The following article evaluates the efficiency of the new Insolvency and Bankruptcy Code, 2016 introduced by the NDA Government in delivering justice and recovering amounts owed to creditors, whereas such companies would have earlier taken shelter behind the chaotic legislation of the Congress regime.

Introduction

The insolvency resolution process in India has involved the simultaneous operation of several statutory instruments in the past.

These include:

- The Sick Industrial Companies Act, 1985

- The Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002

- The Recovery of Debt Due to Banks and Financial Institutions Act, 1993

- The Companies Act, 2013.

Broadly, these statutes have provided for disparate processes of debt restructuring, asset seizure and realization in order to facilitate the satisfaction of outstanding debts. A plethora of cases dealing with insolvency and liquidation has led to immense confusion in the legal system. There was a grave necessity to overhaul the insolvency regime.

Multiple legal avenues and a hamstrung court system led to India witnessing a huge piling up of non-performing assets. The Bankruptcy Code is an effort to allow credit to flow more easily in India and instilling confidence in investors for speedy disposal of their claims. The Code consolidates existing laws relating to the insolvency of corporate entities and individuals into single legislation.

The Code has unified the law related to enforcement of statutory rights of creditors and streamlined the manner in which a debtor company can be revived to sustain its debt without extinguishing the rights of creditors.

Applicability

The Code provides creditors with a mechanism to initiate an insolvency resolution process in the event a debtor is unable to pay its debts. The Code makes a distinction between Operational Creditors and Financial Creditors.

A Financial Creditor is one whose relationship with the debtor is a pure financial contract, where an amount has been provided to the debtor against the consideration of time value of money. Recent reforms have sought to address the concerns of homebuyers by treating them as ‘financial creditors’ for the purposes of the Code.

By a recently promulgated ordinance, the Insolvency and Bankruptcy Code (Amendment) Ordinance, 2018 (“the Ordinance”), the amount raised from allottees under a real estate project (a buyer of an under-construction residential or commercial property) is to be treated as a ‘financial debt’ as such amount has the commercial effect of a borrowing. The Ordinance does not clarify whether allottees are secured or unsecured financial creditors. Such classification will be subject to the agreement entered into between the homebuyers and the corporate debtor.

In the absence of allottees having a clear status, there may be uncertainty about their priority when receiving dues from the insolvency proceedings. A debtor company may also, take recourse to the Code if it wants to avail of the mechanism of revival or liquidation. In the event of inability to pay creditors, a company may choose to go for voluntary insolvency resolution process – a measure by which the company can itself approach the National Company Law Tribunal (“NCLT”) for the purpose of revival or liquidation.

Institutional Framework

The Code proposes the creation of several new institutions, all of which have specialized roles in the insolvency resolution process. The Code has created a regulatory and supervisory body, the Insolvency and Bankruptcy Board of India (“IBBI”), which has the overall responsibility to educate, effectively implement and operationalize the Bankruptcy Code.

The IBBI has the added responsibility to facilitate the functionality of the Code by studying practical implications and framing rules/regulations to overcome any difficulty or hurdle. The Code envisions the creation of a unit of professional insolvency practitioners, known as Resolution Professionals (“RP”). These Professionals are tasked with overseeing various aspects of the resolution of insolvency. The Code also sets up Insolvency Professional Agencies, which are professional bodies that will regulate the practice of insolvency professionals. Individual practitioners are required to be enrolled with insolvency professional agencies which are empowered to certify professionals, conduct examinations, and lay out a code of conduct.

Information Utilities

The Code envisages the establishment of information utilities. Information utilities are tasked with the collection, collation, maintenance, provision and supply of financial data to businesses, financial institutions, adjudicating authorities, insolvency professionals and other relevant stakeholders. These will thereby serve as a comprehensive repository of information on corporate debtors that are of a financial nature. It is optional for operational creditors to provide financial information to the information utility. This information, including records of liabilities, defaults, and overall debt, is to be sourced from creditors by the utility service. In what is a positive step forward towards transparency, all security interests created on assets are to be reported to the utilities by financial creditors.

The records with the utilities have evidentiary value in the initiation of insolvency resolution procedure and can assist various stakeholders in arriving at an ideal resolution at distressed companies. However, the Code is silent on the networking and interlinking of multiple information utilities. National e-Governance Services Ltd. (NeSL), a government entity, has become the first information utility after receiving the required approvals from the IBBI.

The framework of the Code

All proceedings under the Code in respect of corporate insolvency are to be adjudicated by the NCLT. NCLT has been designed as the special one window forum which can tackle all aspects of insolvency resolution. The NCLT is referred to as the Adjudicatory Authority in relation to the insolvency of corporate persons under the Code. No other court or tribunal can grant a stay against an action initiated before the NCLT. Appeals from the orders of the NCLT lie before the National Company Law Appellate Tribunal (“NCLAT”). All appeals from orders of the NCLAT lie to the Supreme Court of India. The jurisdiction of civil courts is explicitly ousted by the Code with regard to matters addressed by the Code. Additionally, it is now established that the Limitation Act, 1963 shall be applicable to proceedings under the Code. Thus, time-barred claims are outside the purview of insolvency.

Corporate Insolvency Resolution and Liquidation

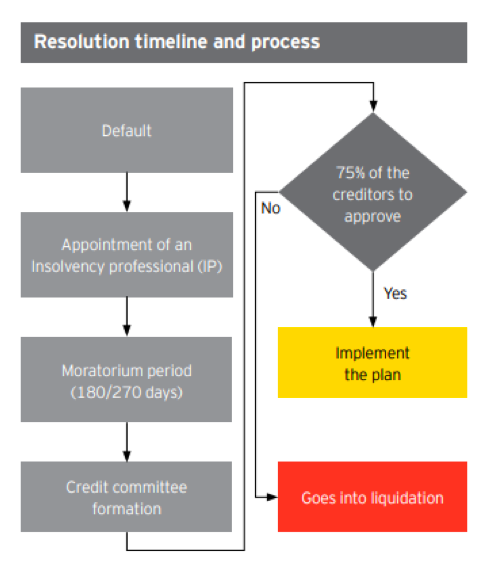

The figure below shows the typical resolution timeline and process. The basic steps are as follows

- Default

- Appointment of insolvency (IP)

- Moratorium period (180/270 days)

- Credit committee formation

It can be seen from the image below that if 75% of the creditors approve then only the insolvency plan can be implemented otherwise the firm goes into liquidation.

Key Highlights Corporate insolvency resolution process

Application on default– Any financial or operational creditor(s) can apply for insolvency on default of debt or interest payment

Appointment of IP– IP to be appointed by the regulator and approved by the creditor committee. IP will take over the running of the Company. From the date of appointment of IP, the power of the Board of directors is to be suspended and vested in the IP. IP shall have immunity from criminal prosecution and any other liability for anything done in good faith

Moratorium period– Adjudication authority will declare moratorium period during which no action can be taken against the company or the assets of the company. A key focus will be on running the Company on going concern basis. A Resolution plan would have to be prepared and approved by the Committee of creditors

Credit committee– A credit committee of creditors will be constituted. A related party is to be excluded from the committee. Each creditor shall vote in accordance to voting share assigned if 75% of creditor approve the resolution plan the same needs to be implemented.

Liquidation Process

Initiation– Failure to approve resolution plan within specified days will cause initiation of Liquidation. The debtor can also opt for voluntary liquidation by a special resolution in a General Meeting.

Liquidator– The IP may act as the liquidator, and exercise all powers of the BoD. The liquidator shall form an estate of the assets, and consolidate, verify, admit and determine the value of creditors’ claims.

Order of priority for distribution of assets

- Insolvency related costs

- Secured creditors and workmen dues up to 24 months

- Other employee’s salaries/dues up to 12 months

- Financial debts (unsecured creditors)

- Government dues (up to 2 years)

- Any remaining debts and dues

- Equity

Key Aspects of Insolvency and Bankruptcy Code

- IBC proposes a paradigm shift from the existing ‘Debtor in possession’ to a ‘Creditor in control’ regime.

- IBC aims at consolidating all existing insolvency related laws as well as amending multiple legislations including the Companies Act.

- The code would have an overriding effect on all other laws relating to Insolvency & Bankruptcy.

- The code aims to resolve insolvencies in a strict time-bound manner – the evaluation and viability determination must be completed within 180 days.

- Moratorium period of 180 days (extendable up to 270 days) for the Company. Insolvency professional to take over the management of the Company.

- Clearly defined ‘order of priority’ or the waterfall mechanism.

- The waterfall to render government dues Junior to most others is significant.

- Antecedent transactions can be investigated and in case of any illegal diversion of assets, a personal contribution can be ordered by the court.

- Introduce a qualified insolvency professional as intermediaries to oversee the Process

- Establishment of Insolvency and Bankruptcy board as an independent body for the administration and governance of Insolvency & bankruptcy Law; and Information Utilities as a depository of financial information.

Why Code is imperative today

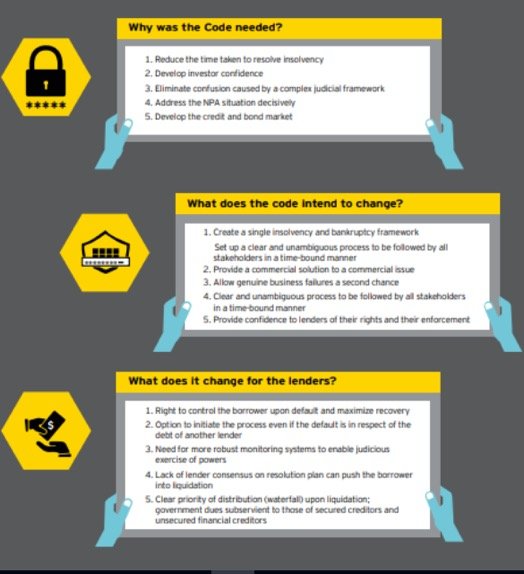

We illustrate below why the code was needed. What does the code intend to change for borrowers and lenders? And how the code has helped fast-track the resolution process?

Why was the Code needed?

- Reduce the time taken to resolve insolvency

- Develop investor confidence

3. Eliminate confusion caused by a complex judicial system - Address the NPA situation decisively

- Develop the credit and bond market

What does the Code intend to change?

- Create a single Insolvency and bankruptcy framework

- Set up a clear and unambiguous process to be followed by all stakeholders in a time-bound marine.

- Provide a commercial solution to a commercial issue

- Allow genuine business failures a second chance

- The clear and unambiguous process to be followed by all stakeholders in a time-bound manner

- Provide confidence to lenders of their rights and their enforcement

What does It change tor the lenders?

- Right to control the borrower upon default and maximize recovery

- Option to initiate the process even if the default is in respect of the debt of another lender

- Need for more robust monitoring systems to enable the judicious exercise of powers

- Lack of lender consensus on resolution plan can push the borrower into liquidation

- Clear priority of distribution upon liquidation; government dues subservient to those of secured creditors and unsecured financial creditors.

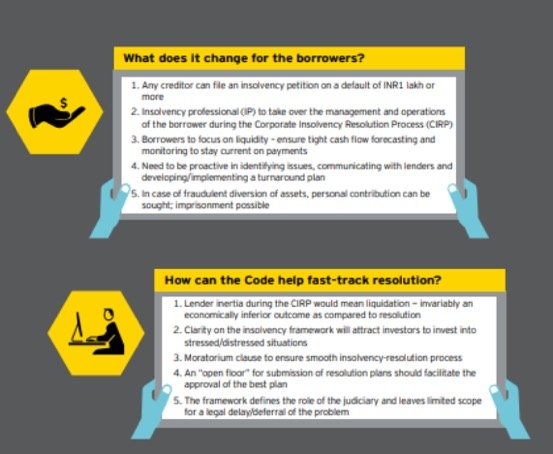

What does it change for the borrowers?

- Aar creditor can file an insolvency petition on default of INR1 lakh or more

- Insolvency professional (IP) to take over the management and operations of the borrower during the Corporate Insolvency Resolution Process (CIRP)

- Borrowers to focus on liquidity –ensure tight cash flow forecasting and monitoring to stay current on payments

- Need to be proactive in identifying issues, communicating with lenders and developing/ implementing a turnaround plan

How can the Code help fast-traffic resolution?

- Lender inertia during the CIRP would mean liquidation –invariably an economically inferior outcome as compared to the resolution

- Clarity on the insolvency framework will attract investors to invest in stressed/distressed situations

- Moratorium clause to ensure smooth insolvency resolution process

- An “open floor” for submission of resolution plans should facilitate the approval of the best plant

- The framework defines the role of the judiciary and leaves limited scope for a legal delay/deferral of the problem.

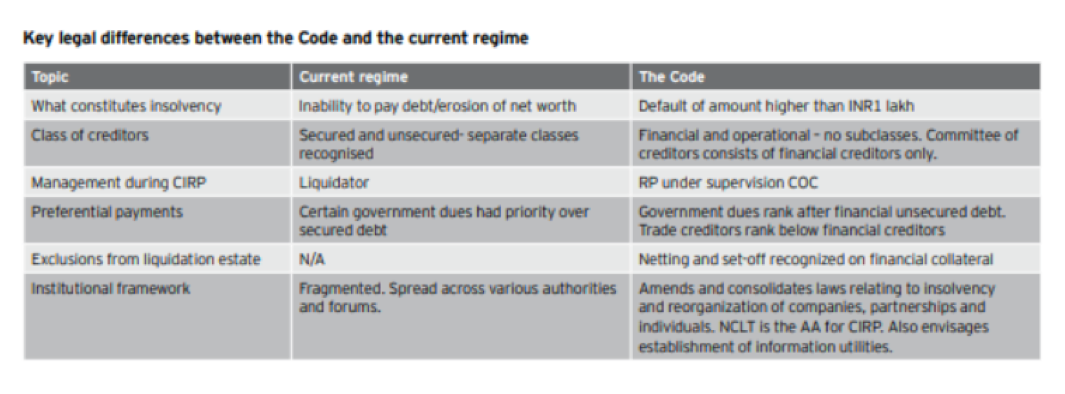

Key legal differences between the Current regime and Code

Below listed are key legal differences between the IBC and the current regime. The new Code clarifies the definition of what constitutes insolvency in a better manner, eliminates subclasses of creditors while empowering Resolution Professionals.

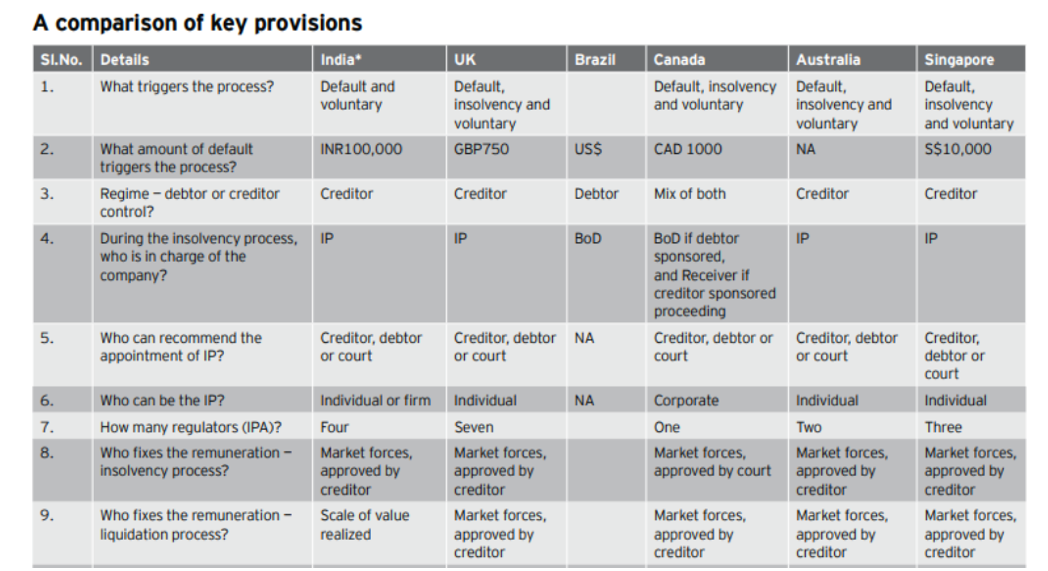

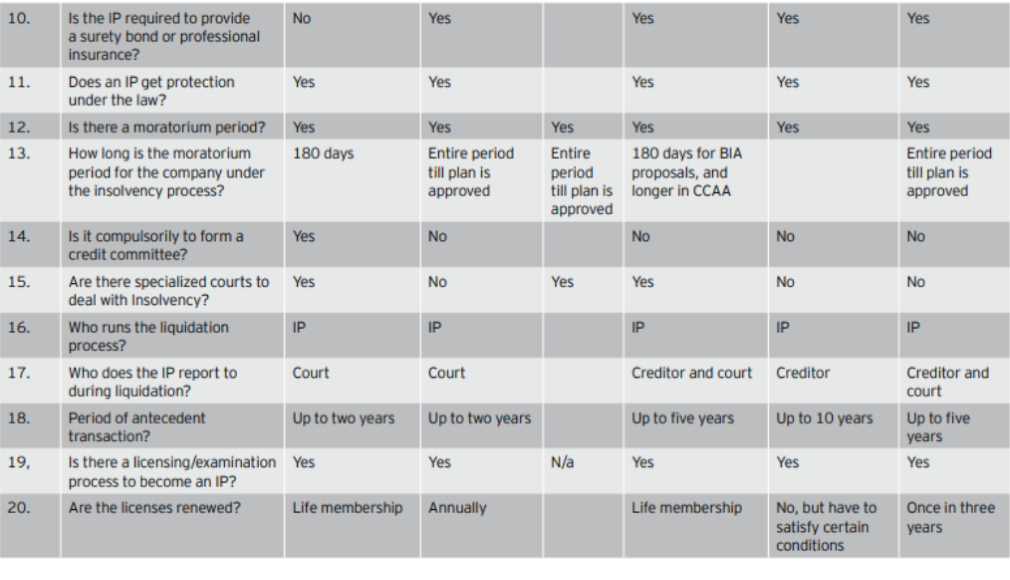

Insolvency and Bankruptcy code: – A Global View

Below image gives a comparison of 20 key provisions Insolvency and bankruptcy code amongst various nations and how India stacks ups against these nations. Key provisions of the Indian code are compared against countries such as the UK, Brazil, Canada, Australia and Singapore. Parameters of comparison include the process of triggering bankruptcy, the amount of default, who retains charge during the process, the extent of the moratorium period, and many other factors.

Insolvency and Bankruptcy code: – NDA Vs UPA

Congress left behind the legacy of an archaic system of resolving commercial insolvency. The Companies Act had a provision of winding up a company if it was unable to pay its debt. Additionally, the Congress Government had enacted the SICA in the decade of 1980s for rehabilitation of sick companies. This applied to companies whose net worth has become negative.

The law proved to be an utter failure. Law carried out rehabilitation, several sick companies got a protective iron curtain against creditors. The Debt Recovery Tribunal was created to enable banks to recover all dues diligently. But these have not proved to be highly efficient mechanism for recovering the debt. For non-corporate insolvencies the Provincial Insolvency Act was applicable. This rusted piece of legislation was ineffective and had faded away because of disuse.

The NDA Government headed by Atal Bihari Vajpayee had enacted the SARFAESI Law which proved to be much better than the earlier mechanism. In the year 2000, the NPAs had sky-rocketed into double digits. Both the SARFESI Law and the prudent interest rate management by the RBI helped in bringing the NPAs down.

Subsequently, between 2008 and 2014, Banks lent indiscriminately. This lead to a very high percentage of NPAs which was highlighted by the Asset Quality Reviews of the RBI. Prompt action by the NDA Government was taken. An Expert Committee was appointed, which submitted its Report in 2015 recommending the IBC.

Immediately, a Bill was introduced in Lok Sabha and referred to a Joint Committee of Parliament. The Parliamentary Committee displayed its wisdom and submitted a report recommending some changes in the Legislation. The IBC was approved by both Houses of Parliament in May 2016. This Economic legislative change has been made by the Parliament.

The NCLT was immediately constituted, the Insolvency Bankruptcy Board of India was established and the regulations were framed. By the end of 2016 corporate insolvency cases were being received by the NCLT.

The early harvest through the IBC process has been extremely satisfactory. It has changed the debtor-creditor relationship. The creditor no longer chases the debtor. In fact, it is otherwise. Upon the constitution of the NCLT and the implementation of IBC its functionality had revealed the need for improvements in the law. Two legislative interventions since then have taken place.

The NCLT has become a trusted forum of high credibility. Those who drive the companies to insolvency, exit from management. The selection of new management has been an honest and transparent process. There has been no political or Governmental interference in the cases.

The recovery of monies parked in insolvent companies has taken place through three methods:

- Firstly, after the introduction of Section 29(A) companies are paying up in anticipation of not crossing a red line and is referred to NCLT. As a result, the banks have started receiving monies from the potential debtors who pay in anticipation of the default. The defaulters are aware that once they get into IBC they will surely be out of management because of Section 29(A).

- Secondly, once a petition of the creditor is filed before the NCLT many debtors have been paying at the pre-admission stage so that the declaration of insolvency does not take place.

- Thirdly, many major insolvency cases have already been resolved and many are on the way of resolving. Those which cannot be resolved move towards liquidation and the banks are receiving the liquidation value.

So far,

- 1322 cases have been admitted by NCLT.

- 4452 cases have been disposed at the pre-admission stage and

- 66 have been resolved after adjudication.

- 260 cases have been ordered for liquidation.

In 66 resolution cases, the realization by creditors was around Rs. 80,000 crores.

As per NCLT database, in 4452 cases disposed at the pre-admission stage, the amount apparently settled was around Rs 2.02 lakh Crores. Some of the big 12 cases such as Bhushan Power and Steel Ltd. and Essar Steel India Ltd. are in advanced stages of resolution and are likely to be resolved in this financial year in which realization is expected to be around Rs 70,000 Crores.

By March 2019, recoveries worth Rs. 1.80 lakh crore is expected, with many resolutions at the final stages. Recovery to the tune of Rs. 52,000 Cr and Rs. 18,000 Cr are expected from Essar Steel Ltd and Bhushan Power & Steel Ltd respectively. Other stressed companies include Monnet Ispat, Amtek Auto and Ruchi Soya.

Increase in the conversion of NPAs into standard accounts and decline in new accounts falling in NPA category show a definite improvement in the lending and borrowing behaviour.

Essar Steel Insolvency case

Following is the timeline Essar Insolvency case

May 5, 2017: The central bank (RBI) is vested with more powers to fix bad loans issue in the banking system.

June 12, 2017: The RBI identifies 12 accounts for immediate resolution under the IBC.

June 27, 2017: Insolvency proceedings begin against Essar Steel in National Company Law Tribunal (NCLT).

July 4, 2017: Essar Steel challenges the RBI’s decision in Gujarat High Court.

July 17, 2017: After hearing both sides, Gujarat HC dismisses Essar Steel’s petition on the RBI’s insistence that the company was far from the debt-restructuring process.

August 2, 2017: NCLT admits Essar Steel for insolvency proceedings under the IBC. Satish Kumar Gupta is appointed Resolution Professional (RP) of the company.

October 2, 2017: Expression of Interest (EOIs) is invited by RP for Essar Steel.

November 2017: Essar Steel’s parent company Essar Group is learnt to be one of the bidders.

November 23, 2017: Section 29A is introduced via Ordinance to bar wilful defaulter, defaulter promoters and related parties from bidding.

February 12, 2018: First round of bidding takes place: Numetal and ArcelorMittal submit bids.

March 2018: RP holds both bids ineligible due Numetal’s connection with the Ruias and ArcelorMittal’s stake in an NPA account. Rewant Ruia, son of Essar Group’s Ravi Ruia, was a beneficiary in Numetal. ArcelorMittal held stakes in loan defaulter Uttam Galva, while Lakshmi Mittal held stakes in defaulter KSS Petron.

March 20, 2018: Numetal moves NCLT challenging the rejection of the bid.

March 26, 2018: ArcelorMittal also challenges disqualification in NCLT.

April 2, 2018: RP invites fresh bids.

April 19, 2018: NCLT Ahmedabad asks RP to re-examine first round of bids, saying RP rejected their offer without putting it in front of the Committee of Creditors (CoC).

September 7, 2018: National Company Law Appellate Tribunal (NCLAT) holds Numetal’s bid valid after it severs ties with Ruias. ArcelorMittal is asked to clear dues of Rs 7,000 crore of Uttam Galva and KSS Petron in three days.

September 10, 2018: ArcelorMittal revises offer to Rs 42,000 crore, including Rs 7,000 crore of past dues. Essar Steel had offered Rs 37,000 crore.

September 12, 2018: Numetal challenges NCLAT decision of allowing ArcelorMittal a chance to clear dues. ArcelorMittal agrees to pay Rs 7,000 crore only if it emerges successful bidder.

October 4, 2018: The Supreme Court gives one more chance, asks Numetal and ArcelorMittal to submit revised bids after paying outstanding dues in two weeks. If the account is not resolved in eight weeks, it will go into insolvency.

October 19, 2018: The Essar Steel Committee of Creditors picks ArcelorMittal as the highest bidder under the IBC.

25 November 2018: Standard Chartered Challenges ArcelorMittal’s bid citing Non-Compliance with IBC.

December 2018: Ruias, promoters of Essar steel make 54000 Cr counter bid to pay off loans.

December 10, 2018: Banks and ArcelorMittal oppose Essar steel’s bid.

29 January 2019: NCLT rejects Essar Steel’s promoter bid for settlement

February 2019: NCLAT directs NCLT Ahmedabad to take a call on ArcelorMittal’s Essar steel bid on March 8

March 8, 2019: ArcelorMittal bags Essar steel as NCLT Ahmedabad clears 42000 Cr takeover bid.

Insolvency and Bankruptcy code: – Way Ahead

It is evident that the Indian government is leaving no stone unturned in its aim to improve the Ease of Doing Business in India. The legislature, RBI, SEBI, and the judiciary have presented a unified front, unprecedented in India so far. Any apparent loopholes are being plugged at the earliest and the law is evolving rapidly.

It comes as no surprise, then, that as in 2019, India had already secured its position in the top 30 developing countries for retail investment worldwide and that insolvency resolution in India has become a more streamlined, consolidated and expeditious affair.

The implementation of Insolvency and Bankruptcy Code, 2016 has faced many challenges. These challenges have been tacked with effective amendments. The IBC has been doing a commendable job, and due credit needs to be given to all the officials who have worked diligently to introduce the Code. Insolvency resolution in India has become a more streamlined, consolidated and expeditious affair. It comes as no surprise, then, that India has already secured its position in the top 30 developing countries for retail investment worldwide. What needs to be seen is whether these measures can successfully be used to reduce the burden of stressed assets on the banking system and whether India can come on par with other developed nations in respect of insolvency resolution.