India’s Prime Minister Mr Narendra Modi has declared his vision of making India a $5 trillion economy by 2024. The hallmark of visionary leaders is that they set audacious targets and then achieve them. However, the roadmap to achieve this goal is not devoid of its share of challenges. A deeper look into the current economic situation and required growth rates to achieve this milestone would reveal that this would be a “stretch goal” which is achievable but not without significant action on economic reforms.

As per the published data from the International Monetary Fund (IMF), India’s GDP in 2018 was $2.7 trillion. IMF forecast for India’s GDP in 2024 is $4.7 trillion. These estimates are in-line with Morgan Stanley which forecasts India’s GDP to touch $5 trillion by 2025.

The INR/USD exchange rate assumed by the IMF for future years in the above analysis is shown in the table below. The green cells contain data taken from IMF and white cells show the calculated values.

From the IMF estimates above, it can be inferred that if –

- India’s nominal GDP grows at about 11.8% per year

- and inflation hovers at around 4% to 4.2% per year (hence real GDP growth = 7.6% to 7.8% per year)

- and INR depreciates at no more than 2% per year (INR/USD exchange rate in 2024 is less than 79)

Then India’s nominal GDP would be approximately $4.7 trillion in 2024.

The size of the economy in 2024 could exceed $4.7 trillion, if the GDP growth rate picks up or if Rupee stays stronger than the above estimates. For example, if real GDP grows at 7.6% per year, but the currency exchange rate in 2024 stays at the levels of INR 75 per USD then nominal GDP would hit $4.9 trillion in US dollar terms.

Challenges

Unfortunately, the global economy is currently going through a slowdown as all major economies of the world are facing headwinds. As of 2019, USA is facing an economic slowdown. China’s GDP growth is at 27 years low and Industrial Output is at 17 years low. Germany is facing a recession (not a slowdown of growth, but actual CONTRACTION of the economy). France’s growth is declining across industries. In Britain, investments are down to 17 years low. Japan’s factory output has slumped. Australia’s GDP growth is at 20 years low. Singapore is facing a recession. South Korea exports are down for 8 consecutive months and the world economy is expected to grow at its slowest pace since the financial crisis of 2008.

With all major economies of the world going through turbulence, India’s economic growth is expected to face a temporary slowdown too. During such scenarios, exports may find it tough to rise and investments may dry down which would make the target even stiffer.

Opportunities

At the same time, the ongoing US-China trade war can be potentially leveraged as a huge one-time opportunity. Towards the year 1999, the global issue of Y2K migration had presented an opportunity that was seized with both hands by the Indian IT companies. That one-time window of opportunity helped nascent Indian IT companies to grow by leaps and bounds and become global behemoths. The current US-China trade war presents a similar opportunity that could potentially help India’s Manufacturing sector grow rapidly.

As per USISPF, hundreds of companies are currently looking to relocate their manufacturing base from China. Elon Musk had expressed his desire to start Tesla Manufacturing in India. If Government of India could swiftly come up with policy reforms for companies looking to start manufacturing in India, it could lead to the rapid expansion of India’s Manufacturing sector with large scale job creation, increased exports and rapid economic growth.

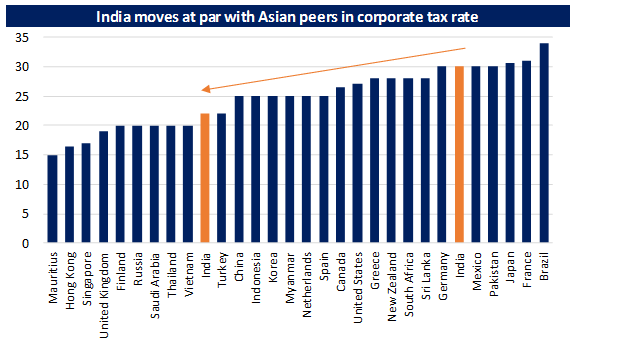

Structural reforms like IBC, GST and others have helped India jump World Bank’s Ease of Doing Business rankings from 142 (in 2014) to 63 (in 2019). That’s a quantum jump signifying a marked improvement in starting new businesses in the country. In another favourable policy change, the government has slashed corporate tax rates from 30% to 22% for existing companies and from 25% to 15% for new manufacturing companies. Including a surcharge and cess, the effective tax rate for existing companies would now come down from 35% to 25.17%. This makes India a highly attractive investment destination for companies looking to set up manufacturing.

In a continued slew of reforms, the government may also announce a dedicated relationship manager for any entity investing more than $500 million in India. Such an officer would help the investor with all government clearances at the centre and state levels.

The Road Ahead

The above steps show the government’s intent to fuel economic growth. However, while the above are necessary, they may not be sufficient by themselves. As the above analysis illustrates, an aggressive increase in exports is not only the key to boost economic growth but would also strengthen INR to propel the nominal GDP even higher.

For the last few years, India’s exports have stayed stagnant. Recently, a government panel has reported that an Exports growth rate of 10% is achievable. It requires India to reduce the cost of capital and introduce labour reforms that facilitate easier business expansion. Making labour laws more flexible would enable firms, particularly in labour-intensive sectors, to scale up rapidly. This would create more jobs in the MSME sector which is traditionally the backbone of the Indian economy for sustainable growth, employment generation, development of entrepreneurial skills and contribution to export earnings.

Another recommendation to increase exports is through a renewed focus on Free Trade Agreements (FTAs). In that direction, it might be worthwhile to consider that by early November 2019, India may sign up RCEP (Regional Comprehensive Economic Partnership) deal. RCEP is a Free Trade Agreement between ten ASEAN countries along with six additional members that include India, China, Australia, New Zealand, Japan and South Korea. In the currently proposed form, RCEP would be the world’s largest economic bloc, covering nearly half of the global economy.

Read: All you wanted to know about the RCEP, the trade deal forming the world’s largest economic block

RCEP requires member countries to provide duty-free access to their markets to each other. This makes RCEP a double-edged sword. While some trade organizations in India fear that this might help Chinese goods to flood Indian markets, the treaty also has its benefits for Indian exports. For agricultural products like rice, India has a competitive advantage and RCEP would open up ASEAN countries as a new 10 million tonne market for India. The treaty would also enable Indian industry to join global supply chains for high-end goods such as electronics and engineering.

Additionally, the government is also pursuing a limited trade deal with the USA to reinstate GSP (Generalized System of Preference) for India. GSP is the largest US trade preference programme and is designed to promote economic development by allowing duty-free entry for thousands of products from designated beneficiary countries.

If India signs up RCEP and the limited trade deal with the USA, then it might provide a significant opportunity to increase exports in the coming years. It would also compel Indian manufacturers to create globally competitive products for local consumption and exports, lest they lose out to cheaper imports from China, Vietnam and South Korea.

Summary

The key to hitting the $5 trillion mark is increasing exports, reducing the cost of capital and bringing flexible labour laws. While the government has taken some steps in the above direction, more action on economic reforms is still required.

Eventually, whether India’s nominal GDP reaches $5 trillion by 2024 or is stuck at below $4.7 trillion is dependent on how the various global factors play out and how the Government of India rolls out economic reforms to propel the economy.