Dubai is again back in the news but for the wrong reasons. With the ongoing Covid-19 pandemic, Dubai is staring at a recession with experts forecasting Dubai’s economy is going to shrink by 5.5% in 2020. Dubai faces about $10 billion in debt maturities this year with revenues expected to drop in line with the pattern of the 2009 crisis. Bank of America estimates that Dubai’s fiscal deficit could widen to $4.4 billion, or 3.9% of GDP, and could be as high as 5.3% if interest payments on a loan from Emirates NBD, Dubai’s biggest lender, are included.

The pandemic and the associated lockdowns have hit Dubai’s economy which relies majorly on retail sales, travel, tourism and real estate sectors really hard. One survey expected, 70 per cent of Dubai companies to go out of business within six months due to the pandemic. Amid the current uncertainty, businesses in UAE’s seven emirates, as elsewhere across the world, are slashing salaries, putting employees on unpaid leave, and reducing staffing levels and Dubai is no exception.

The state-owned airline, Emirates recently fired 600 pilots including a few Indians with what is being seen as one of the largest layoffs in the aviation industry. The airline has also announced 50 per cent salary cuts for employees in all grades 4 and above until September. Dubai’s property developers are cutting salaries by as much as half as the pandemic hits Dubai’s property developers and mall owners. Joyalukkas, is closing its “weak performing” outlets, while Malabar Gold & Diamonds, with more than 100 outlets in the GCC states, has decided to delay opening all its stores until there is clarity on rent reductions from its landlords. Similarly, it’s likely more retail stores will face closure leading to job losses.

The topic of these articles though is actually not on the short term pain faced by Dubai. Almost any nation today is facing the same acute economic crisis due to the pandemic and Dubai is definitely no exception. You can pick any country in Europe, the Americas or the Asia Pacific and you will be to gather enough headlines about business closures, job losses, defaults and recessions. The point that I want to stress is the long term decline of Dubai and its slow death. Let me elucidate the same

Setting the context for the decline of long term decline of Dubai, one has to understand the most critical factor and that is oil and the petrodollar economy associated with it.

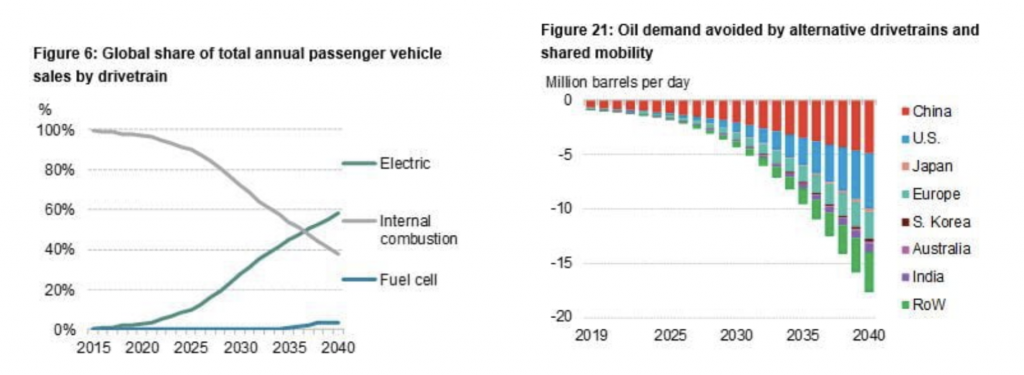

Decline in Oil prices: Coronavirus just laid bare the real strength of petrodollar economies. It has heralded the long term decline of Oil and the purchasing power associated with it. The focus on renewable energy and electrification of transportation has reached a tipping point. Read what the latest Bloomberg New Energy Finance had to say about this – There are over 500,000 e-buses, ~400,000 electric delivery vans and trucks, and 184 million electric mopeds, scooters and motorcycles on the road globally today as we speak. EVs’ share of global car sales is around 3 per cent in 2020 and is expected to rise to 10 per cent by 2025 and 58 per cent in 2040.

Some 30 per cent of global 2- and 3-wheeler sales & 20 per cent of the existing fleet are already electric. Sales of internal combustion passenger vehicles peaked in 2017 and are in permanent decline. EVs across all segments are already displacing 1 Mn barrels of oil demand per day. Oil demand from passenger cars is hit hard by Covid-19 and will never recover to 2019 levels. But growth in commercial vehicles keeps overall road oil demand growing until 2031 when it starts to decline. With long term structural decline in demand, the oil will see more periods of a low price point than high price points.

Of course, the counter-argument that is thrown around is that Dubai is the least dependent on Oil revenues among gulf economies and hence the long term structural decline in oil prices shouldn’t impact it. Dubai’s diversification is going to ensure that not only does it survive but also prosper in this new world bereft of petrodollars. I do agree that Dubai on the surface looks well-diversified and that Dubai has a negligible contribution from direct production and export of oil.

However one tends to miss the forest for the trees and while Dubai does truly have a well-diversified economy across multiple non-petroleum sectors, it, however, is intrinsically linked to the larger oil-based economies powering the Gulf countries and its neighbours. Dubai has negligible energy resources, but its role as a petrodollar recycling hub means its fortunes have long swung in tandem with its larger oil-exporting neighbours. Let me elaborate on how that’s the case, today the major sectors contributing to Dubai’s economy are listed below

The three major pillars supporting Dubai’s economy are. – Trade (physical and financial), Retail (Wholesale incl) and Real Estate (Construction incl).

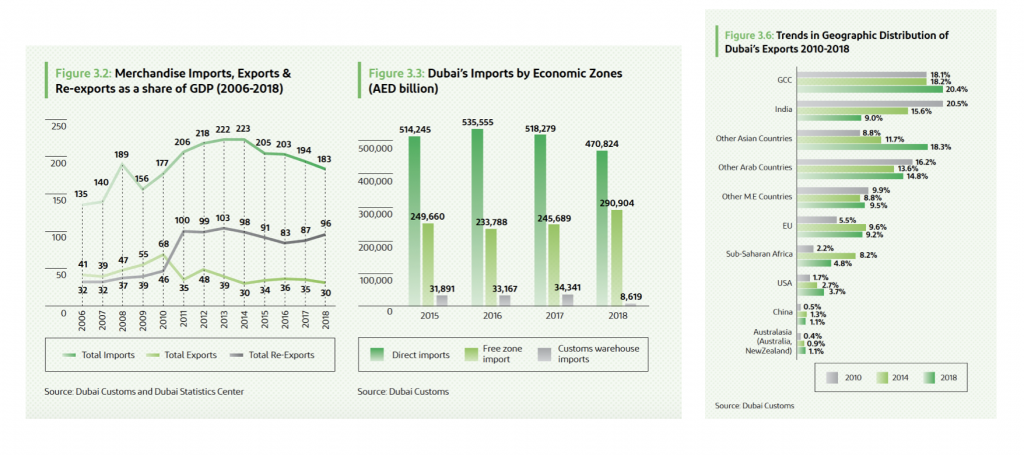

Let us start with trade, Foreign trade is a very important contributor to the economy. Foreign trade value is nearly 321 per cent the value of the GDP. Dubai is an important financial and trading hub for the Middle East, South Asia and Africa. Dubai imports commodities, manufactured goods and re-exports the same to these markets. However, Dubai’s role as a key trading hub is built on weak foundations. Re-export of imported items account for nearly 75 per cent by value of total Dubai’s exports with only 25 per cent of Dubai’s export-driven by domestic production. Hence the trade is not powered by a strong domestic industry, unlike China or Singapore. Domestic exports account for nearly 50 per cent in the case of Singapore.

Singapore is a manufacturing powerhouse with 20 per cent contribution to overall GDP as compared to 10 per cent for Dubai. Additionally, an even more important point to note is that other the Middle East and Arab countries such as Saudi Arabia, Oman account for nearly 45 per cent of Dubai’s exports. Even though Dubai itself is not directly dependent on oil, its major trading partners accounting to nearly half of its trade are heavily dependent on the fortunes of oil. Hence long term decline in purchasing power of oil economies means a direct hit on the trade and economies of Dubai’s partner countries.

The decline in trade will impact in more than one ways as loss of significant share results in loss of scale which originally helped Dubai achieve competitive advantage to emerge as the trading hub of choice. Re-export to South Asia will eventually move to Mumbai or Gujarat with the ongoing up-gradation of infrastructure and East African ports can one day replace Dubai’s as the key trading hub for Africa.

This also reflects in services. Take for example the Tourism industry, nearly 27 per cent (1 in 4) tourists coming to Dubai are from GCC or the Middle East and Arab countries. The drop in oil price will reduce the disposable income available with an average Saudi or Kuwaiti reducing their spend in Dubai. This will have a chain reaction with impact retail sales, hospitality and allied sectors. With most Middle Eastern oil-producing nations drawing down their reserves due to low oil prices, there will be less scope for investments and recycling of petrodollars in the days to come. This will impact the financial, consulting and export of other services to the wider Middle East. Hence decline in oil prices will not only result in lower trade of physical goods but also in lesser trade in services.

The next important sector we will look at is the real estate and construction sector. Real estate and construction collectively accounts for 13-15 per cent of GDP. But the real estate sector in Dubai is in a big mess. It all started with the tremendous growth of Dubai’s real estate market leading up to 2014 correlate with the spike in oil prices. That spike created a glut in supply which is yet to be cleared after 6 years. And with Pandemic, the supply overhang might never get fully cleared in the coming years. The real fact is that Dubai’s real estate market is not purely driven by domestic considerations.

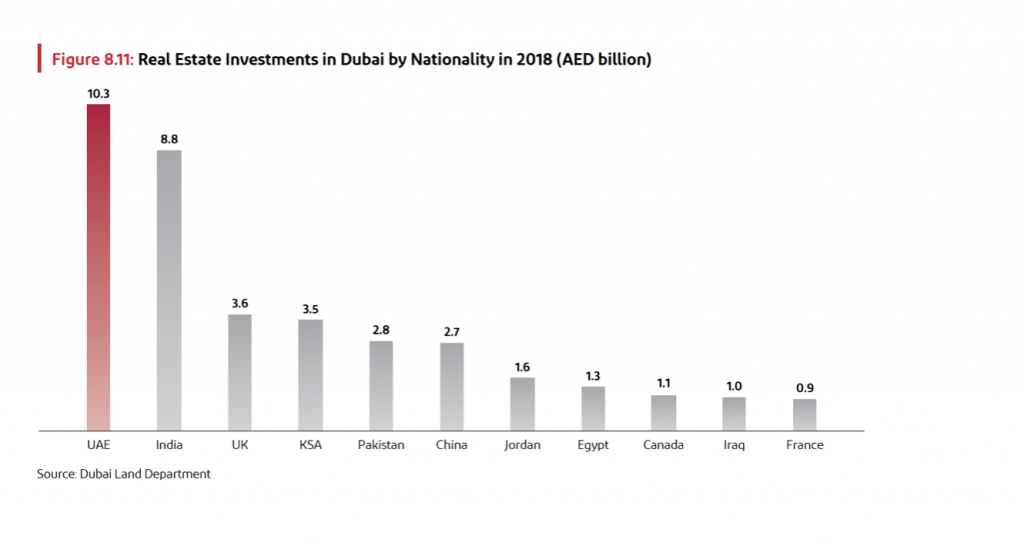

Given the lax or lightly regulated nature of Dubai, a significant share of money from outside investors is parked in Dubai’s real estate. Dubai is an attractive destination for parking of illicit, corrupt or black money. Domestic investment in real estate by Emiratis account for only 20 per cent of total investment.

To elaborate on the impact of illicit money flow into Dubai’s real estate, let us look at India which accounts for nearly 20 per cent of all investments into Dubai real estate. While there are no accurate estimates on how much of the above is illicit or black money. The bulk of purchases are made by wealthy Indians to escape political strife and taxes. According to industry sources in Dubai, close to $100 million moves from India to Dubai every single day!

This money uses the ‘hawala’ route, an informal money transfer system, where rupee gets converted to a dollar at a premium to market exchange rates. In the process, Indian black money is invested in Dubai property. And since Dubai charges no tax on rental income or any capital gains for the purchased property, cash-rich Indians know their investments are safe. The modus operandi is also used by money launderers, smugglers, underworld gangsters and drug traffickers to make payments to propel working for them. Take for example, recently in Jan 2020, ED conducted searches at the residence of a former chief engineer of BMC. ED, in a statement, said incriminating documents with regard to illegal acquisition of a property held in Dubai was recovered during the search operation. The property was in Dubai at ‘Park Island, Bonaire Marsa, Dubai’ measuring 89 square metres purchased for Rs 70 lakh in 2012.

This flow of illicit money into Dubai’s real estate is one of the major causes for the subsequent crisis that we are seeing today. The emirate’s decision in 2002 to allow foreign ownership of so-called “freehold” properties drew a rapid construction boom that attracted developers from across the world. Money quickly flowed in from all corners of the world from Pakistan, India to Mexico and Russia. This flow of money resulted in real estate boom where people could easily flip luxury properties for a quick profit. Speculators made a fast buck by selling off-plan properties for a large profit within weeks of their initial investment – with no intention of ever living there. This caught the attention of the Dubai government who wanted to get into the action.

The result was government today controls some of the emirate’s biggest developers. The state-linked firms, created to speed up construction, used cheap and often free land to compete for buyers. Some paid upfront without waiting for homes to be completed by depositing only 5 per cent of the value. And excessively optimistic projections of growth in Dubai’s population, which consists largely of foreigners, only fed the building boom leading up to 2014 when the bubble finally burst with the collapse of oil prices. Much of today’s property glut is of the government’s own making with land sales remaining an important source of state revenue.

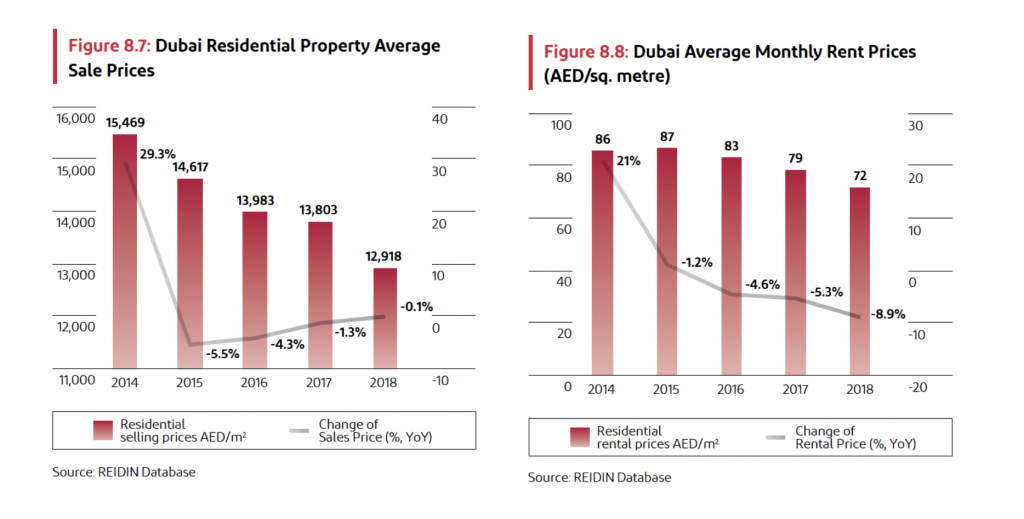

This chronic oversupply resulted in the reversal in property value and rental yields in Dubai. Dubai’s property value has seen consistent decline in prices since 2014. Residential property prices have fallen 16 per cent from 2014 to 2018. Rental yields have followed suite dropping similarly by 16 per cent in the same period. The falling prices makes Dubai real estate a bad investment destination today irrespective of advantages with regards to hiding from regulators and tax authorities.

And the Real Estate prices and rental yield will continue to drop for two reasons. Supply overhang – With a massive guaranteed oversupply of properties and top developers taking losses in 2019, S&P Global ratings said for 2020, it could see another a potential decline of 5 to 10 percent. And this estimate was before Covid-19 stuck the world. The market is already struggling, and 2020 is expected to be a year of the very high delivery cycle. There are still launches with small deposits and long-term payment plans. The oversupply situation is so bad that Dubai is even considering committee to control Dubai’s housing supply.

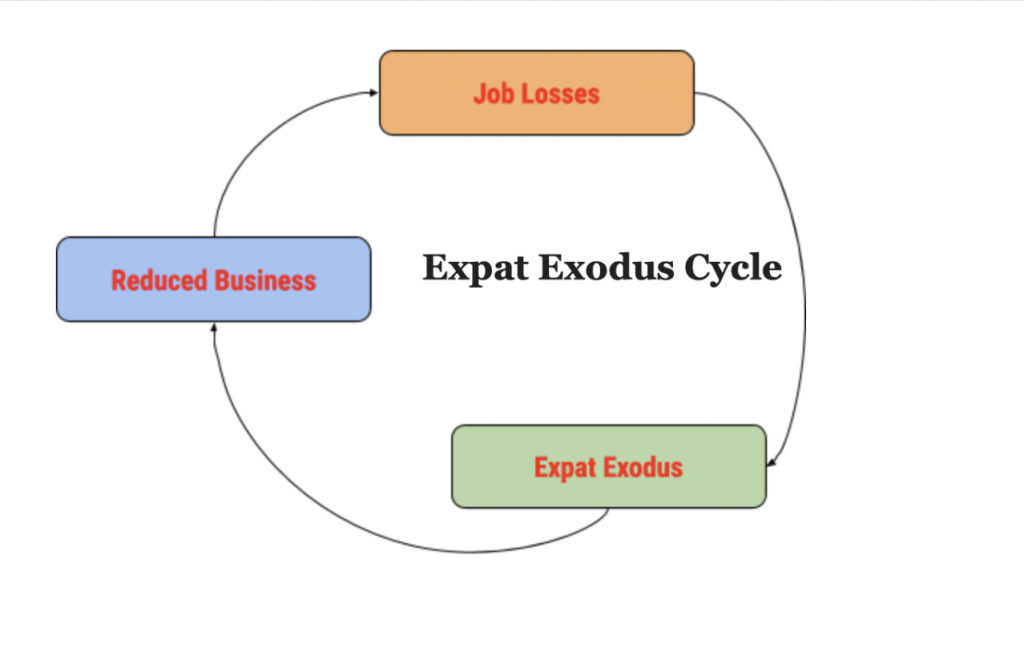

This brings to the next important factor for the decline of the real estate sector and that is ex-pat population. In fact, one can argue that Dubai is highly dependent on one commodity which defines its success and that is the ex-pat population. Dubai is one of those few countries along with its fellow GCC members where ex-pats outnumber locals. Only 15 per cent of Dubai’s population is local Emirati with ex-pats accounting for 85 per cent of the total population. It is estimated that an average ex-pat contributes to 30,000 to 40,000 USD to Dubai’s economy. At an estimated population of 2.8 Million, Ex-pats are estimated to contribute 85 Billion dollars accounting for nearly 20 per cent of Dubai’s economy. However, the continued slump post-oil crash in 2014 and now the coronavirus pandemic is resulting in a drastic outflow of the ex-pat population.

Oxford Economics estimates the United Arab Emirates, of which Dubai is a part, could lose 900,000 jobs — eye-watering for a country of 9.6 million — and see 10 per cent of its residents uproot. The coronavirus is the trigger that is going to start an ex-pat exodus resulting in a death spiral. As ex-pats move out, sectors that relied on those professionals and their families for business such as restaurants, luxury goods, schools and clinics will all suffer. This will create more job losses in these sectors which will trigger further exodus resulting in a self-fulfilling cycle.

With no formal route to citizenship or permanent residency and no benefits to bridge the hard times, it’s a precarious existence for most ex-pats. Education is emerging as a deciding factor for families, Dubai has the region’s highest median school cost last year at $11,402, according to the International Schools Database. With falling revenues, the Dubai government might decide to introduce Income tax, destroying the main attractive factor for wealthy and educate the ex-pat population.

Hence more and more ex-pats are reconsidering their choice to stay in Dubai. And as more ex-pats decide to leave, more business will be impacted by the reduced spending which will result in more job losses triggering the next wave of the exodus. This will put sharp pressure on Dubai’s real estate sector. Already suffering from the overhang of excess supply and with new property launches planned till 2022, the ex-pat exodus will trigger a further sharp fall in real estate prices and rental yields. With property prices already seeing up to 25 per cent reduction in prices, any further drop would exacerbate the capital loss for the investors. The continued fall in property prices will deter any investors including those with ill-gotten wealth who will now think twice before in investing in Dubai.

The final important sector that we will look at is the wholesale and retail trade. It is the largest employer accounting to nearly 20 per cent of the total employees. The drivers of demand in the wholesale and retail trade are mainly domestic population growth and tourism. I have already elaborated how low oil prices are going to impact Tourism. Additionally, the main attractiveness of Dubai is the presence of major brands which results in tourists purchasing items not available in domestic markets.

However as Brands continue to go global, the retail attractiveness for tourists will decline. Add to this the fact, globally retail is moving online and Dubai cannot be immune to such changes, the retail industry will definitely be impacted. E-commerce already accounts for nearly 10 per cent of retail sales in Dubai in 2018. This will put further pressure on the offline retail industry. On top of all of these is the ex-pat exodus elaborated previously which will bear immense damage to this sector. With ex-pats accounting for 85 per cent of the population, any drop in the ex-pat population will have a direct and proportional impact on retail sales. So while retail and wholesale sector accounts for the largest share of GDP (25 per cent), they are the most sensitive to global macroeconomic factors.

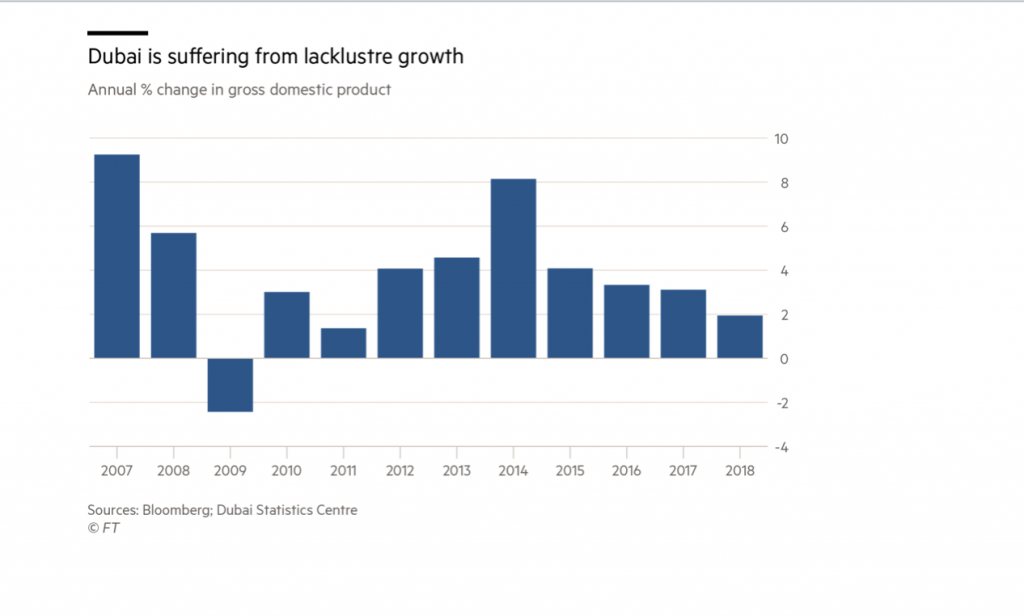

Thus Dubai’s economy while seemingly diversified from the vagaries of oil production is actually built on weak foundations and indirectly rely on two commodities – Petrodollars via spending by other gulf countries and ex-pat population. These trends were well on their way even before Covid-19 stuck Dubai. This FT article illustrates some of the above problems that Dubai was already facing in 2019 much before Covid-19 pandemic appeared on the scene. From clothing to cars, retailers saw sales slump by 50 per cent since the slowdown began with the collapse in oil prices in 2014. Hoteliers were slashing room rates as tourism growth was slowing, hampered by the strong dollar-linked currency and a surfeit of new rooms.

Restaurants were shutting their doors as wealthy expatriates were replaced by less experienced ones, who were being paid less and were saving more because of job insecurity. PepsiCo had made redundancies at its Dubai headquarters and moved about 30 per cent of roles into larger markets such as Egypt and Saudi Arabia. The growth in tourist numbers had slowed since 2017, despite waves of Chinese and Russian nationals arriving, falling short of the relentless pace of hotel construction. So Covid-19 pandemic is not the trigger of the long term crisis Dubai is facing but a catalyst expediting the pace of its decline.

So are we going to see Dubai’s death in 2020, is this the end of it. The answer is no, while the above factors are going to impact Dubai, some of these take a longer-term to play out. It will take another decade or so for Dubai to see the full implications of these factors. Additionally, the above scenario doesn’t take into account any black swan geopolitical events such as the potential crisis in Oman and chaos associated with it or a new Saudi – Iran war with Dubai being one of the centres of such hostilities.

Any such black swan event will expedite the above decline triggering a bigger exodus and further collapse of its economy. The Best case scenario for Dubai today is its rulers take continued measures to slow down the rate of decline and provide a smooth landing. Dubai and all its glitz and glamour with its towering skyscrapers and island villas will disappear into the sunset just like the glitzy gold rush towns of the previous century.