The union govt is reportedly going to table a Bill in the winter session of Parliament aiming to create a facilitative framework for the creation of official digital currency to be issued by the Reserve Bank of India (RBI).

As per the description of the Bill available, the ‘The Cryptocurrency & Regulation of Official Digital Currency Bill, 2021’ would seek a ban on all private cryptocurrencies. However, there would be certain exceptions to promote the underlying technology of cryptocurrency and its uses. The winter session will commence on November 29.

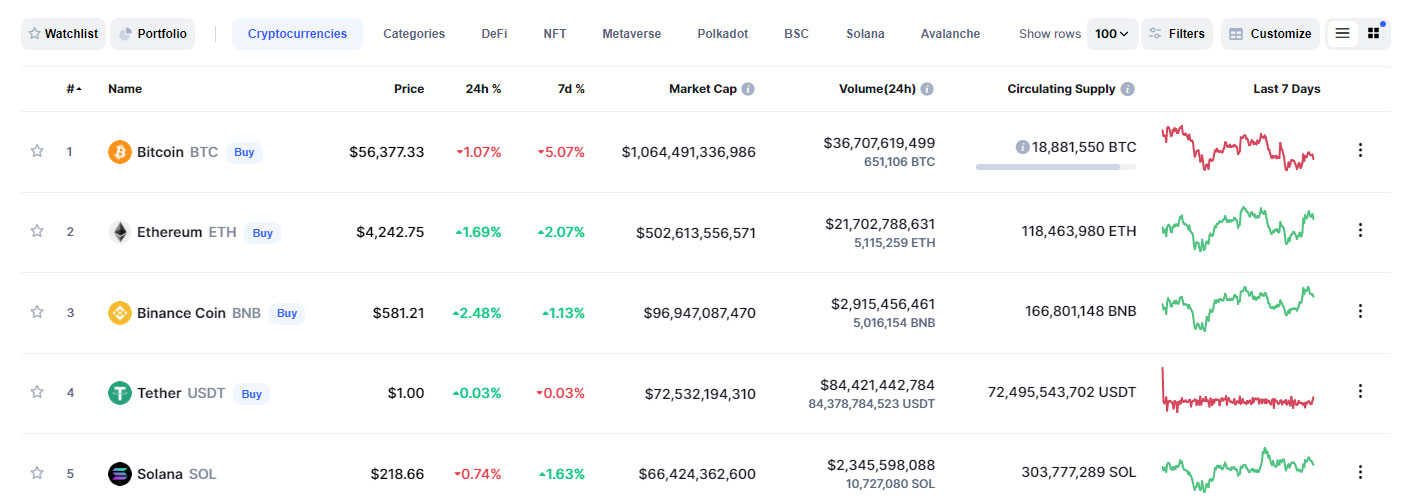

After the information about the Bill was made public, the major digital currencies saw a fall of around 15 per cent and more. However, later it recovered, and currently, three out of the top five cryptocurrencies are showing a rise in the price. Bitcoin is down by a little over 1%, and Solana is down by around 0.70%. On the other hand, Ethereum, Binance Coin and Tether are up by 1.70%, 2.50% and 0.11%, respectively.

In recent times, the Reserve Bank has voiced its concerns about private cryptocurrencies. Since the beginning of 2021, the price of Bitcoin has almost doubled its price of 2020. As per experts, there are around 15-20 million investors in India who have crypto holdings worth Rs. 40,000 crore.

Shaktikanta Das, the governor, RBI, had warned that cryptocurrencies pose a serious threat to financial stability. Notably, Prime Minister Narendra Modi also expressed his concerns about cryptocurrencies during his keynote address at the Sydney Dialogue on November 18. He had urged all countries to ensure cryptocurrencies do not fall into the wrong hands.

Last week, BJP leader Jayant Sinha chaired the Standing Committee on Finance meeting where they discussed the cryptocurrencies with the stakeholders, including representatives from crypto exchanges, blockchain and Crypto Assets Council (BACC), and others. The committee concluded that cryptocurrencies should not be banned but regulated.

Notably, in 2018, the RBI had put a blanket ban on cryptocurrencies in India. However, in March 2021, the Supreme Court set aside the order and allowed banks and entities regulated by RBI from providing services associated with cryptocurrencies.

While the crypto investors in India showed concerns since the announcement of the Bill, it is noteworthy that the definition of private cryptocurrency is yet to be clarified by the Centre. Cryptocurrencies like Bitcoin, Ethereum and others are based on public blockchain networks. While these networks provide anonymity to users, they are traceable. On the other hand, Cryptocurrencies like Monero, Dash and others are based on the private network, thus providing privacy to the investors.

Unlike China, India is not planning to put a blanket ban on Cryptocurrencies, but the idea seems to get it regularised. Nischal Shetty, CEO of WazirX, said in a tweet, “The crypto regulation bill has been listed for the winter session. The description hasn’t changed much. There will be speculation on both sides. The good thing is more people within the government are aware of how crypto works.” WazirX is the largest crypto exchange platform in India. In a follow-up tweet, he asked the investors to not panic.

This is not the end but the beginning of crypto regulations in India

— Nischal (WazirX) ⚡️ (@NischalShetty) November 24, 2021

Industry has had the opportunity to present. Law makers understand the growing market.

Over 15M+ people own crypto in India

There are ways to curb the bad activities and promote innovation

Don’t panic ✌️

While talking to CNBC TV18, Jayant Sinha had emphasised that innovation and regulation should be balanced. He added that various exchanges together have around 15 million KYC-approved users with an investment worth $6 billion.

The government is not only concerned about Cryptocurrencies going in the wrong hands but also about the misleading advertisements that have popped up in recent times promising steady returns to the investors. Banks are also informing their customers to beware of such advertisements.

As per Economic Times, Axis Bank managing director Amitabh Chaudhry said, “Our worry is that we can put all sorts of algorithms to trace customers who are putting money in crypto and have conversations with them to be careful, beyond that we can’t do much because it’s depositors’ money. I really worry when you see the ads because they seem to be indicating as if it’s like a deposit. One advertisement I saw said that the returns are four times that of fixed-deposit rates.”