June 2018 has been one of the worst months from a Chinese economic perspective. The RMB has been on free fall with the decline of more than 3% since Jan 2018. The Shanghai Composite has declined to lowest levels in the year with a drop of 20% from Jan 2018.

These are however symptoms of a larger crisis. To understand, one has to go back to 2008, the global financial crisis. China to stabilize its domestic economy and quell unrest, let loose a fiscal and monetary stimulus. This resulted in a boon in infrastructure splurge and a rise in property prices. This unrelenting spending tap has now created a Frankenstein monster. Popular wisdom holds that the Chinese economy is driven by exports and that trade is the main driving factor for economic growth. However, the Real estate now accounts for an estimated 25% of the Chinese economy including both direct and indirect contribution. To understand the implications of the above statement, the below factors need to be considered.

- More than 80 per cent of Chinese household wealth is held in land and real estate. Only about 10 per cent is held in financial assets, mostly bank products such as checking and savings accounts.

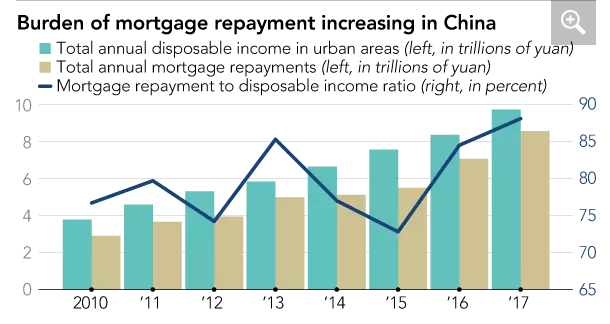

- The household debt to GDP ratio has increased from 10% in 2006 to 50% today. This is driven by an increase in the leveraged purchase of household assets. A clear indication of high prices is the fact that mortgage payments to disposable income are now at 90%+ in China. This would imply that the household has to save every penny earned to pay for a mortgage.

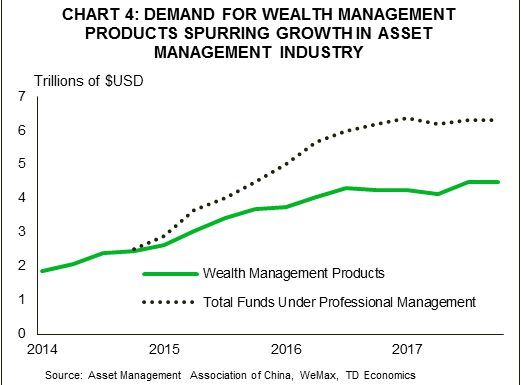

- Due to Financial repression, there are few alternatives for Chinese savers to invest in. Hence the significant source of savings is redirected to high-risk Wealth Management Products which offer higher returns. The assets under WMP have grown into USD 15 trillion. These, however, come with increased risks and most of the funds are invested in Corporate and Local Government Debt. Unlike traditional stock-based investment products like Mutual funds where the investor bears the full risk of investment, most of these WMP’s promise fixed rate of returns. In case of loss of the underlying asset value, WMPs will be forced to default on the payments.

- Land revenue constitutes the single most source of revenue for Chinese local government. Unlike in other countries, Chinese local government bodies don’t have the right to raise taxes (both direct and indirect). The only sources of revenue are – Revenue from land sales, Debt and the Central government funding. Estimated 18% of the revenue of local government is sourced from the sale of land.

- China’s high savings rate could be overestimated. As per Bloomberg, official savings rate includes government-mandated social-security contributions. Other government surveys show that Chinese households only save about 29 per cent of their actual income. After accounting for the fact that Chinese household income is equal to 44 per cent of GDP.

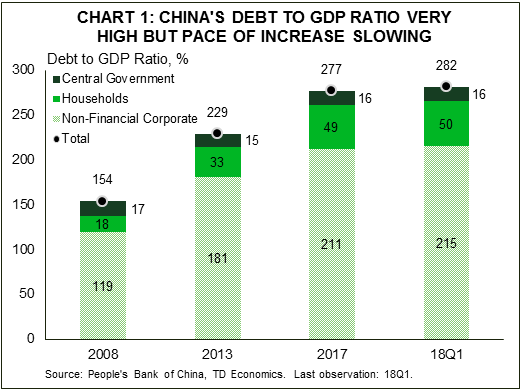

- This has created a mountain of debt across all sections of the Chinese economy. The Debt to GDP ratio for China stands at 282% as compared to 70% in India. Nearly 2/3rds of these debts are owned by Non-financial corporate entities including local government SPE’s and Zombie corporate entities. The Return On Assets (ROA) for State Owned Enterprises (SOE) is trending at 2-3%. Hence most of the debt is currently lying in unproductive sectors of the economy. China will have to enter into a significant restructuring involving huge loan haircuts to solve this problem. Based on 2017 OECD estimates, the liability to asset ratio of non-financial state-owned enterprises is around 60% in 2015. What’s more, the main driver of the advance was short-term debt.

Any central banker can control only 2 of the 3 monetary levers – Interest rates, Capital flow into the country and Exchange rates. China’s central bank PBOC is similarly facing a different variance of the trilemma.

- To stave off economic recession, the central bank has to reduce the cost of capital and infuse liquidity. Thus it would make sense to cut interest rates and reserve ratios. Any increase in interest rate would ripple through all sectors have both households will be impacted by higher mortgage costs, firms will find it harder to re-service debt resulting in a drop in both consumption and investment demand.

- Today China’s 1 yr yield rate of 3% is only 0.7% higher than US 1 yr rate of 2.33%. Thus for any investor, investing in riskier Chinese bonds would make sense only if the RMB can appreciate, otherwise taking into currency hedging costs, Chinese bonds are less attractive compared to US bonds

- The underlying economic weakness combined with the unwinding of the easy monetary policies including QE is causing the RMB to decline against the USD. This will force even more of the capital to flee before further depreciation of RMB.

Hence PBOC governor Yi Gang has the unviable task of balancing the restructuring the mountain of debt while ensuring no significant drop in investment and consumer confidence. This is a herculean task and previous efforts of similar bubbles have ended in a disaster like with Japan in the 1980s and the US prior to 2008 showdown. Beijing has studied Japan’s example and apparently sees forcibly bursting such bubbles as a mistake.

There is however little fear in global policy and economic circles of the coming Chinese economic crisis. The communist mandarins have been successful for the past 20 years to stave off repeated calls of Chinese economic recession and lead the country into unprecedented economic growth and prosperity. However, the reality is that the vast tools at the disposal of the mandarins have been used to effectively manage the short-term risk and kicking the proverbial can down the road. This is only creating a bigger problem to be solved in the future.

In the much-publicized book “This Time is Different: Eight Centuries of Financial Folly” by Reinhart and Rogoff. Each time there has been a speculative bubble driven by an unparalleled rise in debt levels, an economic recession has followed. But this time is indeed different, however from the perspective of economic management of Chinese officials and their ability to prove their naysayers wrong. It is different, purely because of one factor and that factor is Donald Trump and his trade wars.

The real cost of the tariffs levied by the US would be minimal, however in conjugation with the complexity of managing economic slowdown and growing debt pile would be significant. The tariffs inject a certain sense of volatility and unpredictability to the markets. These uncertainties and the general unpredictability of Trump policies towards China can make any complex and well planned economic management haywire. Trump presidency is like dumping Chinese bubbles into a stack of needles and all it needs is one small trigger to begin the big burst.