")

The Reserve Bank of India concluded the uphill task of currency verification and released its report recently. Immediately there were many voices that chimed in discrediting the exercise. In fact, demonetisation was branded as a massive scam. In our earlier articles, we had explained why any claim that demonetisation is a failure is wrong. Since then we have access to more data and many more factually incorrect claims hence clearing the air is important.

So let us again rewind the declared aims sought to be achieved and analyse each one independently.

- Track and tax “black money” in the system

- Bring more people into the formal economy and/or tax base

- Encourage digital payments leading to “less cash economy”

Claim 1: Track and tax black money (Offical Source)

When one delves into the data, some startling revelations come to the fore. Let us take the persons holding PAN and in the Business category for preliminary analysis. There are 2% corporates who have deposited 22.6% of cash and the average deposits in this category is at 1.37cr.

In the non-corporate and proprietor category, the average deposits stand at 42 lacs and approximately 16 lacs and together they account for an approximate 50% of the deposits in the overall category. During demonetisation, the deposits were backed via identity cards and later most of the bank accounts too, have been to Aadhaar. The last date to file the Income Tax return for the period 01/04/2016 to 31/03/2017 was 31/03/2018 which has surpassed. It won’t be a surprise if many cases of deposits during this period, which you can see above are way ahead of the Income Tax limits, will be picked up for scrutiny. In fact, that process has already started, the details of which, can be read here.

Salient points from the report are quoted for ease of understanding.

- Corporates which account for 2% of the reported PAN have a share of 22.6% in the reported cash transactions.

- Proprietors (individual running business) have a share of 41.5% in the reported cash transactions.

- Taxpayers doing business have a share of 78.4% in the reported cash transactions.

- 36.1% of the PAN holders in the reported cash transactions have not filed a return.

If not for demonetisation, how was the opposition planning to find an address to every currency that was circulating? Without exhausting the set time limits under the law, no Income tax proceeding could be started. People have shown an extreme amount of restlessness while judging demonetisation and when the facts and figures are analysed in totality, the cynicism doesn’t add up.

We analysed a second official source which is listed here

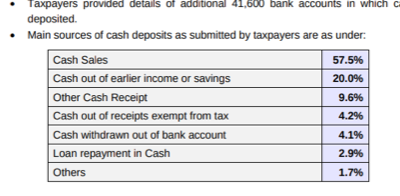

Based on preliminary findings 17.92 lakh persons for verification process were identified by the Income Tax Department. These people were sent notices. Nearly half of them have replied to the same. The notices usually asked them the source of their cash and reasons. Based on responses a tabulation was made which is presented below and is self-explanatory

- 57% have claimed that the cash deposits were sales.

- Taxpayers have provided responses for 13.33 lakh accounts involving cash deposits of around Rs.2.89 lakh crore.

- Taxpayers provided details of additional 41,600 bank accounts in which cash was deposited.

The skeptics must answer, that if not for demonetisation, how could these details be unearthed?

Based on this analysis the IT department categorised taxpayers in various categories. It makes sense to first target the high-value evaders, then the medium and then low. The figures for each category are below

Notices for first 1 lac are already issued. Details here

As time passes, other categories will be tracked. IT dept will also have staff issues etc.

Moving on, let’s see the second claim:

Claim 2: Bring more people into the formal economy and/or tax base

Following is an analysis of the numbers.

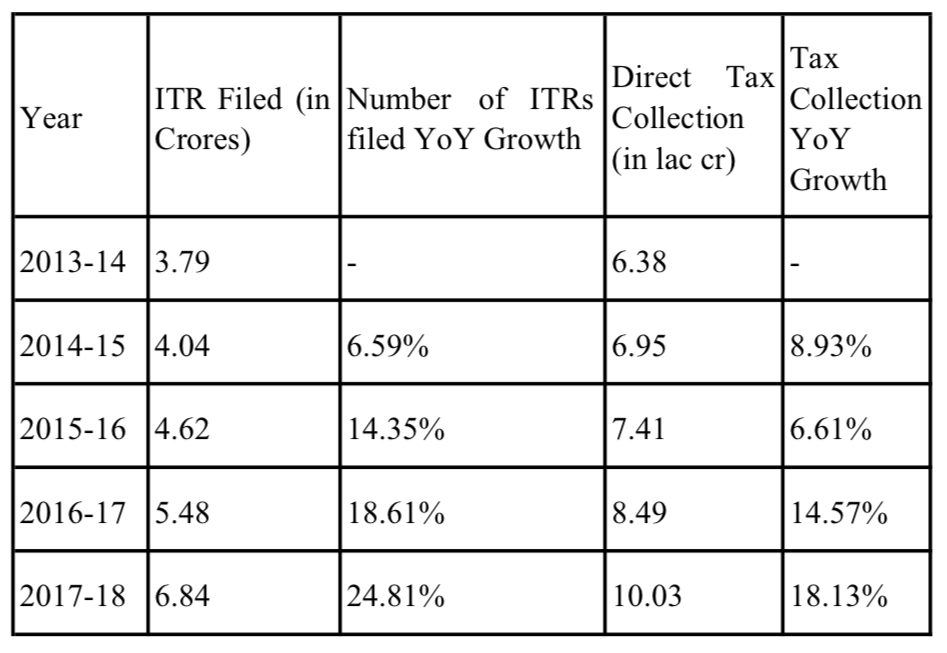

- During FY 2017-18, 6.84 crore Income Tax Returns (ITRs) were filed with the Income Tax Department as compared to 5.48 crore ITRs filed during FY 2016-17, showing a growth of 24.81%.

- As compared to 3.79 crores ITRs filed in F.Y. 2013-14, the number of ITRs filed during F.Y. 2017-18 (6.84 crores) has increased by 80.5%.

- During FY 2017-18, the number of new ITR filers has also increased to 99.49 lakh (as on 30.03.2018) as compared to 85.51 lakh new ITR filers added during FY 2016-17, which translates into a growth of 16.3%.

- For 2016-17 and 2017-18 the direct tax collections grew at 14.57% and 18.13% respectively and previous two years they were at 8.93% and 6.61% growth rates.

The steep increase in the number of ITRs filed as well as the amount of tax collected in 2016-17 and 2017-18 clearly shows that demonetisation has played a big role in both widening the tax base.

Claim 3: Encourage digital payments leading to “less cash economy”

There is no denying that digital payments have grown by leaps and bounds in the last two years. Data on digital payments shows that –

- In the last two financial years (FY 2016-17 and FY 2017-18), retail digital payment methods saw 103% increase in volume and 111% increase in value (source – RBI annual report 2017-18)

- Monthly usage of mobile wallets has grown by 311% in volume and 358% in value from Sept 2016 to June 2018 (source – RBI monthly bulletins December 2016 and August 2018)

- Usage of UPI has exploded since demonetisation. Though it was launched in April 2016, well before demonetisation, UPI did not see widespread adoption until demonetisation. In Oct 2016, UPI saw just a little over 1 lakh transactions amounting Rs. 48.6 crores. In August 2018, UPI transactions volume rose to 31.2 crores, amounting Rs. 54,212.26 crore. This is a staggering 3,02,832% growth in volume and 54,11,506% growth in value in less than 2 years! The number of banks integrated with UPI has more than quadrupled in the same period. (source – NPCI website, UPI Product Statistics)

All these numbers prove that Demonetisation has greatly helped in the widespread adoption of digital payment methods.

On 30 August, veteran journalist and commentator R Jagannathan wrote an article titled “Why DeMo Misfired: Here Are Some Of The Lessons We Can Learn From Fiasco”. While Mr Jagannathan is a respected journalist and is fully entitled to have his own views about Demonetisation, we would like to counter some of his claims in the said article –

Mr Jagannathan says (emphasis added):

“When demonetisation was announced on 8 November 2016, the stated goals were to reduce the stock of black money, throttle counterfeiting, and strike at the roots of terror funding; two more goals were added as an after-thought when the inflows of the demonetised notes in November 2016 exceeded official expectations. These were a move towards a less-cash economy (through the promotion and adoption of digital modes of payment), and capture of more information about who held what amounts of cash.”

The assertion that two goals were added as an afterthought isn’t true. A digital transaction has a complete footprint from source to destination. More digital payments mean more ‘white’ transactions, i.e. less black money in the system. Secondly, capturing information about who held what amounts of cash is essential in reducing the stock of black money. Black money gets generated when people hide their income from tax authorities to evade tax. Due to demonetisation, all the black money hoarded by tax evaders in the form of high currency notes had to be either discarded or deposited in banks. Every deposit made in demonetised notes got tagged to a person.

The data of such crores of deposits is being analysed by tax officials and action against evaders is being taken, as explained earlier. In addition to penalizing tax evaders, demonetisation also discouraged large-scale cash hoarding. In fact, in one of his earlier articles, Mr Jagannathan also acknowledged this – “Belief in cash has taken a knock, not so much in terms of everyday transactions, but as a commodity hoardable in sackfuls.”

Next, Mr Jagannathan also claims in his article (emphasis added):

“Indirectly, it was suggested that the political goals of demonetisation included trapping large chunks of demonetised notes outside the system, which would have reduced the Reserve Bank’s liabilities, and the “savings” paid out as a special dividend to the government. This, in turn, would have allowed the Narendra Modi government to claim that it had confiscated the ill-gotten wealth of the rich and given it to the poor in some form. But with 99.3 per cent of the notes coming back to” the system, it is clear that this objective, though never stated openly, was a 99.3 per cent failure.

We tried to find an official communication by the government or RBI which claimed that reducing the liability of RBI was an objective of demonetisation but could not find any. Mr Jagannathan himself also says that so such objective was stated by the government. All the claims of RBI liability reduction as an objective of demonetisation were just media speculations. In fact, Mr Jagannathan had also made a similar speculation in one of his articles immediately after demonetisation.

Mr Jagannathan further says,

“The benefits claimed so far are an increase in tax compliance and revenues, higher digitisation levels in absolute terms, etc. But the problem is we can’t clearly state that these gains were due to demonetisation since the goods and services tax (GST) provided an added impetus to formalisation from 1 July 2017.”

The claim that the increase in tax compliance and revenues cannot be clearly attributed to demonetisation is not correct. Our analysis above shows that the sharp uptick in direct tax collection started in FY 2016-17 i.e. before the launch of GST. In FY 2017-18 too, CBDT saw a 19.1% increase in direct tax collection for Apr-Jul 2017 i.e. before the launch of GST. Moreover, tax buoyancy, which is the ratio of increase in GDP to the increase in tax revenues, improved significantly post demonetisation. This proves that demonetisation improved tax compliance.

Another sentence from the article reads (emphasis added):

“Going forward, most of the gains in eliminating black money and tax compliance will be the result of GST and the rising formalisation of the economy, not DeMo.”

It is unclear if this is Mr Jagannathan’s hunch or he derived the conclusion based on some data, but we disagree with the assertion. Once a person is in the tax net, he/she cannot get out of it easily. Tax evaders who are being caught due to demonetisation will be on Income Tax department’s radar in the future as well, thus creating a recurring tax revenue for the government. It is true that GST is causing further formalization of the economy and expansion of the tax net, but that does not belittle what demonetisation has achieved.

Mr Jagannathan further claims (emphasis added):

“Jan Dhan thus worked as a laundromat for the tax evader, and – as a byproduct – also helped the poor make some commissions in the bargain”

This claim is far from the truth. Data shows that between 9 November & 28 December 2016, Jan Dhan deposits saw a net increase of approximately Rs 25,000 crore. This amount is less than 2% of Rs.14 lakh crore in demonetised notes which were deposited in that period. So it is factually wrong to say that Jan Dhan accounts were used for large-scale money laundering during demonetisation.

In summary, a sharp upsurge in tax collection and widening of the tax net, action against shell companies and potential tax evaders, and a healthy growth in digital payments prove that demonetisation was certainly not a failure.

(This article has been co-authored by Shantanu and Ashutosh Muglikar)