Earlier last month, an explosive report by a US research firm Hindenburg Research caused tremors in the Indian stock markets after it accused the Adani Group of manipulating its share prices and committing accounting fraud.

Gautam Adani, the founder and chairman of the Adani Group, one of the top 5 wealthiest people in the world before the report was published, saw his fortunes turn and wealth erode as nervous investors pulled money out by selling their holdings of the Adani Group stocks.

The crisis was exacerbated by the Adani Group’s decision to call off an oversubscribed FPO in view of the serious allegations levelled against the group by Hindenburg Research. While the business conglomerate trashed the report as malicious disinformation and released a whopping 413-page statement to contest the claims made by Hindenburg, the attendant confusion, uncertainty, and anxiety among investors sent the group’s stocks into free fall.

The pathological hatred harboured by the left-leaning liberals in India, who abhor successful businessmen for their ability to generate wealth and provide employment which they never could with their hoary activism and communist principles, also contributed to the bloodbath that Adani Group stocks witnessed at the stock market.

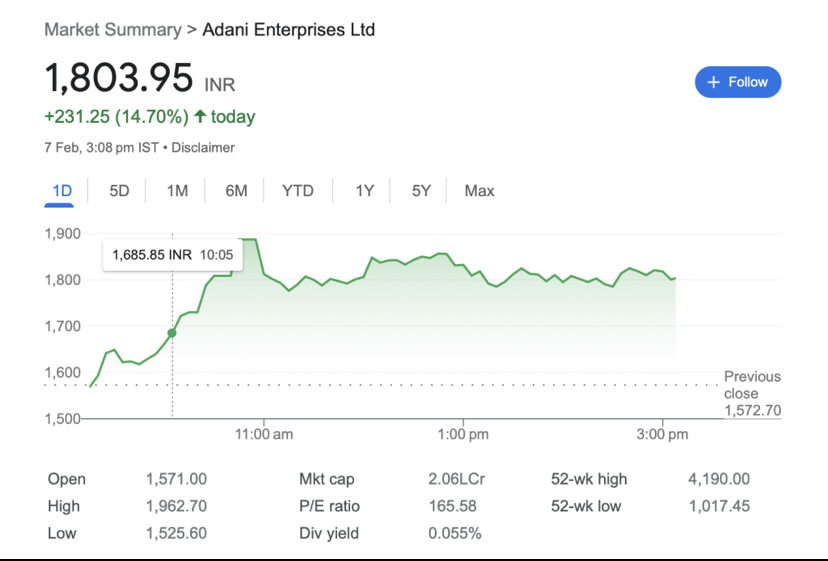

In a matter of just 31 trading sessions, the shares of Adani Enterprises, one of the foremost Adani Group companies listed on the stock market, crashed 76 per cent from their all-time high. The stock, which hit an all-time high of Rs 4,189.55 on December 21, 2022, slipped to a 52-week low of Rs 1,017.10 last week, plummeting 75.72% from its peak. Taking into account the market cap of Rs 1.57 lakh crore for the Adani Group’s flagship, the firm lost over Rs 2.88 lakh crore in market cap from its record high. On December 21 last year, the market cap (at the close of trade) of the firm stood at Rs 4.45 lakh crore.

As Adani Group’s market cap was taking a beating on stock markets, with some estimates claiming the group lost over $100 bn in valuation, a raft of left-leaning ‘liberals’, evidently with little understanding of how bourses work, gleed over the losses suffered by the business conglomerate. They cited the lower-circuit hit by Adani Group shares to emphasise that the Hindenburg Research group’s allegations had some measure of truth to force a market correction on the stock markets.

But more importantly, they used the stock market crash of the Adani Group shares to undermine the Indian growth story witnessed under PM Modi’s government in the last nine years. They insisted that the Indian Growth Story is as hollow as the Adani Group shares that are now tanking after allegations of gross manipulation and accounting fraud claimed by Hindenburg. The idea was to politicise the stock market crisis and co-opt it to use as a stick to beat the Modi government and implicate wrongdoing on its part by highlighting the alleged close relationship between Adani and PM Modi.

Nevertheless, the Adani Group shares saw an impressive recovery this week, with two trading sessions seeing many of the Group’s shares touching upper circuit levels. The stocks of Adani Enterprises, the company that was at the receiving end of negative sentiments fostered by Hindenburg and paranoia stoked by the left-liberal cabal, touched a high of Rs 1,962.70 during Tuesday trading sessions and is currently hovering at Rs 1,803 levels (up by 14.69 per cent) at the time of writing this report.

Notwithstanding the remarkable recovery registered by Adani Enterprises on the bourses, it is worth examining some of the doomsday scenarios that usual suspects foreboded, which may have contributed to the decline in the share prices.

Many gloating over the Adani crisis quickly declared it as India’s Lehman Brothers moment, the culmination of the subprime mortgage crisis in the United States that triggered a worldwide recession back in 2008. Of course, they did not elevate Adani Group to the extent of bringing about a global recession. They restricted their contention to the realm of Indian economic space, which they declared would suffer massively if Hindenburg’s allegations against Adani turned out correct.

Adani: Fundamentals are strong & balance sheet robust

— Praveen Chakravarty (@pravchak) February 2, 2023

Lehman Brothers:

Sept 10 2008: Fundamentals are strong & balance sheet robust.

Sept 15 2008: Filed for bankruptcy.

“Did you mislead investors?” asked US Congress in their hearing

. pic.twitter.com/zkf76EVQAH

Lehman Brother dooba tha toh saari duniya mein recession de gaya tha.

— Kapil (@kapsology) February 1, 2023

Socho Adani dooba toh kya hoga!

In 2007, Lehman Brothers had a record market capitalization of $60 billion. Then came the crash. By 2016, it cost the US economy about $4.6 trillion.

— Salman Anees Soz (@SalmanSoz) February 2, 2023

Since #HindenburgReport, Adani Group has lost $100 billion in value. The Government must step in to protect the broader economy.

But their characterisation of the Adani crisis being a trigger to cause the undoing of the Indian growth story speaks more to their pathological hatred for India and an implicit acceptance that India had charted an enviable growth story in the last few years than their genuine concerns for retail investors.

Why Adani’s fall would expose Adani and not be a harbinger of a Lehman Brothers-like

However, comparing the Adani crisis to the bankruptcy of the Lehman Brothers is like comparing apples to oranges. It is disingenuous of the gloaters to draw a parallel between the two issues even when they are starkly distinct. In fact, the rush to hyphenate the Adani crisis and Lehman Brothers’ bankruptcy betray that liberals have no understanding of either of the issues.

For starters, Lehman Brothers was a financial institute, not a business conglomerate like the Adani Group. The Lehman Brothers crisis was a significant event in the 2008 global financial crisis. It was a bankruptcy filing by the investment bank Lehman Brothers on September 15, 2008, which was one of the largest and most complex in U.S. history.

The bankruptcy of Lehman Brothers triggered a chain reaction in the financial markets and led to a global credit crunch, as well as a drop in the stock markets around the world. The crisis highlighted the interconnectivity and vulnerability of the global financial system and led to significant government intervention in many countries, including the U.S. government’s Troubled Asset Relief Program (TARP) and other measures to stabilize the financial system and restore economic growth.

A financial institute, especially one that was as deeply embedded into the system as Lehman Brothers, incurs a greater risk of triggering cascading ramifications, including recession, through its involvement in financing disparate organisations and sectors—the crash of anyone could severely impact the organisation’s health and future viability.

By contrast, the Adani Group is a business conglomerate whose primary concern is to stay in business, meet its financial obligations, and provide value to its investors. Unlike a financial institute, the Adani Group’s fortunes depend on its actions and not on the performance of other organisations or sectors.

In addition to this, many state-owned financial institutions like the LIC, State Bank of India, Punjab National Bank, and others have minuscule exposure to the investments or loans granted by them to the Adani Group. For instance, the SBI recently cleared apprehensions, stating that it has only 0.9 per cent exposure to Adani and has granted loans against shares but against cashflows. The largest lender also said that it is confident in Adani’s repayment of loans, adding that the group has a historical record of paying on time.

The underlying cause of Lehman Brothers’ bankruptcy was a combination of factors, including excessive risk-taking, leverage, and a lack of diversification in its investment portfolio. The bank was heavily invested in mortgage-backed securities, which suffered significant losses as the U.S. housing market declined and the subprime mortgage crisis deepened. As the value of these securities declined, Lehman Brothers’ balance sheet became increasingly strained, and it was unable to find the capital it needed to meet its financial obligations.

Additionally, the bank’s high levels of leverage, or borrowing, magnified its losses and made it difficult for it to survive the market turmoil. The combination of these factors ultimately led to Lehman Brothers’ bankruptcy and its impact on the global financial system.

While the Lehman Brothers’ collapse could be attributed to a deeper financial malaise plaguing the US financial sector, the allegations on the Adani Group do not reflect system-wide wrongdoing. If proven, the allegations would expose the malpractices espoused by the Adani Group, and the corresponding fall would only impact the business conglomerate.

Those using the Hindenburg Research report to paint gloom and doom and predict a Lehman Brothers-like scenario are unjustifiably resorting to alarmism and paranoia to push their political agenda.