, the maximum covered by the 1961 deposit insurance law. Or they can convert your SB balance of Rs 15 lakh to a fixed deposit, repayable after five years, giving you of five per cent annual interest.

The above paragraphs say:

a. Section 52 of the FRDI Bill can cancel the liability of a bank towards “you”, i.e. it can wipe out your “hard earned money” deposited in banks, by enabling the Resolution Corporation to say, the bank does not owe you “any money”.

b. Section 52 of the FRDI Bill can convert the liability i.e. a 5 year FD can become a 20 year FD, thus the article indicates that in this case, the bank will still be liable to repay the depositor, but over a longer period.

c. The article also says that via the FRDI bill, the deposits “can be reduced to Rs 1 lakh”, which is the maximum covered under the deposit insurance law of 1961. They are referring more specifically to the Deposit Insurance and Credit Guarantee Corporation Act (DICGC) which currently provides a maximum of Rs 1 lakh as insurance coverage for a deposit.

Let us check the claims in reverse order.

Point (c) infers that the FRDI Bill (when passed) and the DICGC Act will work in tandem. This is not possible since the FRDI Bill repeals the DICGC Act, because the functions of the the DICGC Act (primarily deposit insurance) will now be performed by the FRDI Bill (The DI in FRDI stands for Deposit Insurance). So once the FRDI Bill kicks in, deposit insurance cannot be Rs 1 lakh as stated by DICGC Act.

So what will the new insurance amount be? The FRDI Bill has not specified this in the bill. Here we need to know that this Rs 1 lakh limit was fixed 24 years ago in 1993. Prior to this, the insurance amount was set at a measly Rs 1500 in 1961. The insurance amount increased by 66 times over 32 years. Does any rational person still think and believe the insurance amount will remain at Rs 1 lakh in the new FRDI bill? The current FRDI bill has a provision which allows the Resolution Corporation to set the insured amount in consultation with the RBI.

Why isn’t the amount specified in the Bill itself? Firstly, the bill is presently under consideration of the Joint Committee of Parliament. The Joint Committee is consulting all the stakeholders on the provisions of the FRDI Bill. One may see the amount fixed in the final Bill. Secondly, fixing such amounts in a Bill is generally looked down upon. Take the case of GST, where Congress wanted an 18% cap enshrined in the GST Act. If this was done, any time this amount needs to be increased the Government has to amend the Act which takes more procedure. Similarly an insurance amount in the FRDI Bill would be significantly inflexible as compared to the insurance amount specified in other documents. In any case, speculating or claiming that the amount will be Rs 1 lakh is wrong.

Next, point (b) states that a 5 year FD can be converted to a 20-year-instrument. This point read with point (c) states that only the amount over and above the deposit insurance limit, will be converted to a long-term instrument. Now we quote from another article by TLI, on the same issue, published on 5th December, which states the present situation (emphasis added):

That law guarantees the deposits would be under the insurance cover for up to Rs 1 lakh, including interest. This means that the payment of all deposits up to Rs 1 lakh are protected even if the bank collapse. But anything over and above Rs 1 lakh does not have this protection. So, if the bank scuttles, a bank account holder with a large deposit might lose a lot of money.

So TLI states that today if a bank goes bust you get nothing over and above the insurance limit (of Rs 1 lakh). But in case a bank goes bust in FRDI bill regime, you get the insurance amount (unspecified) and the balance gets converted into a longer term instrument (i.e. money is not lost). Which would you prefer? Losing everything above the insurance limit? Or having the bank owe you the money over and above the insurance limit? Doesn’t this make the FRDI Bill, even in its current form, better than what we face today? Has TLI highlighted this explicitly, that the FRDI bill improves the position for depositors (although the position is not perfect)?

Third, at point (a) TLI says Section 52 of the FRDI bill can cancel a bank’s liability towards you, the depositor. To quote TLI, they say, the Resolution Corporation can declare the bank doesn’t owe you any money. For this, let us see Section 52 in depth. Section 52(2) states that a Bail in instrument or scheme shall contain a “bail-in provision”:

Next, Section 52(3) states what a “bail-in provision means”:

TLI’s point (a) comes from the Sec 52 (3) (a) above, which states a bail-in provision means a bank (specified service provider) can cancel a liability it owes.

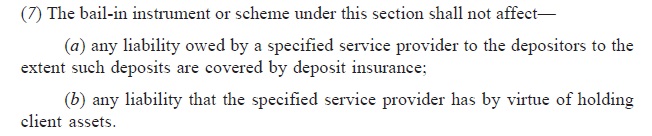

Now, we move to Section 52(7) which neither TLI, not any other media report has mentioned:

Section 52(7) clearly states that the bail-in instrument i.e. the bail-in provision i.e. the provision to cancel liabilities owed by banks DOES NOT AFFECT any liability owed by a bank (specified service provider) to depositors, upto the deposit insurance limit. Thus in any situation, depositors will always get the deposit insurance limit. Then how can the bank, as claimed by TLI, wipe out your “hard earned money” deposited in banks? How can the Resolution Corporation declare the bank doesn’t owe you any money. Is this not fear-mongering?

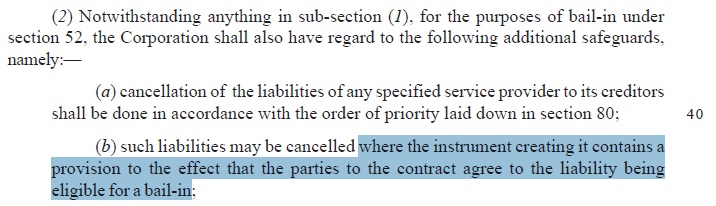

Further, Section 55(2) of the FRDI Bill states that any cancellation of liabilities can be done only if the the instrument creating such a liability, states that the creditor agrees to be eligible for such bail-in :

In simpler terms, in case the bank’s liability towards an FD is to be cancelled, the document creating the FD should state the depositor is agreeing to the bail-in. Thus, consent of the depositor is needed. Even once such clause is in place, thanks to Section 52(7), the FD amount up to the deposit insurance amount cannot be cancelled under any circumstances.

After our original fact-check, TLI added a “rebuttal” to our article, which focused on trivial issues. When our article stated that the FRDI bill is being brought to salvage the situation IF something goes wrong, TLI mauled it by claiming that we were trying to say “nothing will go wrong”. Having said that, TLI itself states that since 1961, no such bank collapse has happened in India. We let the reader judge the probability of the same. The rebuttal at no place acknowledges that they “missed” section 52(7). Instead of speaking on the law and facts, the rebuttal focuses on hypothetical arguments such as “what if the bill is passed as it is”.

Finally, the Finance Ministry in a press release stated clearly, its intent, with regards to the FRDI Bill. The ministry has stated that the bill provides additional protections to the depositors in a more transparent manner and is far more depositor friendly than many other jurisdictions.

Having said all of the above, is the FRDI Bill perfect? No. Which is why it is still under consideration of the Joint Committee of Parliament, which is consulting all stake-holders. But is it better than the existing situation? Yes, since as explained above, currently you stand to lose all your money above the insurance limit, but the FRDI Bill makes sure that money above the insurance limit is still owed to you by the bank. Is the insurance limit better? We do not know, but we must ensure, by appealing to the Government, to set it at a substantial level, by increasing it multi-fold, as it did from 1961 to 1993.