Every discussion on rupee is driven by political rhetoric (and opportunism) which makes the discussion lose its objectivity in terms of looking at the economic implications of rupee as a currency. For all practical purposes, much of the discussion on the rupee is governed in terms of how people view it as an indicator of the economic situation within India- just as they do with the stock markets.

Here’s an important economic fact that’s worth stating; neither the rupee (domestic currency) nor the stock market help us make a definitive conclusion regarding the economic health of India (or any other country).

Therefore, what the “Rupee” does not tell us is the situation of the domestic economy and it in no way reflects the growth prospects of the economy. The question, does arise then, why is a falling rupee bad for India? The answer is that India is a net importer of goods and services so with a weaker rupee we may have to pay more rupees to get the same dollar worth of goods. This also means that our exporters would benefit from a weaker rupee as their goods become competitive in the international market. So, does rupee serve as the sole indicator of the competitiveness of domestic goods? Not really, but it is definitely one of the important indicators that determine the competitiveness of domestic goods on the external front.

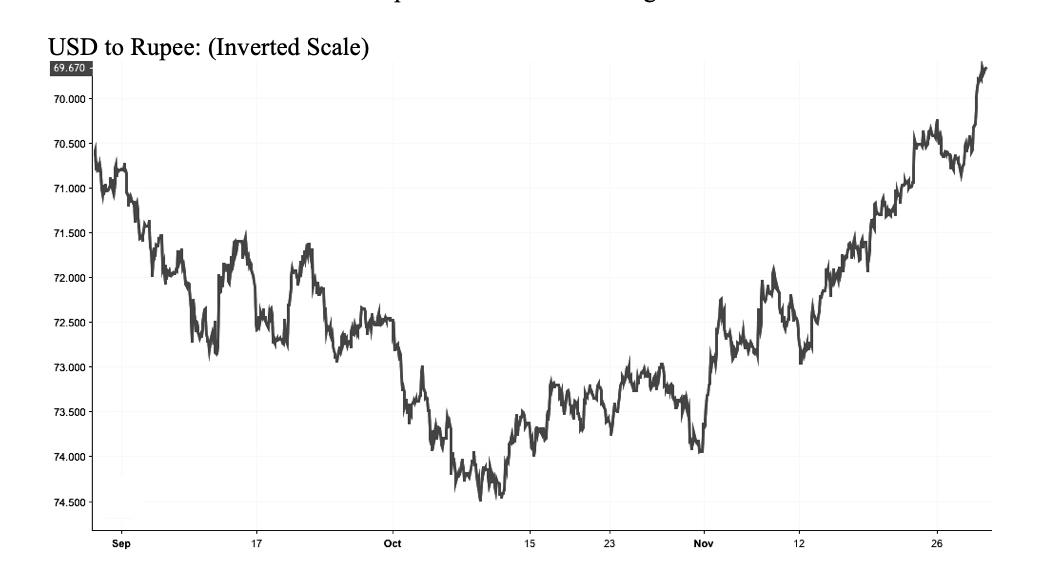

USD to Rupee: (Inverted Scale)

Politics aside, why is the rupee all of a sudden strengthening? The answer to this has a lot to do with the crude oil prices. A reduction in the price of oil is largely driving the rally of the rupee. In fact, it is this factor that has also resulted in most analysts predicting a moderation of the current account deficit signalling that the short-term downside risks to Indian Economy have largely been mitigated. Thus, there is a considerable long-term relationship that exists between Oil Prices, Rupee’s value and Current Account Deficit for obvious reasons. This relationship comes from as much of economic literature as it does from empirical evidence and it suggests that Oil Prices tend to cause an effect on the value of rupee and both these factors collectively determine the current account deficit.

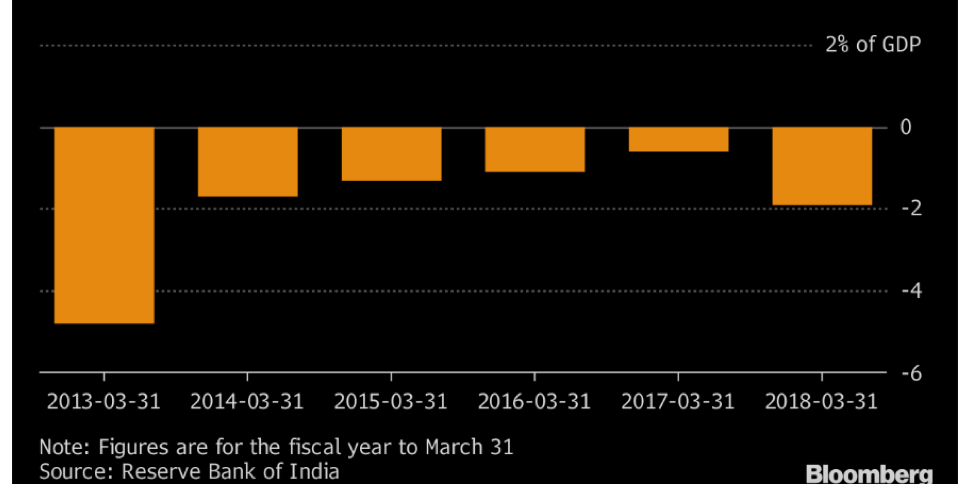

Current Account Deficit as a percentage of GDP

With these well-established facts, can we take rupee to be an indicator of the economic health? Absolutely not as the government has no control over the international crude oil prices that tend to have a disproportionate impact on the value of rupee. Besides oil prices, another important factor that determines the value of rupee is capital mobility and capital movements have two aspects, the “hot-money” that is invested in highly liquid assets as against foreign direct investments that tend to be more long-term in nature.

Capital Movements in the economy has been fairly decent over the last couple of months despite increasing returns and the strong growth being registered in the American Economy. What this tells us is that there is an optimism around the prospects of the Indian Economy and this was confirmed even by RBI as it found through one of its surveys that Indians had a more positive outlook for the economy for the next year.

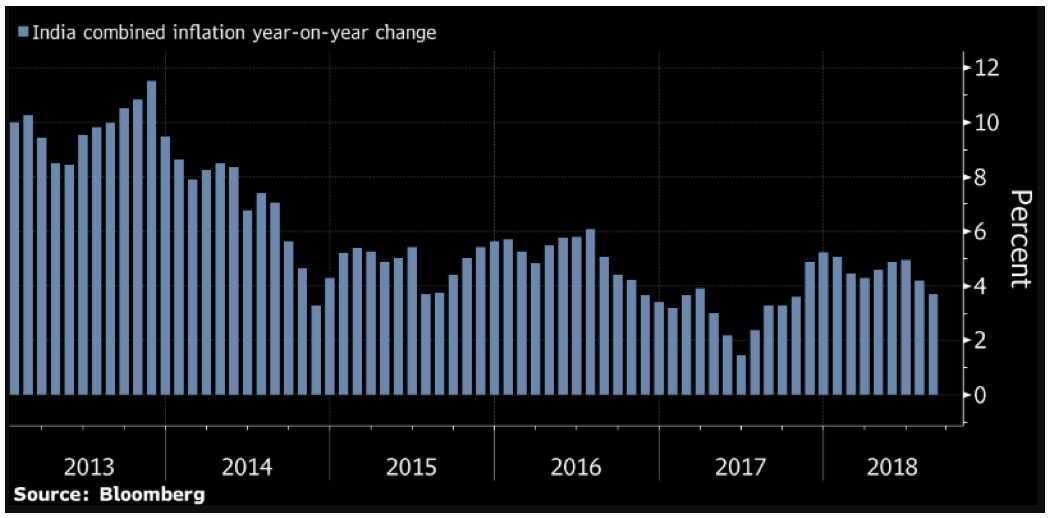

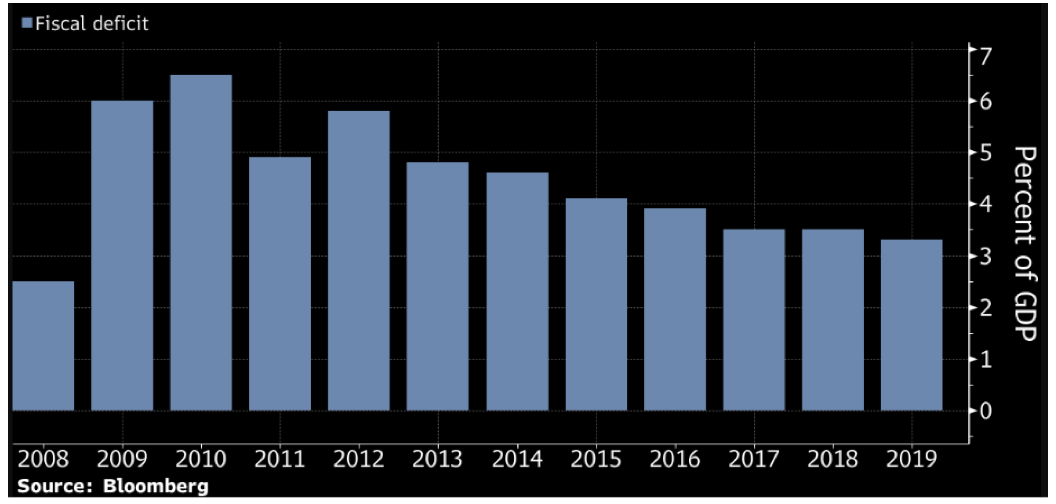

In an earlier article, I had categorically stated that the recent slide in rupee is not a cause of concern for me and one of the reasons why I made that assertion was that India had a manageable current account deficit, a narrowing fiscal deficit, low inflation (despite high crude prices) and healthy forex reserves. These healthy parameters ensured that despite the slide in the value of rupee there was a healthy confidence in the economy due to the strong macroeconomic fundamentals. This was in contrast with the previous slide in the rupee (Tapper Tantrum, 2013) that came with high inflation, high current account deficit, high fiscal deficit and a slowing growth: the stagflation era. Back then, despite interventions from the RBI, the rupee’s slide continued and a major reason behind this was the loss of confidence amongst investors and a very bleak outlook on the future economic prospects.

Thus, the key takeaway from this article is that rupee does not signal the health of the Indian Economy, however, it is an important indicator as far as the external sector is concerned. While international oil prices have a significant impact on the value of rupee, the strong macroeconomic fundamentals are key to mitigate any such downside risks to growth prospects of the economy.

Luckily, India has a very strong set of macroeconomic fundamentals and with the moderation of Oil Prices, strengthening of the rupee and moderation of India’s Current Account Deficit, the downside risks to our short and medium-term growth has significantly reduced.