The Reserve Bank of India on the 29th of May 2024 ordered Edelweiss Asset Reconstruction Company Limited (EARCL) to cease and desist from the acquisition of financial assets, including security receipts (SRs), and reorganizing the existing SRs into senior and subordinate tranches. In the same order, the banking regulator also ordered ECL Finance Ltd (ECL) to cease and desist from undertaking any structured transactions in respect of its wholesale exposures with immediate effect.

EARCL and ECL both are entities under the Edelweiss group or the Edelweiss Financial Services Limited, based in Mumbai.

Why did the RBI come down heavily on Edelweiss and its group entities?

The RBI in its press release said, “The action is based on material concerns observed during the course of supervisory examinations, essentially arising out of conduct of the group entities acting in concert, by entering into a series of structured transactions for evergreening stressed exposures of ECL, using the platform of EARCL and connected AIFs, thereby circumventing applicable regulations. Incorrect valuation of SRs was also observed in both ECL and EARCL. Apart from the above, in ECL, supervisory observations included submission of incorrect details of its eligible book debts to its lenders for computation of drawing power, non-compliance with loan to value norms for lending against shares, incorrect reporting to Central Repository for Information on Large Credits system (CRILC) and non-adherence to Know Your Customer (KYC) guidelines. ECL, by taking over loans from non-lender entities of the group for ultimate sale to the group ARC, allowed itself to be used as a conduit to circumvent regulations which permit ARCs to acquire financial assets only from banks and Financial Institutions”.

If we break down this operative part of the RBI order, startling revelations about the functioning of Edelweiss and its group entities come to the fore:

- Edelweiss and its group entities were entering into structured transactions for the evergreening of loans.

- They were doing so through stressed exposures of ECL, using the platform of EARCL and connected AIFs, circumventing applicable regulations.

- Both ECL and EARCL (group entities of Edelweiss) were giving incorrect evaluations of Security Receipts (SRs).

- ECL, by taking over loans from non-lender entities of the group for ultimate sale to the group ARC, allowed itself to be used as a conduit to circumvent regulations that permit ARCs to acquire financial assets only from banks and Financial Institutions.

Evergreening of loans is a euphemistic phrase. In simple terms, it essentially means giving a fresh loan to avert the default on another loan, by using the new loan to repay the existing one. Essentially, it is done by several banks to hide the true nature of stressed loans. So let’s assume two banks have 2 stressed loans. Both banks would then ‘buy back’ the loans from each other to hide the real nature of the stressed loan. One of the common methods of evergreening of loans is to extend a loan to a related entity which is then used to pay back to stressed loan of the entity. For example, company A has a Rs 100 loan which it might default on. Company B, which is related to Company A, takes a loan of Rs 100 and then pays off the loan of Company A.

In December 2023 as well, the RBI had taken a stern view of Non-Banking Financial Institutions (NBFCs) utilizing the Alternate Investment Fund (AIF) route to evergreen their loans.

An Alternative Investment Fund or AIF is any fund established or incorporated in India that is a privately pooled investment vehicle that collects funds from sophisticated investors, whether Indian or foreign, for investing it in accordance with a defined investment policy for the benefit of its investors. Interestingly, AIFs cannot make invitations to the public at large to subscribe to its units and can raise funds from sophisticated investors only through private placement. AIFs (other than angel funds) are not allowed to accept from an investor, an investment of value less than Rs 1 crore. In the case of investors who are employees or directors of the AIF or employees or directors of the Manager, the minimum value of an investment is Rs 25 lakh.

AIFs are regulated by SEBI and are incorporated under the SEBI (Alternative Investment Funds) Regulations, 2012. All AIFs are required to submit reports to SEBI. Among the three categories, Category 1 and 2 AIFs are required to submit quarterly reports while Category 3 AIFs are required to submit monthly reports. It is pertinent to note that Edelweiss AIF, which we will be talking about in this article, is a Category 3 AIF which would require to submit monthly reports to SEBI. These AIFs are meant to be strictly controlled and monitored by the SEBI to ensure no malpractice is undertaken.

The issue, however, is larger than just evergreening of loans by NBFCs through AIFs. RBI’s Financial Stability Report, issued in December 2023, highlights the regulatory concerns over the growing interlinkages of AIFs with traditional providers of capital such as banks and NBFCs, spillover effects, and the potential for misuse of regulatory arbitrage between the different funding platforms.

As far as the RBI order concerning Edelweiss is concerned, it is clear that Edelweiss was not only evergreening loans by entering into structured transactions through its group entities but ECL and EARCL were also using connected AIFs to circumvent applicable laws.

This order by the RBI came days after a report by OpIndia where we had conducted a case study on the Hindustan National Glass (HNGIL) case. The HNG case is one of the longest Insolvency and Bankruptcy Code (IBC) cases in India – one that has dragged on for over 600 days (and counting). OpIndia has analyzed in detail how the conduct of the Competition Commission of India (CCI) has contributed greatly to the delay in the resolution process. We also analyzed how private financial institutions like Edelweiss were manipulating the IBC process for financial gains. While the OpIndia report focused on certain aspects of Edelweiss’ involvement in the HNG case, the RBI order passed under the SARFAESI Act opens a can of worms.

As we would now analyze, it would appear that Edelweiss and its group entities seem to have indulged in the same predatory practices in the HNG case for which the RBI passed strictures against Edelweiss Asset Reconstruction Company Limited (EARCL) and ECL Finance Ltd (ECL).

HNGIL – a classic case that fits into the scenario of Edelweiss group misusing its web of entities in a particular transaction to circumvent regulations.

The case started in 2020 with the DBS Bank initiating insolvency proceedings against Hindustan National Glass & Industries Limited (HNG) in NCLT Kolkata. Insolvency was admitted in the year 2021. Hindustan National Glass & Industries Limited is an Indian container glassmaker based in Kolkata. The company is the largest and one of the oldest glass manufacturing companies in India.

The IBC process as far as HNG goes is one of the longest resolution processes after the passage of the law – marred with allegations of impropriety on the part of the Resolution Professional (RP), conflict of interest, and hijacking of the process for financial gain by private players like Ernst and Young and Edelweiss, alleged oversight of material facts by the Committee of Creditors (CoC), which included Edelweiss, miscarriage of justice by the NCLT and finally, improper dispensation of the case by the Competition Commission of India (CCI). The insolvency process of HNGIL is now stuck in a series of litigations.

For this article, we would analyze how the Edelweiss group, using a web of entities, could have potentially indulged in the very same irregularities due to which RBI passed strictures against its group entities.

The insolvency proceedings against Hindustan National Glass (HNGIL) was initiated by DBS Bank.

According to the Committee of Creditors of HNG formed by the Resolution Professional in 2022, there were several creditors of CoC, SBI being the largest. The percentages indicated below are their voting percentages in the CoC based on their share of total debt.

i. State Bank of India- 38%

ii. Canara Bank- 5%

iii. Bank of Baroda- 1%

iv. Export-Import Bank of India- 4%

v. DBS Bank Limited -Singapore- 13%

vi. DBS Bank India Limited- 1%

vii. Edelweiss Asset Reconstruction Co. Ltd.- 24%

viii. Standard Chartered Bank- 2%

ix. Life Insurance Corporation of India- 8%

x. Goldman Sachs International Bank- 5%

xi. Rathi Brothers- 0%

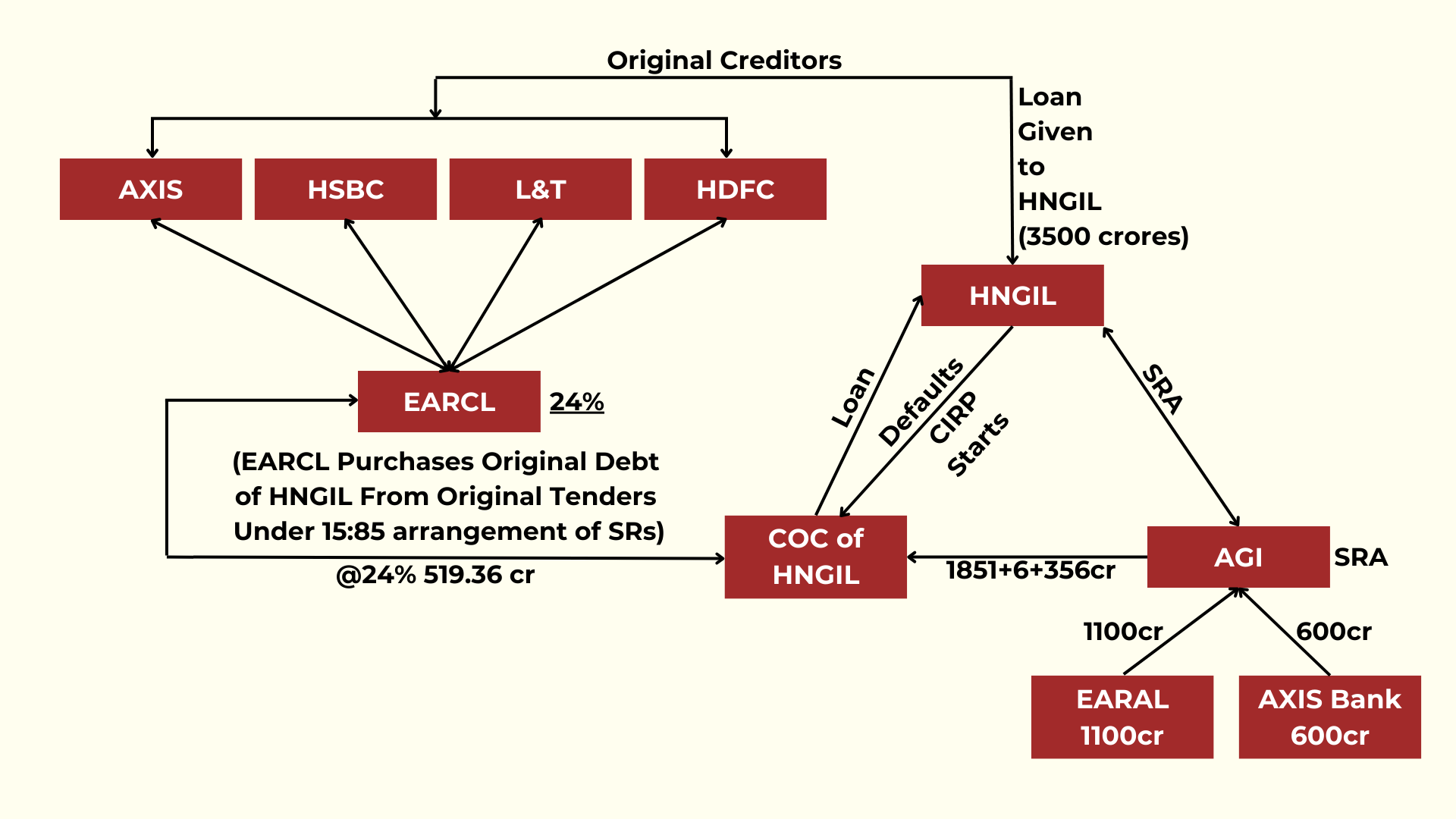

Edelweiss Asset Reconstruction Company Limited (EARCL or Edelweiss ARC) purchased the original debt of HNG from the original creditors under the 15:85 arrangement of Security Receipts (SRs). The debt purchased by EARCL was from Axis, HDFC, HSBC, and L&T. The original creditors had lent Rs 3500 crores to HNIG (Rs 3,500 crores of the amount that was loaned to HNG by the original creditors. HNG defaulted on that debt and therefore, went into the insolvency process).

EARCL purchased 24% of that Rs 3,500 debt which amounts to Rs 840 crores. While the debt purchased was Rs 840 crores, the original creditors would have taken a substantial haircut in this arrangement. This means that Edelweiss ARC would have paid far less than Rs 840 crores to purchase the debt which amounts to Rs 840 crores.

To make this simpler – Edelweiss essentially told Axis, HDFC, HSBC, and L&T that they were holding bad debts, which may or may not be realized. Further, the creditors can never be sure at what rate would their debt be realized post the IBC process. So, Edelweiss said that if their combined debt is Rs 100, it would buy the Rs 100 debt for Rs 40. The creditors take that Rs 40 thinking that they would recover at least that much of the total debt and be able to cut their losses.

Security Receipts (SRs) are essentially instruments issued by Asset Reconstruction Companies as consideration for their purchase of distressed assets from banks/ NBFCs – something EARCL used to purchase 24% of the debt from the original creditors of HNG after the latter went into the IBC process. The 15:85 rule essentially means that the Asset Reconstruction Company (ARC) purchases bad loans from the Bank by paying 15% of the value agreed upon and the remaining 85% is purchased by issuing Security Receipts (SRs) to the banks. This 85% is paid to the banks after the loan is realized after the resolution process – essentially – when the insolvent company (HNG in this case) is acquired by another company.

So far, EARCL purchased 24% of the debt from original creditors and paid 15% of it (under the 15:85 rule). The remaining 85% would only be paid after HNG is acquired and the resolution process would be completed.

In the case of HNG, after the issue of Expression of Interest, the RP received 14 bids to acquire HNG. Once the RP received the applications, on the 24th of May 2022, a Request for Resolution Plan was issued and eventually, only three firms expressed interest in purchasing HNG – AGI Greenpac (AGI), International Sugar Corporation (INSCO), and Nirma Chemical. Later, Nirma Chemical dropped out of the process and only two bidders remained – AGI and INSCO. As discussed in the earlier articles, the combination of AGI and HNG would lead to a monopolistic market whereas there were no such constraints if HNG was acquired by INSCO.

The legal jugglery in getting conditional approval for the AGI plan from the CCI, the misrepresentations of the Resolution Professional (RP) in this case, and the subsequent legal case which is still ongoing can be read in detail here and here.

In this article, we will analyze how Edelweiss had a vested interest in HNG being acquired by AGI and how it speaks to the very strictures ordered by RBI.

After acquiring the 24% debt from the original lenders, EARCL became a part of the Committee of Creditors (CoC) of HNG. It is pertinent to note that while EARCL was not an original creditor of HNG at all, after acquiring 24% of the debt, it became the second largest CoC member after SBI which had 38% of the debt.

When both plans by AGI and INSCO for the acquisition of HNG were put to vote to the CoC (after legal chicanery by the RP), the AGI plan was passed with the help of EARCL. At this stage, it is important to remember that the INSCO plan had CCI approval while the AGI plan did not and AGI’s application to CCI under FORM 1 was rejected “Not Valid” on 22nd Oct 2022 Yet, Edelweiss ARC voted in favor of the AGI plan thereby misusing its commercial wisdom.

In the CoC, each credit can vote for multiple plans or no plan at all and therefore, the percentages don’t add up to 100%. Edelweiss ARC, after purchasing the debt amounting to 24% also had one vote. The value of that one combined vote was 24%. However, at the explicit request of Edelweiss ARC, one vote was split into 4 votes by the RP – the combined value of the 4 votes being 24%. One of the votes it cast was against INSCO which resulted in AGI winning by 8.30% difference owing to Edelweiss ARC’s vote. Essentially, Edelweiss ARC cast all 4 votes in favor of AGI Greenpac. However, it cast only 3 votes in favor of INSCO, and therefore, AGI proposal won in the CoC by the 1 vote extra cast in its favor by Edelweiss ARC (EARCL).

Why did Edelweiss ARC (EARCL) have a vested interest in assuring that the AGI plan was passed by the CoC and eventually, leading to the acquisition of HNG

AGI Greenpac, which eventually became the Successful Resolution Applicant owing to the flawed presentation of the plan in the CoC and the oversight by CCI, had produced a letter dated 13th September 2022 as proof of funds for the acquisition of HNG.

In that letter, Edelweiss Alternate Asset Advisors Pvt Ltd (AAAPL) had committed Rs 1,100 crore to AGI Greenpac towards the acquisition of HNG. Edelweiss AAAPL is an AIF entity acting as the ‘Investment Manager of India Special Assets Fund III (a scheme of ISAD III), ISAF III Onshore Fund (a scheme of Edelweiss Credit Opportunities Trust), and EO Special Situations Fund (a scheme of Edelweiss India Special Situations Fund).

One of the key clauses of the funding that Edelweiss AAAPL was providing to AGI Greenpac was that the funding would only be approved if their proposal was approved by the CoC. Edelweiss Alternate Asset Advisors, in their letter, had told AGI that they would fund the acquisition of HNG by AGI only after the CoC approval. At the same time, Edelweiss ARC was a part of the CoC, influencing the decision of the AGI proposal being accepted by voting in their favor.

Further, the rush with which the AGI plan was passed, flouting laws and rules, could be for a specific reason. Edelweiss in its letter to AGI had also mentioned a deadline. It had said that if the AGI plan does not get CoC approval within 60 days, then the offer to fund the acquisition would not hold valid. The strict timeline imposed by Edelweiss ARC on AGI also seems to have played a role in the rush with which the AGI plan was passed by the CoC, owing to the distinguishing vote by EARCL in favor of AGI.

Edelweiss Financial Services Limited owns a 95% stake in Edelweiss AAAPL (AIF which is funding AGI with Rs 1100 crores). Edelweiss Financial Services Limited also has 65% shareholding in Edelweiss ARC (which is a member of CoC as a creditor, voting to ensure AGI’s plan for acquiring HNG gets approved) – either directly or through its subsidiaries.

It is therefore evident that Edelweiss has placed itself uniquely in a position where it is funding the acquisition of HNG by AGI through the AIF entity, and is also the creditor of HNG through its Asset Reconstruction Company after purchasing 24% of the debt from the original creditors.

Roundtripping of money by Edelweiss?

AGI in its resolution plan had undertaken to pay Rs 1851 crores to the CoC. Apart from the Rs 1851 crores of upfront payment to the CoC, it had also undertaken a payment of Rs 356 crores by way of deferred payment, to be paid over 3 years. This was discounted at a rate of 12% to arrive at a Net Present Value (NPV) of Rs 314 crores.

Therefore, while the original debt of HNG was Rs 3,500 crores, the resolution plan by AGI offered to acquire HNG for Rs 2,165 crores – the amount that would be used to pay the creditors of HNG.

Let us reverse engineer the sequence of events to understand how AGI’s deferred payment of INR 356 crore having NPV of INR 314 crore after discounting by 12% as defined in RFRP was funded through proceeds of divestment of the Rishikesh plant of HNGIL.

AGI Greenpac being the second largest container glass manufacturer in the country after HNGIL ought to have known that the combination of HNGIL+AGI would lead to a monopoly in the market thereby ending up in an Appreciable adverse impact on competition (AAEC). It would appear that to sidestep AAEC concerns arising out of the proposed combination affecting the CoC’s voting, AGI applied under FORM 1 (green channel) approval as highlighted in the previous article. FORM 1 was rejected on 22nd Oct 2022 and therefore AGI Greenpac again applied for CCI approval under FORM 2 (which requires detailed investigation) on 3rd November 2022 post-CoC approving its plan on 28th Oct 2022 through the conflicted vote of EARCL in favour of AGI Greenpac.

The Competition Commission of India (CCI), realizing this, issued a show cause notice to AGI on the 10th of February 2023 for potential AAEC. AGI while responding to SCN on 10th March and 14th March 2023 offered to divest the Rishikesh plant of HNGIL (corporate debtor) under a voluntary modification scheme as a remedy to AAEC concerns arising from the combination of AGI+HNGIL.

It seems like without verifying information submitted by AGI on voluntary modification, CCI conditionally approved the proposed combination of AGI-HNGIL subject to fulfillment of the Rishikesh plant.

There were several issues with the show cause notice issued by the CCI, since CCI failed to issue the show cause notice to HNG as well, the conditional approval it gave to the AGI combination plan and the modifications it accepted. An explanation of the probable missteps by the CCI can be read here.

However, it is important to note that the Rishikesh Plant did not belong to AGI at all. In its modified combination plan to CCI, it had undertaken the divestment of a plant that belonged to HNG.

One could theorize that the proceeds that AGI would get from the divestment of the Rishikesh Plant would then be used to acquire HNG and fund the Rs 356 crore over 3 years having NPV of INR 314 crore, to acquire HNG.

Essentially, it would seem like AGI has undertaken to divest a plant owned by HNG and the fund from the said divesture of an asset that does not belong to AGI would be then used by AGI to fund the acquisition of HNG. Documents in our possession show that the liquidation value of the Rishikesh plant which is spread over 11 acres of land is valued by a valuer appointed by RP is in the range of INR 200-300 crore, which indicates that AGI Greenpac is funding deferred payment of INR 314 crore (NPV) and paying to CoC by using proceeds generated from divesting one of the plant/assets which belongs to CoC (HNGIL).

Such dubious transactions raise suspicion on how CoC under the garb of commercial wisdom voted to the resolution plan which was rejected by CCI. Did EARCL vote exclusively in favor of AGI to benefit its AIF entity which was funding AGI Greenpac for said acquisition? That is a matter of investigation which must be carried out.

It is pertinent to note that SBI having the highest vote share of 38% leading the CoC of HNGIL allowed such transactions to go through which resulted in less financial recovery and caused ultimate loss to public money along with other PSU entities like LIC, BoB, etc.

Let’s simplify with a hypothetical scenario. A owes Rs 100 to B. A tells B that out of the Rs 100, A would give B Rs 40 right away. For the other Rs 60, A would sell of B’s phone and pay him back the amount from the proceeds of the sale.

The entire fiasco leads to a playing field that is tilted in the favor of AGI, with the help of Edelweiss, seemingly tarnishing the entire process of IBC.

Moving on, EARCL, which had purchased debt from the original creditors had purchased 24% of the debt under the 15:85 plan. When debt is purchased by an ARC company from original creditors, it is generally at a haircut to the original creditors. Per industry norms, the haircut is a minimum of 40-60%.

This means that if the original credits were owed Rs 100 by AGI, Edelweiss ARC purchased that Rs 100 debt for, say Rs 40 Out of that Rs 40, it paid 15% upfront and the remaining 85% is to be paid when the resolution plan for HNG goes through.

On the other hand, Edelweiss AAAPL funded AGI with Rs 1,100 through Non-Convertible Debentures. This means that at the end of a specified period, Edelweiss AAAPL gets the Rs 1,100 crores back along with the interest on the NCDs.

So what does Edelweiss make, financially, at the end of the deal? Edelweiss ARC, which is now a part of CoC after purchasing debt at a haircut to original creditors, gets 24% of Rs 3500 crores – which is about Rs 840 crores. Edelweiss ARC had in all probability purchased the debt at 40-60% lower than 840 crores, given that a 40-60% haircut to the original creditor is the industry norm. If we assume that EARCL purchased the debt of Rs 840 crores at a 40-60% haircut to the original creditors, it would mean that it purchased the debt under the 15:85 scheme would be much lower than Rs 840 crores.

In this scenario, when EARCL gets 24% of Rs 2165 crores (which is the AGI proposal), it would get about Rs 519 crores.

Here is how.

At the end of the deal, Edelweiss AAAPL gets the Rs 1,100 crore back with interest (17% to 22%) and Edelweiss ARC gets the Rs 519 crore.

Edelweiss AAAPL would in turn tell authorities that it booked a profit on their transaction. They got the Rs 1,100 back and the interest they got from AGI would be booked at profit while Edelweiss ARC would potentially say that it was a loss-making transaction owing to loss in interest due to delay in the process. Documents in our possession read that CoC has claimed that as of March 2024, CoC has incurred an interest loss of INR 850 crore (EARCL interest loss: 24*850= INR 204 crore) due to a delay in the conclusion of CIRP.

Together, these group entities (EARCL and Edelweiss AAAPL) would transfer the money to Edelweiss Financial Services Ltd. Edelweiss Financial Services (Holding company) then adjusts the “loss-making transaction” and the profit-making transaction, to pay less taxes on both transactions combined in a probable scenario.

Such a structured arrangement of using connected/related entities on both sides of the deal typically in the case of the use of ARC and AIFs creates a huge conflict of interest and thereby encourages a lack of transparency in such deals which potentially are being done to benefit financially on both sides of the deal by circumventing regulations and round tripping of rounds as observed by RBI in its order dated 29th May 2024.

Due to lack of transparency, one entity can show a potential loss in the deal due to haircut being taken as part of CIRP and another entity which is on another side of the deal (EAAAL) is earning interest income by funding successful resolution applicant (in this case AGI Greenpac) is transferring funds from one entity to another entity using CIRP as medium for potential tax evasion.

Such transactions should be investigated by concerned investigation agencies like the Income tax department, SFIO, ED, and other competent agencies to ascertain if there has been tax evasion which is hinted at by RBI in its order dated 29th May 2024.

The other thread that we must consider in this transaction is asking – where is this Rs 519 crores to Edelweiss ARC coming from?

It is essentially coming from the Rs 1,100 crores that Edelweiss AAAPL had extended to AGI to acquire HNG. Because AGI would use the Rs 1,100 extended by Edelweiss AAAPL towards the Rs 2165 crores that it would pay to the CoC to acquire HNG. Edelweiss ARC being a part of CoC would get 24% of that amount.

In the end, it would appear that Edelweiss AAAPL may have roundtripped Rs 519 crores to Edelweiss ARC, channeling it through AGI using IBC as a mechanism.

On the other hand, it is also pertinent to note that Axis Bank was one of the original creditors of HNG. It sold its entire debt to Edelweiss ARC and after having done so, extended Rs 600 crore to AGI to purchase HNG. Why was this done? Essentially, the Rs 600 extended to AGI to acquire HNG would earn interest. That interest would then make up for the haircut that Axis took while selling its debt to Edelweiss ARC at a haircut.

The transaction by Axis Bank is not particularly barred under the IBC, however, the Edelweiss transaction seems to be of the exact nature on which the RBI passed strictures.

The RBI stricture observed that “the group entities were acting in concert, by entering into a series of structured transactions for evergreening stressed exposures of ECL, using the platform of EARCL and connected AIFs, thereby circumventing applicable regulations”.

In the HNG case, Edelweiss seems to have done exactly what the RBI voices its concerns about – circumventing applicable regulations through group entities entering into structured transactions in concert.

Further, the fact that action against Edelweiss was taken by the RBI under the SARFAESI Act also shows concerns regarding money laundering and round-tripping of money. It is pertinent to note that on 31st May 2024, the Deputy Governor at RBI had also raised similar concerns. “Asset reconstruction companies (ARCs) are being misused by “tainted” promoters to enter the bankruptcy process after leading their firms to loan defaults”, deputy governor of Reserve Bank of India M Nageshwar Rao had said.

What becomes important to consider after the entire sequence of events is analyzed is that Edelweiss and its group companies have been pulled up by the RBI. Edelweiss Asset Reconstruction Company Limited (EARCL) has been ordered to cease and desist from the acquisition of financial assets, including security receipts (SRs), and reorganize the existing SRs into senior and subordinate tranches. In the same order, RBI also ordered ECL Finance Ltd (ECL) to cease and desist from undertaking any structured transactions in respect of its wholesale exposures with immediate effect.

With such strictures, it cannot be ignored that the very same entities and group companies of Edelweiss are indeed involved in the HNG case with their involvement leading to an inordinate delay in the IBC process. The HNG case has now been ongoing for over 600 days. As per the CoC of HNG itself, the inordinate delay in the IBC process has resulted in an accumulated interest loss of over Rs 850 crores to the creditors. One could argue that the inordinate delay in the process is a consequence of wrong CoC decisions to back and favor AGI Greenpac as a successful resolution applicant whose resolution plan appears to be full of contingencies. It also resulted in a situation where CCI approval only kicks in after the successful divestment of the Rishikesh plant of HNGIL whereas it can only be divested once AGI’s plan is approved by Adjudicating authority but due to stale mate situation Adjudicating authority cant approve its resolution plan in absence of unconditional approval from CCI which mandatory requirement under IBC and RFRP, as discussed in the previous article.

However, the elements that were overlooked by the CCI were also a result of the involvement of Edelweiss and its group companies. It was Edelweiss that tipped the scale in AGI’s favor in the CoC with its distinguishing vote and the process has been in a freefall ever since. With the hints of Edelweiss hijacking the IBC process, the misrepresentations made by AGI, the potential roundtripping of funds, and the apparent tipping of the scale towards AGI despite INSCO getting the CCI approval raises several questions on the bodies that are meant to regulate financial institutions like Edelweiss. With RBI coming down heavily on Edelweiss, it would seem only right for the RBI to evaluate the role played by Edelweiss in the HNG case and for SEBI to step in and evaluate if it needs to step in to ensure that Edelweiss, and by extension, AGI, needs to be investigated for the potential flouting of regulatory norms in the HNG.

Given the questions which are being raised on the conduct of Edelweiss and its group entities, it would perhaps call for a thorough investigation where potentially, given the RBI order, SEBI could instruct Edelweiss AAAL to rescind its letter dated 13th Sept 2022 committing Rs 1,100 crores to AGI for its acquisition of HNG pending further investigation, at the very least.

Given the gravity of the situation, there are several questions come to mind and need rationalization by the RBI and SEBI.

SEBI:

- Taking cognizance of the RBI order will SEBI come down on Edelweiss Group for misusing AIFs connected with other entities of Edelweiss Group as observed in the RBI order dated 29th May 2024?

- Has SEBI taken note of the RBI order and initiated any action against Edelweiss Group for potential misuse of AIF platforms?

- What are the checks and balances followed by SEBI to protect investors in AIF platforms controlled by Edelweiss Group?

- Does SEBI see merit in taking cognizance of the RBI order and further coming out with specific order for restricting participation directly/indirectly by funding AGI Greenpac through its AIF entity called Edelweiss AAAPL, acting as the ‘Investment Manager of India Special Assets Fund III (a scheme of ISAD III), ISAF III Onshore Fund (a scheme of Edelweiss Credit Opportunities Trust) and EO Special Situations Fund (a scheme of Edelweiss India Special Situations Fund)’?

- Is there any ongoing investigation against Edelweiss Group for using connected/associated AIFs to enter into structured transactions to circumvent regulations as observed by RBI in its order? If not, why?

- Will SEBI restrict Edelweiss Alternate Asset Advisors of India Special Assets Fund III (a scheme of ISAD III), ISAF III Onshore Fund (a scheme of Edelweiss Credit Opportunities Trust), and EO Special Situations Fund (a scheme of Edelweiss India Special Situations Fund) from directly or indirectly funding resolution applicant AGI Greenpac?

- Will SEBI issue an interim order to immediately restrict AIF entities connected to Edelweiss from acquiring business?

- Will SEBI invoke issue of conflict of Interest in HNGIL CIRP case and restrict AIF entity of Edelweiss Alternate Advisors Limited from directly or indirectly funding AGI Greenpac?

RBI:

- RBI has recently restricted various Edelweiss entities from acquiring new business through an order dated 29th May 2024. Will RBI further restrict/examine the role of EARCL in HNGIL insolvency Case?

- Will RBI launch an investigation into the role of EARCL and connected AIFs in HNGIL CIRP?

- Will RBI further pass supplementary orders to penalize the role of various Edelweiss group entities like EARCL and connected AIFs which are used to circumvent regulations and create circular funding issues in the HNGIL deal, after investigation?

- Will RBI investigate Edelweiss Group especially EARCL and connected AIF entities like EAAAL for potential round-tripping of funds through such structured transactions as the HNGIL Insolvency case?

- What steps RBI is considering taking to come out with a robust monitoring tool for minimizing such misuse of ARC and AIFs to circumvent regulations and round-tripping of funds?

- Will RBI consider recommending SFIO inquiry on Edelweiss Group, especially keeping in mind its own order of 29th May 2024 exercising restrictions on EARCL and connected AIFs?

The IBC process is a robust one that ensures transparency and the interest of creditors as well as the going concern itself. However, as discussed, Edelweiss seems to be misusing the process for financial gains and potential round-tripping of funds, as per the RBI order and the facts of the HNG case. Financial institutions such as Edelweiss, while almost indispensable in the IBC process, must be curtailed and monitored far more thoroughly to ensure the sanctity of the IBC process.