The budget for 2025-26 has provided major relief for the middle class by reducing the income tax burden. Finance Minister Nirmala Sitharaman in her budget speech announced substantial changes to the tax structure and raised the minimum taxable income to ₹12 lakh. This means, those with an annual income of ₹12,00,000 don’t have to pay income tax under the New Tax Regime.

Following the announcement, social media users and media have started calculations of income tax under the new structure. However, it seems that many people have missed one key component of the income tax calculation, which is the marginal relief.

Devil is always in the details!

— Manoj Arora (@manoj_216) February 1, 2025

Income <= 12 Lacs; No Tax ?

Income >12 Lacs; Tax starts from 4 Lacs ?

Several social media users have posted that once a person’s income exceeds ₹12 lakh, he or she will have to pay income tax on the whole income. Some are saying that one person’s income increases from ₹11.90 lakh to ₹12.10, the tax outgo will go up from zero to ₹61,500, based on calculation of tax for the slabs above 4L, 8L and 12L.

While it is true that if the income exceeds the exemption limit, tax becomes payable on the entire taxable income, there is actually a relief for income that exceed the limit by a very small amount. This is called the marginal relief.

The marginal relief was introduced under the New Tax Regime to ensure that taxpayers with income slightly above the exemption limit do not pay excessive tax compared to those earning below the limit. As a result of this marginal relief, taxpayers earning slightly above ₹12 lakh won’t have to pay the income tax calculated on their income, as the marginal relief will be deducted from the payable tax.

Under the tax structure announced in the budget, marginal relief will be calculated by deducting the amount exceeding ₹12,00,000 from the tax calculated on the entire taxable income, and this marginal relief will be deducted from the calculated tax.

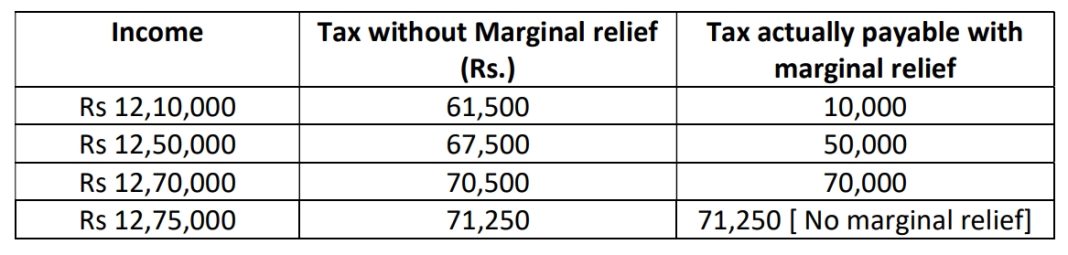

Let us see this with an example of a taxable income of ₹12,10,000. As this exceeds the exemption limit of ₹12 lakh, tax will be calculated on the entire amount. As per slabs, this will be 0 for first ₹4 lakh, ₹20,000 for next ₹4 lakh at 5%, ₹40,000 for the next ₹4 lakh at 10%, and finally 15% on the remaining ₹10,000. Thus, the total tax amount will be ₹61,500.

This seems unfair compared to a person earning ₹11,90,000, who don’t have to pay any tax. To remove this feeling of unfairness, the marginal relief has been introduced.

Now, as the income of ₹12,10,000 exceeds the exemption by ₹10,000, this will be deducted from the tax calculated to get the marginal relief. It will be ₹61,500-₹10,000, or ₹51,500 in this case. Therefore, this marginal relief so arrived will be deducted from the tax calculated to get the payable tax. This will be ₹61,500- or ₹51,500=₹10,000 in this case.

Under the new structure, marginal relief will be available if the taxable income exceeds the exemption by maximum ₹75,000. Therefore, if the income is above ₹12,75,000, there will be no marginal relief, and tax will be payable on the entire income.