On Wednesday, the CBI filed a new FIR against NDTV, its founders Prannoy Roy and Radhika Roy and former CEO Vikram Chandra for alleged violation of Foreign Direct Investment (FDI) norms and alleged tax evasion. It is alleged that the accused floated subsidiaries in tax haven destinations to route foreign funds to India through sham transactions. It is also alleged that the proceeds of corruption of unknown public servants were invested in NDTV.

Two of its subsidiaries, NNPLC in London and NDTV lnternational Holding BV (NNIH) in the Netherlands, are at heart of the matter. Charges of criminal conspiracy, cheating and corruption have been slapped on the accused. As it so happens, the issues were flagged by the Assessing Officer (AO) of NDTV’s income tax returns who issued notices initiating reassessment proceedings against the accused and the provisional attachment of NDTV’s assets under provisions of the Income Tax Act, 1961.

NDTV filed a writ petition in the Delhi High Court against the decision of the authorities to initiate reassessment proceedings against the channel and provisionally attach their assets. The concerns registered by NDTV in its petition were summarily dismissed by the Court. The Court ruled in August, 2017 that there was merit in the AO’s arguments and hence, the demands made ought to be rejected.

The AO examined the Step Up Coupon Bonds issued by NNPLC, NDTV was the guarantor in the said transaction. According to the investigations of the authorities in the matter, NDTV also received $150 million through investments made in NDTV Networks International Holding BV (NNIH) by Universal Studios International BV, Netherlands (USBV) during FY 2008-09. After studying the entire matter, the AO concluded that NDTV had unaccounted money on which taxes were not paid.

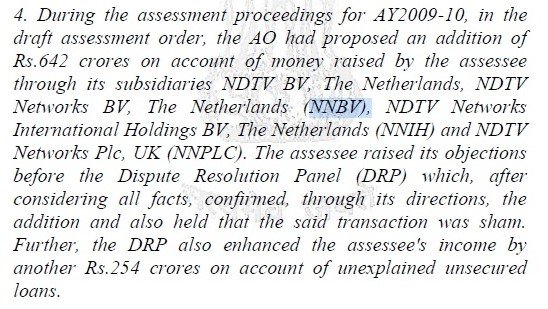

According to the AO, the investments made in its subsidiaries were actually NDTV’s own unaccounted money and was of the view that it was a sham transaction. The matter was further examined by the Dispute Resolution Panel (DRP) which permitted the lifting of the corporate veil. The lifting of the corporate veil is a legal term that indicates a legal decision to treat the rights or duties of a corporation as the rights or liabilities of its shareholders. Ordinarily, a corporation is treated as a separate legal entity that is solely responsible for its debt and credit. However, on exceptional occasions, the corporate veil can be ‘pierced’ or ‘lifted’.

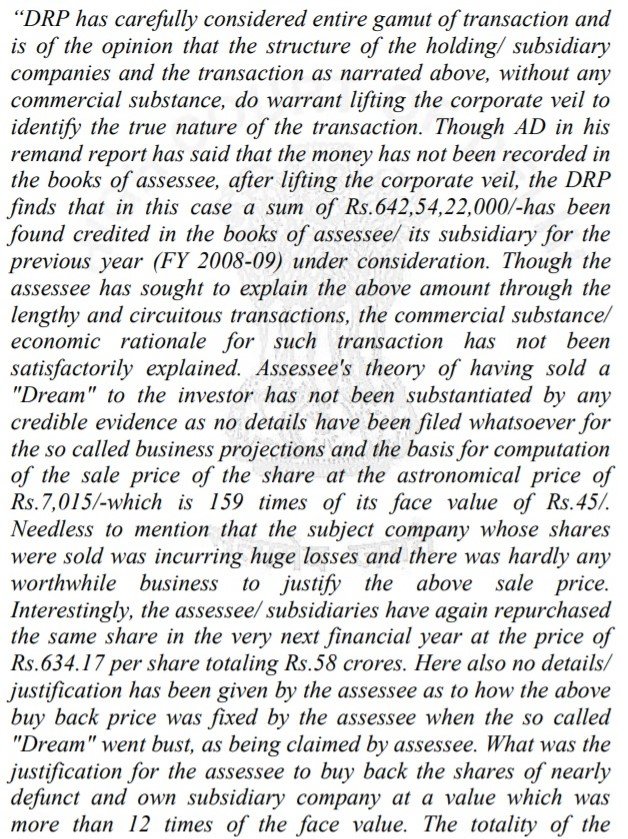

The DRP observed, “Though the assessee has sought to explain the above amount through the lengthy and circuitous transactions, the commercial substance/economic rationale for such transaction has not been satisfactorily explained.” It further noted, “Assessee’s theory of having sold a “Dream” to the investor has not been substantiated by any credible evidence as no details have been filed whatsoever for the so called business projections and the basis for computation of the sale price of the share at the astronomical price of Rs.7,015/-which is 159 times of its face value of Rs.45/.”

Furthermore, the NNIH was incurring huge losses and there appeared to be no justification as to why investors would invest in the company and buy shares at such exorbitant prices. Interestingly, the shares were bought back the next financial year at the rate of Rs.634.17 per share totaling Rs.58 crores. In neither instance was any justification provided for the price of the shares that were fixed.

The DRP observes, “no details/justification has been given by the assessee as to how the above buy back price was fixed by the assessee when the so called “Dream” went bust, as being claimed by assessee. What was the justification for the assessee to buy back the shares of nearly defunct and own subsidiary company at a value which was more than 12 times of the face value.”

Thus, the DRP concluded, “The totality of the transaction clearly lead to the inescapable conclusion that the entire transaction of sale & subsequent buy back of shares was a “sham” transaction entered into by the assessee with the sole motive of introducing Rs.642,54,22,000/-in its books and providing loss of Rs.584.46 crores to Universal Studios BV Netherlands.”

Lastly, it noted, “In view of the facts and finding as mentioned above and taking the totality of the picture into consideration, it is held that assessee has brought an amount of Rs.642,54,22,000/- being unexplained money in to its books through its subsidiary

NDTV Networks BV Netherlands (NNBV). It is pertinent to mention that, as per the admission of the assessee the above subsidiary has been subsequently liquidated, which shows that the same was floated only to create a front for introducing the above amount.”

It is pertinent to mention that the NNIH finds mention in the CBI’s new FIR against NDTV and that the subsidiaries of NDTV are intricately intertwined with each other through a series of complex transactions. The CBI’s FIR states, “NDTV Ltd. incorporated other company in Netherlands on 10.04.08 in the name and style of M/s NDTV lnternational Holding BV for the purpose of raising funds of USD 150 million from M/s NBCU, a subsidiary of General Electric USA. M/s NBCU transferred an amount of USD 150 million from the account of its subsidiary M/s Universal Studios lnternational BV Netherland on 23.05.08. By investing the said amount by NBCU in NDTV lnternational Holdings, M/s NBCU acquired 26% indirect share holding in NNPLC.”

On the same note, the DRP observes that “the money amounting to US $150 million received by an NDTV subsidiary NDTV Networks International Holdings BV, Netherlands from Universal Studios International BV, Netherlands on account of issue of shares of its indirect subsidiary NDTV BV, resulting in transfer of 26% effective indirect stake in NNPLC, represents NDTV’s own unaccounted money introduced into its books through its subsidiary NDTV Networks BV (NNBV) through this ‘sham’ transaction and the same was directed to be added to the taxable income of NDTV.”

The AO also relied on the tax evasion petitions filed by shareholders of NDTV alleging that the money introduced in its subsidiaries is its own unaccounted money which was later transferred to NDTV through merger and liquidation of its subsidiaries. Thus, the AO concluded that the investments made in NNPLC through Step Up Coupon Bonds were a sham transaction and NDTV’s own money along the lines of the investment made in other subsidiaries.

The AO is said to have taken note of these tax evasion petitions because they were received from NDTV’s shareholders “who were aware of its internal affairs and aim and object of floating complex corporate structure by the petitioner; therefore, the AO had reason to believe that information was credible.” It is further said, “The tax evasion petition

contained detailed information regarding the complex corporate structure created by petitioner to route funds and evade taxes and most of this information was corroborated with the findings of the DRP for AY 2009-10.”

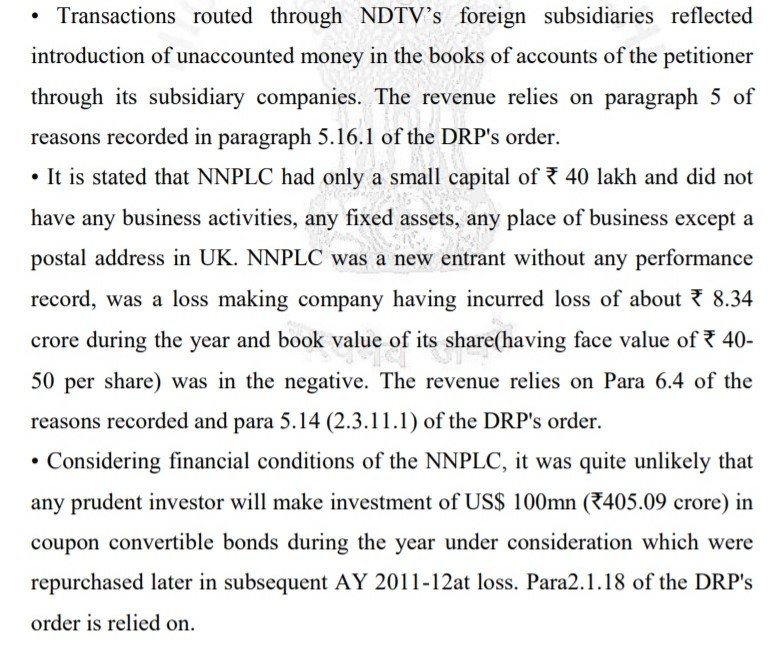

The authorities further observed that the NNPLC had a capital of only Rs. 40 lakh and did not have any business activities or fixed assets. It was a new company with no performance record, was incurring losses and therefore, it was unlikely that any investor with a sound mind would invest such huge sums in it.

In light of the arguments made, the Court ruled that “the complex and circuitous structure of subsidiaries and the transactions entered therein are closely connected and provide a live link for the formation of the belief of the AO that there has been escapement of income in AY 2009-10 and for the previous assessment year, AY 2008-09 as well because the investments continued that year.”

The Judgment stated, “NDTV has alleged that the details of the corporate guarantee issued by NDTV to NNPLC regarding the Step Up Coupon Bonds was intimated to the Revenue during the original assessment proceeding. This argument of NDTV falls flat in light of the judicial decisions mentioned above considering that the AO has reason to believe that this transaction is bogus. For these reasons, this Court is of the view that the impugned reassessment notice is valid in law and can be sustained.”

NDTV objected to the provisional attachment of its assets under section 281B of the Income Tax Act, 1961 on the grounds that it is mala fide and in violation of the said Act. NDTV argued that the respondent in the matter, the CIT, failed to establish that NDTV was likely to thwart attempts at recovering legitimate taxes. Furthermore, it argued that the relevant section cannot be invoked merely on grounds of difficulty in recovering taxes.

However, on this matter as well, the Court agreed with the decision of the authorities to provisionally attach NDTV’s assets and shot down NDTV’s objections. It observed that “a reasonable apprehension that NDTV may liquidate the assets thwarting the recovery of tax liability is not unwarranted.” It added, “the impugned order under Section 281B does not suffer from any infirmities and is valid under the Act.”

According to the new FIR filed against NDTV by the CBI involving the said subsidiaries, it isn’t merely a case of tax evasion or corruption. It is alleged that NNPLC got approval from the FIPB board in violation of the existing FDI norms. It was also alleged that the investments made in these subsidiaries were actually the tainted money of unknown public servants. Furthermore, charges were also slapped on unknown public servants who allegedly colluded with NDTV in their criminal conspiracy.

The FIR, thus, reminds one of the allegations made by Income Tax Officer Sanjay Srivastava who had claimed that P. Chidambaram had parked his bribe money in NDTV. In an 88 page letter written to the CBI chief in April in 2018, Srivastava had said that “NDTV Ltd. needs to be investigated over parking of bribe of US $40 million by Maxis and its owner T. Ananda Krishnan (accused in the Aircel-Maxis case) on behalf of P Chidambaram and Karti P. Chidambaram for obtaining FIPB approval in Rs.3500 crores. Aircel-Maxis deal fraudulently claiming the proposal for Rs.180 crores only when gross value of the proposal was to be considered and which has been hushed up by certain IRS officers in lieu of bribe paid by NDTV Ltd.”

According to Srivastava, in return of the senior Chidambaram’s favour to Aircel-Maxis, his son Karti was paid $40 million, which was routed through NDTV. He claimed that the transaction was “disguised as a purchase of shares (49% indirect stake whatever that may mean) of NDTV Lifestyle Holdings Pvt. Ltd wholly owned by NDTV Networks Plc, UK which was wholly owned by NDTV Networks BV, Holland and which in turn was wholly owned by NDTV Ltd, India and all of which were sham letterbox companies owned and floated by NDTV Ltd to launder the proceeds of crime bring the bribe paid to the Union Finance Minister P Chidambaram and Karti by various entities by All Astro Asia Networks Plc, UK wholly owned subsidiary of the Maxis Ltd an T Ananda Krishnan.”

It is to be noted that the NDTV Networks Plc, UK and NDTV Networks BV (NNBV) mentioned by Srivastava are the same NNPLC, London and NNBV, Netherlands which have been mentioned in the DRP examination of the AO’s findings as mentioned above. According to the AO, the investment made in NNPLC was a sham transaction of a similar nature to the $150 million made in NNBV.

The officer went on to add that “the fraudulent nature of the transaction between NDTV and Maxis is borne out from the fact that Maxis Ltd never cared to carry its investment or seek any return on that or get involved in the affairs of the company which was 49% owned by Maxis Ltd & had just forgotten their huge investment of about Rs.200 crores with NDTV Ltd and its subsidiaries. The case was hushed up by the NDTV Ltd by paying a bribe to the Indian Revenue Service (IRS) officers.”

On Wednesday, OpIndia.com learnt from government sources Chidambaram’s modus operandi. We were told that it revolved around granting illegal FIPB clearances to receive kickbacks, often paid through various shell companies floated by his son Karti Chidambaram. Thus, it appears that the INX Media case, the new FIR against NDTV and Chidambaram’s arrest are all interconnected. If one card falls, the entire pack would collapse.