Every few months, we witness hysteria on social media regarding loan write offs. Almost exactly a year ago, a social media rumour claimed that SBI had “waived off” Mallya’s and other wilful defaulters’ loans, to the tune of Rs 7000 crore. This was based on an article in DNA.

Now, a similar article has sparked off similar reactions. The Indian Express has carried a news article titled: “PSU banks write off Rs 55,356 crore in six months“. There may be nothing factually wrong with this, but readers and politically inclined people are either misunderstanding the term used, or are deliberately spinning it.

Yogendra Yadava and Comrade Yechury have compared these write-offs with waivers, indicating that while farm loan waivers are scorned upon, “waivers” given to corporates are fine:

Small loans of farmers are not waived, but loans of over Rs 1,00,000 cr expected to be written-off in Fiscal 2018. No disclosures. Modi and his govt speak of the poor but help only rich defaulters. #NoTransparency pic.twitter.com/ETnVR5hc8C

— Sitaram Yechury (@SitaramYechury) December 4, 2017

Please remember this figure when hear outcry against farm loan waiver.

Total write-offs in the last year and half: Rs 1,32,659 crore.

https://t.co/Yw7aeCWJ6A via @IndianExpress— Yogendra Yadav (@_YogendraYadav) December 4, 2017

Congress leader Arjun Modhwadia has used this news to land the “suit boot ki sarkar” jibe, indicating that these “waivers” are helping corporate India

Banks have written off loans worth ₹55,356 crore in the first six months of fiscal 2017-18, – 54% higher than the ₹35,985 crore written off in the same period last year – & Then PM wonders why @INCIndia & Rahulji calls this Govt ‘Suit-Boot Ki Sarkar’https://t.co/cG7B1kF5tV

— Arjun Modhwadia (@arjunmodhwadia) December 4, 2017

A JNU-ite, displaying his knowledge, asks whether there is a “ghotala” (scam)

Indian Public Sector banks wrote off loans worth Rs 55,356 crore in the first six months of fiscal 2017-18, 55% more than same period last year! Total write offs in 2016-17 stood a whopping Rs 1,32,659 crore! Koi Ghotala hua hai Mitaron? https://t.co/QrZaMW91lH

— Samar (@Samar_Anarya) December 4, 2017

So what is this write-off? Is it really a loan waiver, a sweet deal given to errant corporates?

For this we need to understand what write-offs are. A balance sheet should reflect the real position of assets and liabilities. Hence Banks have to write off loans given to borrowers, which are “assets” to the banks, which have now shown signs of weakness. If they don’t write off loans, it is like claiming to hold a high quality asset, when actually the quality has deteriorated. Will you trust an entity that doesn’t give the true picture of its assets?

Secondly, if a loan is not written-off and is continued as a healthy asset (when it actually is an Non Performing Asset), then banks can continue to book interest income on the loan, on accrual basis of accounting. This has two impacts: Firstly, the bank is artificially increasing its income by booking interest on accrual basis, income which it may or may not receive (since the loan is actually an NPA). Secondly, the bank has to pay tax on such interest income. Both are undesirable. A write off prevents banks from doing this, since once a loan is “written-off”, income booking on the same is based on actual receipt of income, and not based on accrual. Banks do not stop earning interest on such loans, but now they can recognize it as income only when they receive it.

Hence write-offs are a purely technical, accounting entry. Loans, which may not be repaid by the borrower in normal course of business are written off. Even when these loans are written off, various recovery procedures like recovery suits filed before the DRT/ Court. and action initiated under SARFAESI Act continue. Now, the bank takes control of the assets secured against such loans and sells them off to recover the loans.

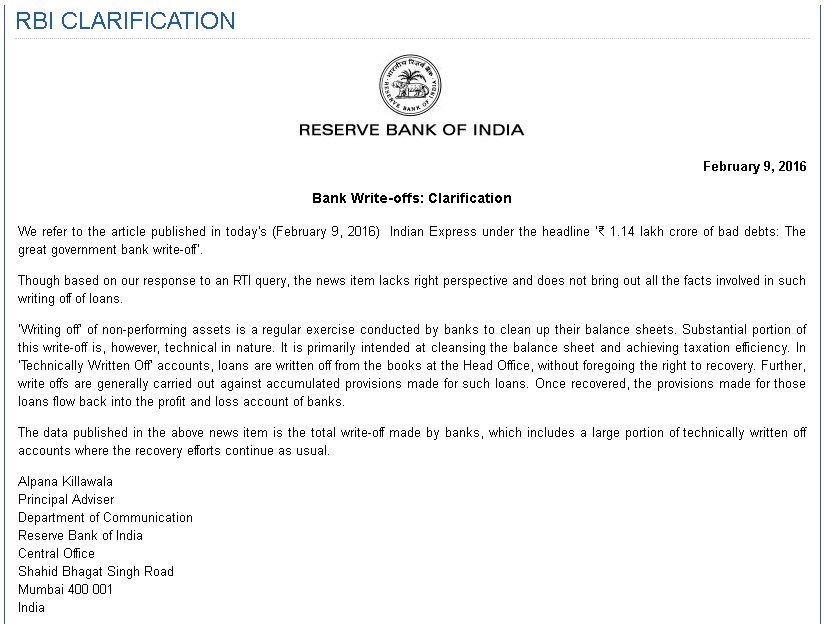

So a write off means the loan has been waived? Definitely not. Even the RBI had issued a clarification in February 2016 (Raghuram Rajan headed the RBI then) stating exactly what we have explained above:

The RBI, now and even during Raghuram Rajan’s tenure, has been a big votary of this clean up process. The RBI has been constantly monitoring the write-offs by banks, and adding to the banks’ own write-off amounts whenever it has felt necessary. Rajan has recently stated that he felt banks were “scared” of writing-off loans, which they ideally should have written-off.

The people who have shared today’s Indian Express article, would have been better served if they had bothered to read the piece. The same report quotes an RBI explanatory note which states that a substantial portion of the write-off is, technical in nature:

“It is primarily intended at cleansing the balance sheet and achieving taxation efficiency. In ‘Technically Written Off’ accounts, loans are written off from the books at the Head Office, without foregoing the right to recovery.”

Former chairman and MD of Indian Overseas Bank, M Narendra,’s views are also reported in the same piece:

“The write-off is just a technical book entry. Banks are not losing anything. It doesn’t mean banks are giving up those assets. They will continue with various recovery methods.”

In an ideal world, write-offs would not be needed. Loans given would be repaid back in time. But write-offs are needed right now since loans given earlier, are now showing signs of weakness, and accounting prudence, RBI guidelines, and Tax efficiency demand that such loans be “written off”. These “write-offs” are by no means a “waiver”.